First let me say that I don't have anything against short selling in general. People bet on stocks going up, they should be allowed to bet on stocks going down. Personally, I do both and I don't think it makes me a bad person. Short "squeezes" also do not benefit long term shareholders. If every single Tesla short covered tomorrow what would happen? The stock price would go up, then it would come right back down. Nothing changes with the company, and unless shareholders become traders to time this event, nothing changes with their holdings either.

Also, my view is that CEOs should focus on running their company instead of their stock price, because in the long run only the fundamentals matter. Elon Musk historically has commented on Tesla's stock price, but very sporadically. The infamous "tsunami of hurt", the "don't have any right to deserve" our current market cap etc. I haven't had a problem with it because its been sparse, he's been balanced, and honestly he's been accurate. But there has been a decided shift lately. His interest and rhetoric has been ramping up versus the short sellers, dating back almost a year ago but really reaching a crescendo this past month.

Initially, it made me a bit uncomfortable whenever he engaged short sellers. Again, focus on running the company and share price will follow. However, in recent weeks I came upon an excerpt from The Divide: American Injustice in the Age of the Wealth Gap by Matt Taibbi that was posted here on TMC that radically changed my view. I've attached this excerpt and strongly encourage any longs to read it, because it will give you newfound perspective on the events surrounding Tesla.

Brief synopsis:

In 2002, Canadian insurance company Fairfax Financial run by Prem Watsa decided to list on the NYSE. Watsa was a bit of a prodigy and is known as the "Canadian Warren Buffet". In the summer of 2002, investing legend who made his name exposing Enron, Jim Chanos, decided something was wrong at Fairfax and bet against it. Chanos evangelized his belief in Fairfax's shortcomings, and by the end of 2002 a slew of other hedge fund titans followed suit, including Steven Cohen, Dan Loeb, Adam Sender. This culminated on Jan 17, 2003 when an analyst report from investment bank Morgan Keegan asserted that Fairfax was under-reserved by $5 billion, making it insolvent. This sent the stock down 25% the next day. Extraordinarily, this report was written by a rookie analyst John Gwynn who just came from Trinity, one of the hedge funds who made a huge bet against Fairfax. The collective hedge funds may have initially genuinely believed that Fairfax was corrupt or incompetent, but their even stronger belief was that enough bad press and market momentum would crater the firm. Chanos' own words, "With a financial services company like Fairfax, it can all be self-fulfilling. If the market finally decides the glass isn't half full anymore, the trouble starts... you can see the stock go into a waterfall." That was supposed to happen with the Morgan Keegan analyst report, but it didn't. Questions surfaced about the accuracy of the $5 billion calculation, and in February 2003 Fairfax released a positive financial report that shot the stock back up. The shorts flipped out. In Dan Loeb's text conversation: "We need to speak to the rating agencies today... they could provide the downside catalyst."

Incredibly, over the next three years was stories of harassment of Fairfax workers, the CEO Prem Watsa, his wife, even his pastor. While this was happening Fairfax was besieged by accusations of fraud sent to rating agencies, regulators, even Fairfax's own business partners. Nearly all of these troubles could be traced back to Spyro Contogouris, a man hired by Chanos, Loeb, and Sender to "bring down Fairfax". Contogouris’s strategy would be to sink Fairfax by “closing access to the capital markets”—cutting off its access to funding by undermining its reputation. This was old-school Sun Tzu stuff, isolate-and-destroy tactics, “attacking by stratagem”: General Contogouris would cut off his enemy’s supply lines by, among other things, sullying the firm’s standing with ratings agencies and shareholders and others in a group he termed “FoF,” for “Friends of Fairfax.” He wanted to “get them where they eat,” cutting off their credit lines, particularly going after their ratings by agencies like A. M. Best. All this Contogouris promised to Chanos, Loeb, Sender, and others from the start. He pledged to “get the message of what I think is a massive fraud to these long term value holders” by creating a “crisis of confidence” that would frighten investors and “shake them out of the stock.

By late July in 2006, Fairfax really was on the verge of collapse. Its stock price was declining, long loyal shareholders were slowly departing, questions from rating agencies, its executives were under surveillance by the FBI, and it was receiving subpoenas from the SEC. Like any financial firm, an insurance company can quickly implode in a run-on-the-bank-like crisis of confidence, and if it did not answer its detractors soon its share price might crater and the firm might go out of business.

So Fairfax ultimately made the only move it had left, it sued. And merely filing it was what saved the firm. The detailed response about all the allegations spooked short investors who jumped on the bandwagon with Chanos and the rest. According to discovery materials, some of these investors were all but assured that Fairfax was about to be busted by authorities at any moment and was sure to go out of business. So when Fairfax was gearing up for a long legal battle instead of just rolling over, it didn't seem to be the behavior of a guilty company. The short sellers began to cover.

On June 23, 2006 Fairfax share price reached a low of $100.00. A month later, on July 26, 2006, they decided to fight back and file suit. On June 15, 2018, last Friday, Fairfax closed at an all time high of $775.19.

Solarcity

First we have to talk about Solarcity since that is where Chanos and some of these same bad actors started here. I know Einhorn is at least another hedge fund mogul who is also short Tesla.

Solarcity was in essence a financial company. They were an arbitrage firm that profited from the difference between their borrow rate and their leasing rate to their customers. Now there was a bunch of noise and opaque accounting about how shareholder value should be calculated, net present value, renewal rates etc. So you can argue that it was worth $30 a share, or $20, or $10. But as far as keeping its doors open, as long as it could continue to borrow, and at a lower rate than it leased(and all the costs associated), their business can be profitable and continue to run. And in theory, their borrow rate should be determined by their ability to service this debt. In reality, it was determined by the market's confidence in their ability to service this debt. Which is exactly where Chanos, like with Fairfax, began his attack.

