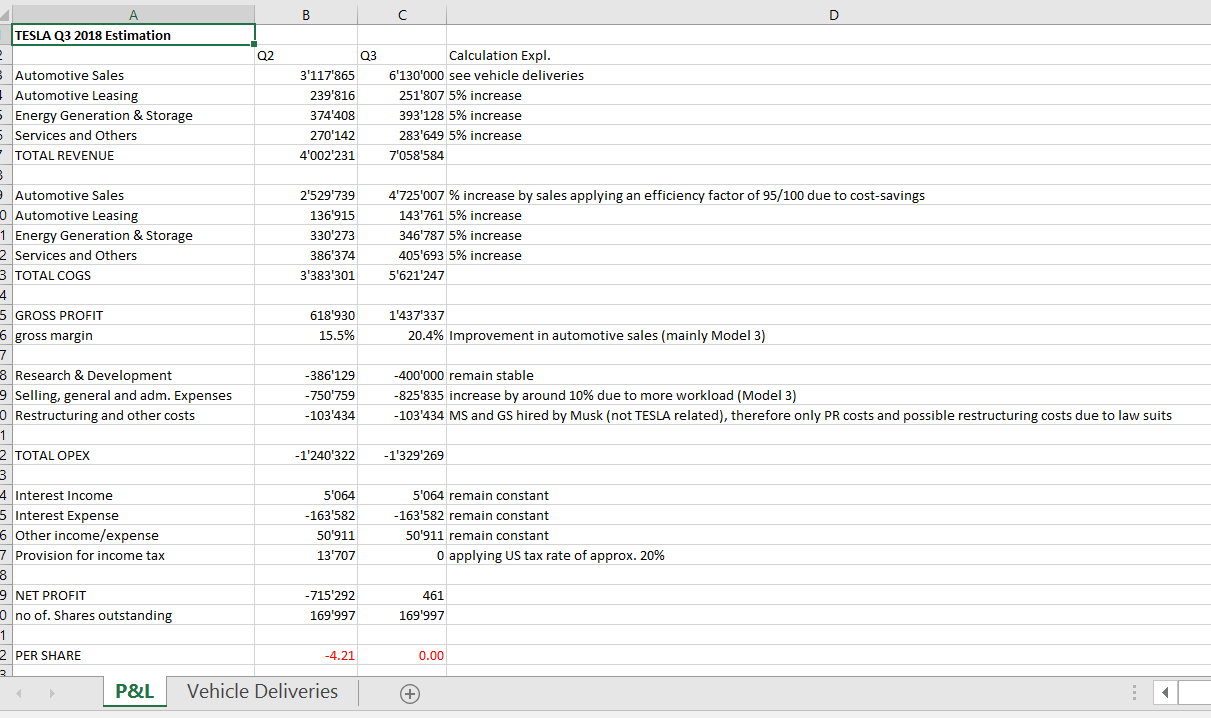

Tesla is doing over 7,000 a week now, they won't hit 300k this year but if you take July 1 2018 to June 30 2019 it'll be over 300k.

Just looking at Jan 1 2018 to Dec 31 2018 they'll break 200,000 manufactured and likely be over 200,000 delivered. Q1+Q2 = 87,833, meaning they have to make more than 112,167 in Q3 and Q4 but they've already more than tripled the pace for Q3 vs Q2 so that is a given.

Musk says Tesla pushed out 7,000 cars last week, meeting goal of 5,000 Model 3s

You'll have to wait for October to see the Q3 numbers but you can get a sneak peak by looking at

Tesla, Inc. - Wikipedia and

Monthly Plug-In Sales Scorecard

I wouldn't be surprised to see 90,000 to 100,000 S/X/3 for Q3 global deliveries. Which is on a 350,000 to 400,000 rate if you multiply by 4.

")