When Chanos announced his short in August 2015, his thesis was that Solarcity was a subprime lender. That at any moment, Solarcity's customers could stop paying their bills. This was ignoring the fact that Solarcity customers had an average FICO score 750, compared to below 620 to be considered subprime. Not to mention unlike defaulting on a home mortgage, where when you are underwater enough it can make financial sense.(not to mention you still get to live there for months) Defaulting on payments to Solarcity would make no financial sense, because reverting back to your utility would cost more. That was the whole value proposition from Solarcity.

But that was not what this was about. Because Solarcity and the entire solar industry had real issues at that time, with huge uncertainty whether the Investment Tax Credit would get renewed, not to mention Sunedison collapse. Demand was uncertain, and Solarcity had to significantly cut back their growth, by half. The stock would have gone down with or without short sellers. But what Chanos was doing was exactly what he described in his own words about Fairfax. He was taking advantage of a bad situation, and using fear to create a "crisis of confidence". Solarcity, after all, was a financial company. And as Chanos knows too well, it becomes a self-fulfilling prophecy once investor confidence is broken.

The first highlighted area was when Chanos announced his short. Elon responded the next day and bought stock, as well as making a rebuttal on CNBC, iirc. The second highlighted area is an incredible similarity to the Fairfax story. Gordon Johnson, a solar analyst of Axiom Capital initiated coverage of Solarcity that day with a scathing Sell rating. This seem to set off the "waterfall" of Solarcity's decline. Over the next year, Johnson would publish report after report reiterating his bearish stance. This in itself isn't necessarily incriminating, perhaps he was even right. Since Tesla acquired Solarcity, Chanos moved his short onto TSLA. Curiously, Johnson is now no longer with Axiom and has moved to Vertical group. He is also now no longer a solar analyst and instead "specializes in Basic materials sector", which apparently also includes Tesla. He initiated coverage on April 9, 2018 with a Sell rating and currently is the owner of the lowest price target on the street at $99. He is constantly seen on CNBC, every time reiterating the brilliant Bob Lutz-esque thesis of how much Tesla loses for every car sold.

So how would Solarcity have looked today without these short sellers? Well we know that the two other installers, Vivint and Sunrun are alive and well. In fact, Sunrun, has a very similar business model to Solarcity, with the same opaque accounting regarding NPV and renewal rates. It did not even pivot to loans from leases like the others did to conserve cash. Sunrun is currently trading at an all time high.

Solarcity did have one major issue that was company specific. During this already difficult time for the entire industry, they were tied to the Buffalo Silevo plant, and all the cap ex costs associated. Would these costs have overwhelmed them? Could they have found financing to get them through? Especially now that we see the business model has proven viable after the fact? I don't know the answers to those questions. Perhaps they would have gone under either way. What I do know, or highly suspect, is that the negativity created by short sellers like Chanos and analysts like Johnson made certain that the capital markets were closed shut, to ensure that those questions never needed to be asked.

Solarcity is water under the bridge, and its fate debatable. But the same bad actors who attempted to take down Fairfax, the same bad actors who attempted and nearly(or perhaps they did) succeed in taking down Solarcity, have now moved on to Tesla.

Short interest

Tesla currently has close to 40 million shares or over $12 billion dollars betting against it. It is easy to conflate this with the litany of Tesla bears all over social media, twitter, seeking alpha, etc. Don't. These people may be responsible for 99% of the noise, but I highly doubt if they even amount to 10% of the short interest.

Historically in the stock market, a high short interest is actually bearish and indicative that something is wrong. (there are obviously great examples to the contrary, ie AMZN) And in general short sellers are considered more sophisticated than the average long, because they are mostly professional traders/fund managers vs retail investors. While there does seem to be an inordinate amount of "retail shorts" in Tesla, I believe the actual money amount is minimal compared to the real actors.

Over the past few years, there has been three significant spikes in short interest.

So the bear thesis ranges from Tesla is overvalued, to Tesla cannot make a profit(therefore doomed to bankruptcy), to now recently I'm hearing more that Tesla is fraudulent. As professional, sophisticated, presumably intelligent short sellers who believe in any of that, you would think they would short the most when the stock is high. After all, is Tesla not most overvalued when it is highest? Reality is not the case, in fact short interest is lowest at the peaks, and the three spikes in short interest all coincide with significant market declines. Now, it is easy to scoff at this and dismiss it as "dumb shorts" buying highs and selling the lows. I am sorry, but as a trader of many years, you cannot convince me that this is $12 billion of dumb money.

Moreover, the three spikes in short interest all coincide with specific events:

1. In early 2016 there was a market downturn that stemmed from declining high yield bonds that contributed to this. But also, it coincided with the Solarcity short seller attack described before. If Solarcity was forced into bankruptcy, they would have defaulted on their solar bonds that Spacex bought previously. All Elon Musk companies are connected, and all would have been harmed. It is almost as if it was a coordinated attack.

2. In late 2016, short interest rose to an all time high. I remember the negativity was overwhelming during this period. Constant negative media coverage and bearish articles/analyst reports. And then all of sudden, it all went away and the stock rallied. Do you remember what changed? Do you remember what those analyst reports and bearish articles were about? This was the lead up to the Solarcity/Tesla merger vote. The articles and analyst reports were about how Solarcity and its mountain of debt was about to drown Tesla. The outrage was over the lack of corporate governance and how bad a deal this was. The other major narrative was that the deal would not pass. Gordon Johnson rears his head again and declares there is only a 50/50 chance of Tesla shareholders approving. (SCTY), Tesla Motors, Inc. (NASDAQ:TSLA) - Gordon Johnson Warns Of 'Burgeoning Risk' To SolarCity/Tesla Deal Closure Jim Chanos went on CNBC, imploring Tesla shareholders to reject the deal since it was so terrible and would bring Tesla down with it.

And then, Nov 17, 2016, the vote passes. The stock literally bottoms three days before this, and proceeds to rally to all time highs. Media negativity was gone instantly after the vote. Analyst reports muted. Think about that for a second, and logically if it even makes sense. If this deal truly was so bad, if it was the down fall of Tesla, shouldn't the overwhelming negativity occur AFTER the deal closes? After all, now that it is official and Tesla is responsible for this huge debt burden, isn't Tesla doomed? Yet there was nothing. Almost as if the negativity was to shut the deal down.

3. In March 2018, short interest spiked to a new all time high, to its current levels. This coincided with the Moody's downgrade, and sudden questions over liquidity. Just as Tesla's most important product is about to ramp. Just as Tesla is about to take its biggest leap, become profitable and sustainable as a company, a new narrative emerges: Bankruptcy. I will talk about this more in followup post.

To reiterate my sentiments towards short selling. I have no qualms with market participants betting that a stock is overvalued. I have no problems with people betting that a stock will go bankrupt. I believe the majority of the Tesla bears on social media, with the highest visibility, fit into those groups. I believe they are misguided, but they have every right to risk their own money how they like.

However, it is my belief that the vast majority that encompass the $12 billion in short interest do not fit this. They are not chasing highs and selling lows because they are emotional retail investors. They are not shorting because they think Tesla is overvalued. They are not shorting because they think Tesla will go bankrupt. They are shorting during specific periods when Tesla is most vulnerable, and covering when they fail to achieve their targeted goal. They are shorting to bankrupt Tesla.

Moody's

Hopefully by now you have read the transcript that's linked. If so, you understand the depth that these people will go to. You understand that analyst reports are circulated before to be front-runned. You understand the rating agencies are mentioned by name and used as tools. But you also have to understand, Fairfax Financial was a relative unknown midsize firm from Canada. Tesla's short interest is the largest in the entire US stock market. What is at stake now is profoundly greater, what about the methods? Of course I can't know that for sure. But what we do know:

After the close on 3/27, Moody's downgraded Tesla's debt to B3, senior notes to Caa1, with outlook negative.

Before this happened, during the trading session on 3/27 Tesla was down $25 on double the average volume. In the prior 11 trading days, Tesla was down 10. Note that the stock market as a whole was also down during this period, but not to this extent and especially less so on 3/27.

The rationale behind Moody's downgrade:

Tesla's ratings reflect the significant shortfall in the production rate of the company's Model 3 electric vehicle. The company also faces liquidity pressures due to its large negative free cash flow and the pending maturities of convertible bonds ($230 million in November 2018 and $920 million in March 2019). Tesla produced only 2,425 Model 3s during the fourth quarter of 2017; it is currently targeting a weekly production rate of 2,500 by the end of March, and 5,000 per week by the end of June. This compares with the company's year-earlier production expectations of 5,000 per week by the end of 2017 and 10,000 by the end of 2018.

The negative outlook reflects the likelihood that Tesla will have to undertake a large, near-term capital raise in order to refund maturing obligations and avoid a liquidity short-fall. Prospects for addressing its liquidity requirements (whether equity, convertible notes or debt) will be supported if the company can establish credibility for reaching Model 3 production levels -- 2,500 per week by the end of March, and 5,000 per week by the end of June.

So the crux of the downgrade and especially the negative outlook revolved around the uncertainty of Tesla's production rate. It was stated that this could be alleviated if Tesla could hit its production targets by the end of March. Those precise production targets were set to be updated the very next week. Moody's could have waited less than one week to confirm their projections in order to make a more informed judgment. Yet for some reason they did not, and was determined to get this downgrade out.

The fallout after Moody's downgrade:

Tesla bond price plummeted to 87 cents on the dollar, while yields approached 8%. Just a few short months before this, Tesla sold these bonds paying 5.3%. At these new prohibitive rates, Tesla was essentially shut out of the debt markets. This was happening precisely during Tesla's cash "valley" before Model 3 ramps up. There was talk of a liquidity crisis, while JP Morgan started peddling Tesla "crash puts" below $100. JPMorgan Recommends Tesla ‘Crash Puts’ With Tail Risk Rising

I did not have a position in Tesla at this time, and I did not yet read the excerpt from the Divde. I am not sure if my reaction would have changed much if I had. I consider myself a conservative bull, and after reading this news I became more cautious on Tesla than ever before. I understood that nothing has changed with Tesla the company, but there are many things outside of Tesla's control. Markets create a narrative and it takes on a life of it's own, especially when it comes to liquidity issues. It becomes a self-fulfilling prophecy.

Self-fulfilling prophecy

This is not the case for every company. If McDonalds were shut off from the debt markets and capital markets, it would not matter because they have a sizable cash horde and positive cash flow. No matter the amount of fear generated in the markets, there is no "bank" to run-on.

This is why short sellers like Jim Chanos target financial and insurance companies, they are beholden to the capital markets, and in his own words, once you create a "crisis of confidence", the story plays itself out. Fairfax was this way. Solarcity, due to its financial model, was this way.

Tesla is this way as well, for now.

The day that Tesla announced the Gigafactory, in a way, it became like a financial company. This is because from then on they were tied to years of capital expenses without any immediate return. To expand the company on top of that, while developing and tooling up for the Model X, Tesla Energy, service centers and superchargers, while all this was paid for only by the Model S. The company could not possibly fund this on its own, so it has been depending on the capital markets since. The day after announcing the Gigafactory, TSLA hit $265. I don't think it was a coincidence that it spent the next three years largely below this level with only two brief stints up to $280s. I also don't think it was a coincidence that only after 1/4/17 when Tesla announced that the Gigafactory was finally online did share price eventually break through to a higher range. (there were other factors including Tencent investment and anticipation for Model 3).

However, due to Model 3 delays and the enormous costs associated with ramping, Tesla arrived at a "cash valley" right before Model 3 really ramps up. When you exacerbate this with the Moody's downgrade and shutting off the debt markets, Tesla once again is at a precarious position. I became extremely cautious because I've seen this movie before when a ratings downgrade leads to a liquidity event, which was exactly the intent here.

A little background: I am a trader for a living and often use something called an analog as a tool. It is a comparison of two charts that mirror eachother. The idea is that stock movement is largely emotion driven in the short run, and if you can match two charts it may represent a similar set of emotions during those separate times, therefore leading to similar outcomes.

Probably what spooked me the most was this analog that I found:

Not only was Tesla trading in an similar overall pattern to Solarcity did before it collapsed, the most recent price action after support was broken were near identical. I discovered this before reading the excerpt from The Divde and suspected that short sellers were using similar tactics on Tesla as they did when they broke Solarcity. After reading it, I can say with near certainty that it is the case.

I suspect that if Tesla had made a turn lower from there it would have represented the bull narrative crumbling and the bear narrative taking on a life of its own - a self-fulfilling prophecy.

It DID NOT.

Profit and Beyond

As long as Tesla depends on access to capital to survive, it will have certain characteristics of a financial company - vulnerable to short sellers and market sentiment.(and often times market sentiment driven by short sellers) This was part of the downfall for Solarcity. Because of this, the Moody's downgrade(potentially brought on by short sellers) materially harmed Tesla by increasing its borrowing cost.

I believe a CEO should focus on running their company instead of worrying about stock price or short sellers.

The thing is though, I think when Elon Musk looks around, he realizes the greatest threat to his company is not the Mission E or Model 3 take rate or whatever. It is the massive amount of capital betting against him steered by bad actors with malicious intent and an incriminating history.

I think this is why after 15 years Tesla has now made profitability and positive cash flow such a priority, so much so that they are going to extraordinarily lengths to achieve it. By laying off 9% of the entire workforce while retaining all production personnel, the numbers could be as high as 20% for non-production. By cutting cap ex for all but the essentials, Elon stated that anything over $1 million has to be personally vetted by himself, and only cap ex for immediate(next 2 years iirc) needs will be approved.

Because the way to break from the short sellers influence is by becoming self sustaining. When you no longer need to sell stock to survive, you don't care how high or low your stock goes. When you no longer need to raise debt to survive, you don't care which agencies short sellers can manipulate.

Remember, these short sellers are not in because they think the stock is overvalued, instead they are trying to break Tesla during the times of distress. And even though they have been unsuccessful so far, they have caused material harm.

However, if Tesla becomes self sustaining, the shorts would lose their effect and therefore lose their purpose. It is my hope that once this happens the short interest will disperse and Tesla would be free from these attacks. I believe this will happen. However, I do fear that with the stakes so high, once they lose control of share price, they may instead move on the the next logical targets. Attacking demand - they already do this with the fires and autopilot incidents. Or even worse, attack the company and its people. Those are much harder to pull off compared to price/sentiment manipulation, and carry a lot more legal risk, so I hope for their sake it does not come to that.

Last bit is that, to be clear, even when Tesla becomes self sustaining, they will still raise tons of capital in the future, actually more than ever before(most likely debt at a favorable rate). Tesla has massive ambitions and even greater capital needs for 10 gigafactories and the pipeline of new products. I actually agree with Goldman that they will need at least $10 billion over the next few years. The difference is when you are a self sustaining company, you can raise capital on your own terms. And if the terms offered are unfavorable, you can simply move on and wait for a better opportunity. If there is a recession, Tesla can simply scale back or slow down. A company that is reliant on access to capital to survive is faced with tough decisions that could hurt the company/shareholders whenever its stock is down or yields are up. A company that is self sustaining can simply wait those tough times out. Because Tesla is going to need plenty of cheap capital to accomplish their mission statement: to accelerate the world's transition to sustainable energy.

Mod: This article and the responses generated huge interest, and subsequently a podcast. By request, here's that podcast done a couple of weeks after this original series of articles. --ggr

Blubrry PowerPress Player

Also, my view is that CEOs should focus on running their company instead of their stock price, because in the long run only the fundamentals matter. Elon Musk historically has commented on Tesla's stock price, but very sporadically. The infamous "tsunami of hurt", the "don't have any right to deserve" our current market cap etc. I haven't had a problem with it because its been sparse, he's been balanced, and honestly he's been accurate. But there has been a decided shift lately. His interest and rhetoric has been ramping up versus the short sellers, dating back almost a year ago but really reaching a crescendo this past month.

Initially, it made me a bit uncomfortable whenever he engaged short sellers. Again, focus on running the company and share price will follow. However, in recent weeks I came upon an excerpt from The Divide: American Injustice in the Age of the Wealth Gap by Matt Taibbi that was posted here on TMC that radically changed my view. I've attached this excerpt and strongly encourage any longs to read it, because it will give you newfound perspective on the events surrounding Tesla.

Brief synopsis:

In 2002, Canadian insurance company Fairfax Financial run by Prem Watsa decided to list on the NYSE. Watsa was a bit of a prodigy and is known as the "Canadian Warren Buffet". In the summer of 2002, investing legend who made his name exposing Enron, Jim Chanos, decided something was wrong at Fairfax and bet against it. Chanos evangelized his belief in Fairfax's shortcomings, and by the end of 2002 a slew of other hedge fund titans followed suit, including Steven Cohen, Dan Loeb, Adam Sender. This culminated on Jan 17, 2003 when an analyst report from investment bank Morgan Keegan asserted that Fairfax was under-reserved by $5 billion, making it insolvent. This sent the stock down 25% the next day. Extraordinarily, this report was written by a rookie analyst John Gwynn who just came from Trinity, one of the hedge funds who made a huge bet against Fairfax. The collective hedge funds may have initially genuinely believed that Fairfax was corrupt or incompetent, but their even stronger belief was that enough bad press and market momentum would crater the firm. Chanos' own words, "With a financial services company like Fairfax, it can all be self-fulfilling. If the market finally decides the glass isn't half full anymore, the trouble starts... you can see the stock go into a waterfall." That was supposed to happen with the Morgan Keegan analyst report, but it didn't. Questions surfaced about the accuracy of the $5 billion calculation, and in February 2003 Fairfax released a positive financial report that shot the stock back up. The shorts flipped out. In Dan Loeb's text conversation: "We need to speak to the rating agencies today... they could provide the downside catalyst."

Incredibly, over the next three years was stories of harassment of Fairfax workers, the CEO Prem Watsa, his wife, even his pastor. While this was happening Fairfax was besieged by accusations of fraud sent to rating agencies, regulators, even Fairfax's own business partners. Nearly all of these troubles could be traced back to Spyro Contogouris, a man hired by Chanos, Loeb, and Sender to "bring down Fairfax". Contogouris’s strategy would be to sink Fairfax by “closing access to the capital markets”—cutting off its access to funding by undermining its reputation. This was old-school Sun Tzu stuff, isolate-and-destroy tactics, “attacking by stratagem”: General Contogouris would cut off his enemy’s supply lines by, among other things, sullying the firm’s standing with ratings agencies and shareholders and others in a group he termed “FoF,” for “Friends of Fairfax.” He wanted to “get them where they eat,” cutting off their credit lines, particularly going after their ratings by agencies like A. M. Best. All this Contogouris promised to Chanos, Loeb, Sender, and others from the start. He pledged to “get the message of what I think is a massive fraud to these long term value holders” by creating a “crisis of confidence” that would frighten investors and “shake them out of the stock.

By late July in 2006, Fairfax really was on the verge of collapse. Its stock price was declining, long loyal shareholders were slowly departing, questions from rating agencies, its executives were under surveillance by the FBI, and it was receiving subpoenas from the SEC. Like any financial firm, an insurance company can quickly implode in a run-on-the-bank-like crisis of confidence, and if it did not answer its detractors soon its share price might crater and the firm might go out of business.

So Fairfax ultimately made the only move it had left, it sued. And merely filing it was what saved the firm. The detailed response about all the allegations spooked short investors who jumped on the bandwagon with Chanos and the rest. According to discovery materials, some of these investors were all but assured that Fairfax was about to be busted by authorities at any moment and was sure to go out of business. So when Fairfax was gearing up for a long legal battle instead of just rolling over, it didn't seem to be the behavior of a guilty company. The short sellers began to cover.

On June 23, 2006 Fairfax share price reached a low of $100.00. A month later, on July 26, 2006, they decided to fight back and file suit. On June 15, 2018, last Friday, Fairfax closed at an all time high of $775.19.

Solarcity

First we have to talk about Solarcity since that is where Chanos and some of these same bad actors started here. I know Einhorn is at least another hedge fund mogul who is also short Tesla.

Solarcity was in essence a financial company. They were an arbitrage firm that profited from the difference between their borrow rate and their leasing rate to their customers. Now there was a bunch of noise and opaque accounting about how shareholder value should be calculated, net present value, renewal rates etc. So you can argue that it was worth $30 a share, or $20, or $10. But as far as keeping its doors open, as long as it could continue to borrow, and at a lower rate than it leased(and all the costs associated), their business can be profitable and continue to run. And in theory, their borrow rate should be determined by their ability to service this debt. In reality, it was determined by the market's confidence in their ability to service this debt. Which is exactly where Chanos, like with Fairfax, began his attack.

When Chanos announced his short in August 2015, his thesis was that Solarcity was a subprime lender. That at any moment, Solarcity's customers could stop paying their bills. This was ignoring the fact that Solarcity customers had an average FICO score 750, compared to below 620 to be considered subprime. Not to mention unlike defaulting on a home mortgage, where when you are underwater enough it can make financial sense.(not to mention you still get to live there for months) Defaulting on payments to Solarcity would make no financial sense, because reverting back to your utility would cost more. That was the whole value proposition from Solarcity.

But that was not what this was about. Because Solarcity and the entire solar industry had real issues at that time, with huge uncertainty whether the Investment Tax Credit would get renewed, not to mention Sunedison collapse. Demand was uncertain, and Solarcity had to significantly cut back their growth, by half. The stock would have gone down with or without short sellers. But what Chanos was doing was exactly what he described in his own words about Fairfax. He was taking advantage of a bad situation, and using fear to create a "crisis of confidence". Solarcity, after all, was a financial company. And as Chanos knows too well, it becomes a self-fulfilling prophecy once investor confidence is broken.

The first highlighted area was when Chanos announced his short. Elon responded the next day and bought stock, as well as making a rebuttal on CNBC, iirc. The second highlighted area is an incredible similarity to the Fairfax story. Gordon Johnson, a solar analyst of Axiom Capital initiated coverage of Solarcity that day with a scathing Sell rating. This seem to set off the "waterfall" of Solarcity's decline. Over the next year, Johnson would publish report after report reiterating his bearish stance. This in itself isn't necessarily incriminating, perhaps he was even right. Since Tesla acquired Solarcity, Chanos moved his short onto TSLA. Curiously, Johnson is now no longer with Axiom and has moved to Vertical group. He is also now no longer a solar analyst and instead "specializes in Basic materials sector", which apparently also includes Tesla. He initiated coverage on April 9, 2018 with a Sell rating and currently is the owner of the lowest price target on the street at $99. He is constantly seen on CNBC, every time reiterating the brilliant Bob Lutz-esque thesis of how much Tesla loses for every car sold.

So how would Solarcity have looked today without these short sellers? Well we know that the two other installers, Vivint and Sunrun are alive and well. In fact, Sunrun, has a very similar business model to Solarcity, with the same opaque accounting regarding NPV and renewal rates. It did not even pivot to loans from leases like the others did to conserve cash. Sunrun is currently trading at an all time high.

Solarcity did have one major issue that was company specific. During this already difficult time for the entire industry, they were tied to the Buffalo Silevo plant, and all the cap ex costs associated. Would these costs have overwhelmed them? Could they have found financing to get them through? Especially now that we see the business model has proven viable after the fact? I don't know the answers to those questions. Perhaps they would have gone under either way. What I do know, or highly suspect, is that the negativity created by short sellers like Chanos and analysts like Johnson made certain that the capital markets were closed shut, to ensure that those questions never needed to be asked.

Solarcity is water under the bridge, and its fate debatable. But the same bad actors who attempted to take down Fairfax, the same bad actors who attempted and nearly(or perhaps they did) succeed in taking down Solarcity, have now moved on to Tesla.

Short interest

Tesla currently has close to 40 million shares or over $12 billion dollars betting against it. It is easy to conflate this with the litany of Tesla bears all over social media, twitter, seeking alpha, etc. Don't. These people may be responsible for 99% of the noise, but I highly doubt if they even amount to 10% of the short interest.

Historically in the stock market, a high short interest is actually bearish and indicative that something is wrong. (there are obviously great examples to the contrary, ie AMZN) And in general short sellers are considered more sophisticated than the average long, because they are mostly professional traders/fund managers vs retail investors. While there does seem to be an inordinate amount of "retail shorts" in Tesla, I believe the actual money amount is minimal compared to the real actors.

Over the past few years, there has been three significant spikes in short interest.

So the bear thesis ranges from Tesla is overvalued, to Tesla cannot make a profit(therefore doomed to bankruptcy), to now recently I'm hearing more that Tesla is fraudulent. As professional, sophisticated, presumably intelligent short sellers who believe in any of that, you would think they would short the most when the stock is high. After all, is Tesla not most overvalued when it is highest? Reality is not the case, in fact short interest is lowest at the peaks, and the three spikes in short interest all coincide with significant market declines. Now, it is easy to scoff at this and dismiss it as "dumb shorts" buying highs and selling the lows. I am sorry, but as a trader of many years, you cannot convince me that this is $12 billion of dumb money.

Moreover, the three spikes in short interest all coincide with specific events:

1. In early 2016 there was a market downturn that stemmed from declining high yield bonds that contributed to this. But also, it coincided with the Solarcity short seller attack described before. If Solarcity was forced into bankruptcy, they would have defaulted on their solar bonds that Spacex bought previously. All Elon Musk companies are connected, and all would have been harmed. It is almost as if it was a coordinated attack.

2. In late 2016, short interest rose to an all time high. I remember the negativity was overwhelming during this period. Constant negative media coverage and bearish articles/analyst reports. And then all of sudden, it all went away and the stock rallied. Do you remember what changed? Do you remember what those analyst reports and bearish articles were about? This was the lead up to the Solarcity/Tesla merger vote. The articles and analyst reports were about how Solarcity and its mountain of debt was about to drown Tesla. The outrage was over the lack of corporate governance and how bad a deal this was. The other major narrative was that the deal would not pass. Gordon Johnson rears his head again and declares there is only a 50/50 chance of Tesla shareholders approving. (SCTY), Tesla Motors, Inc. (NASDAQ:TSLA) - Gordon Johnson Warns Of 'Burgeoning Risk' To SolarCity/Tesla Deal Closure Jim Chanos went on CNBC, imploring Tesla shareholders to reject the deal since it was so terrible and would bring Tesla down with it.

And then, Nov 17, 2016, the vote passes. The stock literally bottoms three days before this, and proceeds to rally to all time highs. Media negativity was gone instantly after the vote. Analyst reports muted. Think about that for a second, and logically if it even makes sense. If this deal truly was so bad, if it was the down fall of Tesla, shouldn't the overwhelming negativity occur AFTER the deal closes? After all, now that it is official and Tesla is responsible for this huge debt burden, isn't Tesla doomed? Yet there was nothing. Almost as if the negativity was to shut the deal down.

3. In March 2018, short interest spiked to a new all time high, to its current levels. This coincided with the Moody's downgrade, and sudden questions over liquidity. Just as Tesla's most important product is about to ramp. Just as Tesla is about to take its biggest leap, become profitable and sustainable as a company, a new narrative emerges: Bankruptcy. I will talk about this more in followup post.

To reiterate my sentiments towards short selling. I have no qualms with market participants betting that a stock is overvalued. I have no problems with people betting that a stock will go bankrupt. I believe the majority of the Tesla bears on social media, with the highest visibility, fit into those groups. I believe they are misguided, but they have every right to risk their own money how they like.

However, it is my belief that the vast majority that encompass the $12 billion in short interest do not fit this. They are not chasing highs and selling lows because they are emotional retail investors. They are not shorting because they think Tesla is overvalued. They are not shorting because they think Tesla will go bankrupt. They are shorting during specific periods when Tesla is most vulnerable, and covering when they fail to achieve their targeted goal. They are shorting to bankrupt Tesla.

Moody's

Hopefully by now you have read the transcript that's linked. If so, you understand the depth that these people will go to. You understand that analyst reports are circulated before to be front-runned. You understand the rating agencies are mentioned by name and used as tools. But you also have to understand, Fairfax Financial was a relative unknown midsize firm from Canada. Tesla's short interest is the largest in the entire US stock market. What is at stake now is profoundly greater, what about the methods? Of course I can't know that for sure. But what we do know:

After the close on 3/27, Moody's downgraded Tesla's debt to B3, senior notes to Caa1, with outlook negative.

Before this happened, during the trading session on 3/27 Tesla was down $25 on double the average volume. In the prior 11 trading days, Tesla was down 10. Note that the stock market as a whole was also down during this period, but not to this extent and especially less so on 3/27.

The rationale behind Moody's downgrade:

Tesla's ratings reflect the significant shortfall in the production rate of the company's Model 3 electric vehicle. The company also faces liquidity pressures due to its large negative free cash flow and the pending maturities of convertible bonds ($230 million in November 2018 and $920 million in March 2019). Tesla produced only 2,425 Model 3s during the fourth quarter of 2017; it is currently targeting a weekly production rate of 2,500 by the end of March, and 5,000 per week by the end of June. This compares with the company's year-earlier production expectations of 5,000 per week by the end of 2017 and 10,000 by the end of 2018.

The negative outlook reflects the likelihood that Tesla will have to undertake a large, near-term capital raise in order to refund maturing obligations and avoid a liquidity short-fall. Prospects for addressing its liquidity requirements (whether equity, convertible notes or debt) will be supported if the company can establish credibility for reaching Model 3 production levels -- 2,500 per week by the end of March, and 5,000 per week by the end of June.

So the crux of the downgrade and especially the negative outlook revolved around the uncertainty of Tesla's production rate. It was stated that this could be alleviated if Tesla could hit its production targets by the end of March. Those precise production targets were set to be updated the very next week. Moody's could have waited less than one week to confirm their projections in order to make a more informed judgment. Yet for some reason they did not, and was determined to get this downgrade out.

The fallout after Moody's downgrade:

Tesla bond price plummeted to 87 cents on the dollar, while yields approached 8%. Just a few short months before this, Tesla sold these bonds paying 5.3%. At these new prohibitive rates, Tesla was essentially shut out of the debt markets. This was happening precisely during Tesla's cash "valley" before Model 3 ramps up. There was talk of a liquidity crisis, while JP Morgan started peddling Tesla "crash puts" below $100. JPMorgan Recommends Tesla ‘Crash Puts’ With Tail Risk Rising

I did not have a position in Tesla at this time, and I did not yet read the excerpt from the Divde. I am not sure if my reaction would have changed much if I had. I consider myself a conservative bull, and after reading this news I became more cautious on Tesla than ever before. I understood that nothing has changed with Tesla the company, but there are many things outside of Tesla's control. Markets create a narrative and it takes on a life of it's own, especially when it comes to liquidity issues. It becomes a self-fulfilling prophecy.

Self-fulfilling prophecy

This is not the case for every company. If McDonalds were shut off from the debt markets and capital markets, it would not matter because they have a sizable cash horde and positive cash flow. No matter the amount of fear generated in the markets, there is no "bank" to run-on.

This is why short sellers like Jim Chanos target financial and insurance companies, they are beholden to the capital markets, and in his own words, once you create a "crisis of confidence", the story plays itself out. Fairfax was this way. Solarcity, due to its financial model, was this way.

Tesla is this way as well, for now.

The day that Tesla announced the Gigafactory, in a way, it became like a financial company. This is because from then on they were tied to years of capital expenses without any immediate return. To expand the company on top of that, while developing and tooling up for the Model X, Tesla Energy, service centers and superchargers, while all this was paid for only by the Model S. The company could not possibly fund this on its own, so it has been depending on the capital markets since. The day after announcing the Gigafactory, TSLA hit $265. I don't think it was a coincidence that it spent the next three years largely below this level with only two brief stints up to $280s. I also don't think it was a coincidence that only after 1/4/17 when Tesla announced that the Gigafactory was finally online did share price eventually break through to a higher range. (there were other factors including Tencent investment and anticipation for Model 3).

However, due to Model 3 delays and the enormous costs associated with ramping, Tesla arrived at a "cash valley" right before Model 3 really ramps up. When you exacerbate this with the Moody's downgrade and shutting off the debt markets, Tesla once again is at a precarious position. I became extremely cautious because I've seen this movie before when a ratings downgrade leads to a liquidity event, which was exactly the intent here.

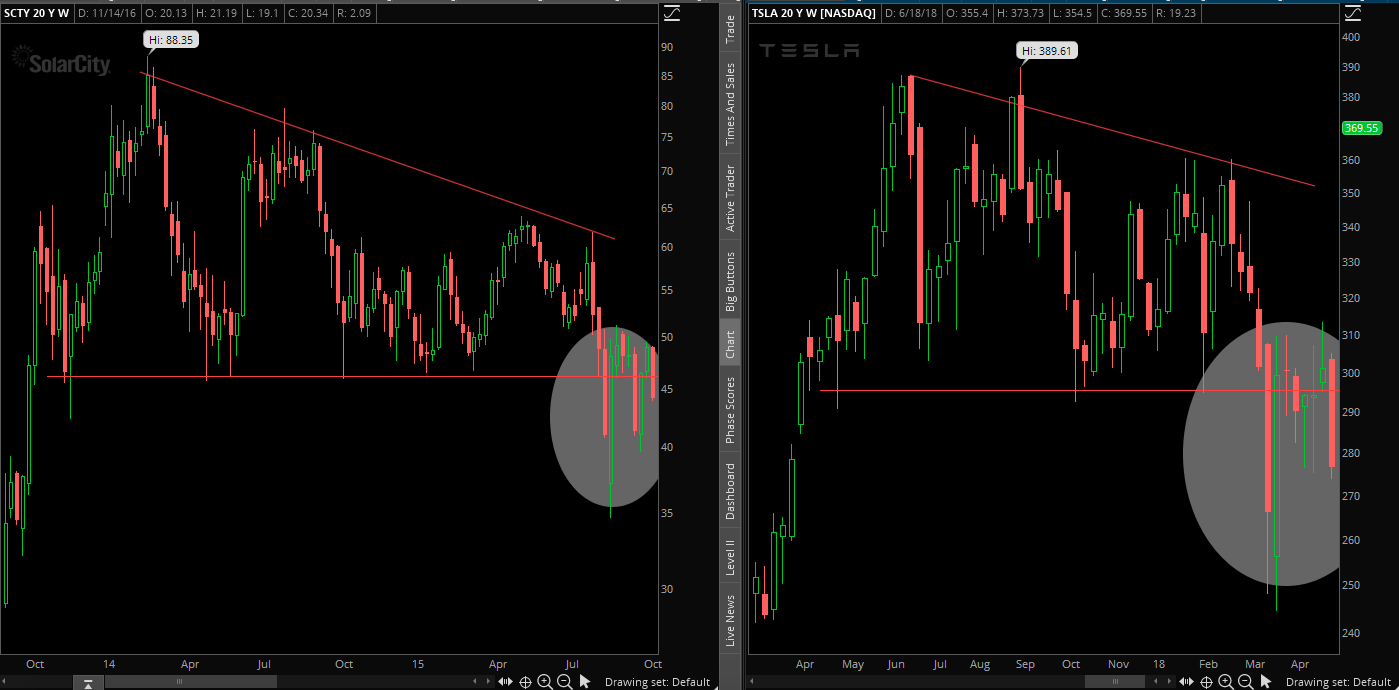

A little background: I am a trader for a living and often use something called an analog as a tool. It is a comparison of two charts that mirror eachother. The idea is that stock movement is largely emotion driven in the short run, and if you can match two charts it may represent a similar set of emotions during those separate times, therefore leading to similar outcomes.

Probably what spooked me the most was this analog that I found:

Not only was Tesla trading in an similar overall pattern to Solarcity did before it collapsed, the most recent price action after support was broken were near identical. I discovered this before reading the excerpt from The Divde and suspected that short sellers were using similar tactics on Tesla as they did when they broke Solarcity. After reading it, I can say with near certainty that it is the case.

I suspect that if Tesla had made a turn lower from there it would have represented the bull narrative crumbling and the bear narrative taking on a life of its own - a self-fulfilling prophecy.

It DID NOT.

Profit and Beyond

As long as Tesla depends on access to capital to survive, it will have certain characteristics of a financial company - vulnerable to short sellers and market sentiment.(and often times market sentiment driven by short sellers) This was part of the downfall for Solarcity. Because of this, the Moody's downgrade(potentially brought on by short sellers) materially harmed Tesla by increasing its borrowing cost.

I believe a CEO should focus on running their company instead of worrying about stock price or short sellers.

The thing is though, I think when Elon Musk looks around, he realizes the greatest threat to his company is not the Mission E or Model 3 take rate or whatever. It is the massive amount of capital betting against him steered by bad actors with malicious intent and an incriminating history.

I think this is why after 15 years Tesla has now made profitability and positive cash flow such a priority, so much so that they are going to extraordinarily lengths to achieve it. By laying off 9% of the entire workforce while retaining all production personnel, the numbers could be as high as 20% for non-production. By cutting cap ex for all but the essentials, Elon stated that anything over $1 million has to be personally vetted by himself, and only cap ex for immediate(next 2 years iirc) needs will be approved.

Because the way to break from the short sellers influence is by becoming self sustaining. When you no longer need to sell stock to survive, you don't care how high or low your stock goes. When you no longer need to raise debt to survive, you don't care which agencies short sellers can manipulate.

Remember, these short sellers are not in because they think the stock is overvalued, instead they are trying to break Tesla during the times of distress. And even though they have been unsuccessful so far, they have caused material harm.

However, if Tesla becomes self sustaining, the shorts would lose their effect and therefore lose their purpose. It is my hope that once this happens the short interest will disperse and Tesla would be free from these attacks. I believe this will happen. However, I do fear that with the stakes so high, once they lose control of share price, they may instead move on the the next logical targets. Attacking demand - they already do this with the fires and autopilot incidents. Or even worse, attack the company and its people. Those are much harder to pull off compared to price/sentiment manipulation, and carry a lot more legal risk, so I hope for their sake it does not come to that.

Last bit is that, to be clear, even when Tesla becomes self sustaining, they will still raise tons of capital in the future, actually more than ever before(most likely debt at a favorable rate). Tesla has massive ambitions and even greater capital needs for 10 gigafactories and the pipeline of new products. I actually agree with Goldman that they will need at least $10 billion over the next few years. The difference is when you are a self sustaining company, you can raise capital on your own terms. And if the terms offered are unfavorable, you can simply move on and wait for a better opportunity. If there is a recession, Tesla can simply scale back or slow down. A company that is reliant on access to capital to survive is faced with tough decisions that could hurt the company/shareholders whenever its stock is down or yields are up. A company that is self sustaining can simply wait those tough times out. Because Tesla is going to need plenty of cheap capital to accomplish their mission statement: to accelerate the world's transition to sustainable energy.

Mod: This article and the responses generated huge interest, and subsequently a podcast. By request, here's that podcast done a couple of weeks after this original series of articles. --ggr

Blubrry PowerPress Player

Attachments

Last edited: