qdeathstar

Completely Serious

For something like a shipping container nuclear seems more feasible than wind, and that says more about the feasibility of wind than the feasibility of nuclear reactors on shipping vessels.

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

1) If you think nuclear reactors on land are expensive, try sending them to sea to really make your eyes water.For something like a shipping container nuclear seems more feasible than wind, and that says more about the feasibility of wind than the feasibility of nuclear reactors on shipping vessels.

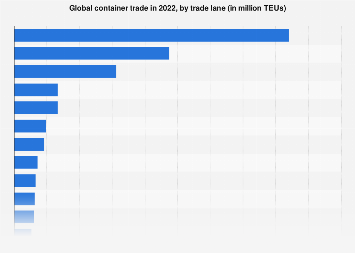

www.statista.com

www.statista.com

1) If you think nuclear reactors on land are expensive, try sending them to sea to really make your eyes water.

2) The world is only one new railway line away from there being a rail link that can substitute for all the Far East <> North America container trade, with little or no seafreight required (the Bering Strait connection). There is now sufficient potential in the existing Far East <> Europe rail lines to substitute for all the container traffic on that route. And I am continually putting up news items showing intra-Asia rail cargo links growing. By the way, the rail links are faster and can be 100% renewable. It is quite conceivable that long distance containerised seafreight is an endangered species. Just like we already know long distance seafreight of oil/gas/coal is very much an endangered species.

View attachment 882170

Global container trade by trade lane 2022 | Statista

Container trade flows within Asia reached an estimated volume of 42.1 million TEUs in 2022.

The qualitative point is very valid. It depends, and in any case I think we will get to the same place in carbon terms by way of (green) ammonia shipping in due course.There is a meme about the point you might want to investigate.

I do wonder how America will feel about being reliant on Russia for access to the world trading markets. Not to mention it would take 50 cargo trains to equal one cargo ship.

Interesting that interasia trade accounts for 1/2 of the worlds transport by sea, despite India and China being able to be connected by rail and rail being the panacea you think it is…

Sure we need to improve our rail system, but it’s no substitute for nuclear cargo ships

Yea, so you’d have to have multiple rail links over the bearing straight to avoid a choke point, and you’d need them spread so that there is redundancy. Then you’d have to double the number of trains and labor needed to operate the trains.The qualitative point is very valid. It depends, and in any case I think we will get to the same place in carbon terms by way of (green) ammonia shipping in due course.

The quantitative point is not at all valid. The loco & wagon fleets required are equivalent in size to those already in use within North America, or within Europe, i.e. business as usual.

I think the NS Savanah demonstrated the feasibililty of nuclear power for commercial merchant vessels. NS Savannah - Virtual Toursubstitute for nuclear cargo ships

Kite sails certainly are limited to tail winds but other sailing ships have been able to sail against the wind for a long time. Depending on sail size, many can sail fast with a beam wind (wind 90 degrees to direction of travel) than a tail wind.I don't see Sails making any meaningful contribution in power to any decently sized cargo ship. And that too only if it is a tail wind

The duel fuel ammonia moves are gathering pace*. Fleet owners are ordering vessels, bunkerage ports are ordering bunkerage facilities, and the manufacturers are ordering ammonia manufacturing kit. At a guess this will get adopted faster than biofuel. The handling limitations on ammonia are such that one doesn't really want it in widespread use by the general public (which rules out road vehicles). The corrosion issues are such that one doesn't really want to put it through the high stress areas of a gas turbine (which rules out aircraft).I think the NS Savanah demonstrated the feasibililty of nuclear power for commercial merchant vessels. NS Savannah - Virtual Tour

Essentially, that ship has sailed its last time.

Kite sails certainly are limited to tail winds but other sailing ships have been able to sail against the wind for a long time. Depending on sail size, many can sail fast with a beam wind (wind 90 degrees to direction of travel) than a tail wind.

I don't see either nuclear or sail replacing fuel and combustion for shipping any time soon. Biofuels are probably the only sustainable option in our lifetimes.

I'm not too familiar with the options for making ammonia. The only way I know of is starting with natural gas (methane) as is done in the fertilizer industry. This approach, however, releases all of the Carbon in the methane and that is usually emitted as CO2 so, other than reduced particulate emissions, it is hardly an improvement from use of oil for deep sea ships.deep sea commercial shipping goes to ammonia.

The pathway for green ammonia is :I'm not too familiar with the options for making ammonia. The only way I know of is starting with natural gas (methane) as is done in the fertilizer industry. This approach, however, releases all of the Carbon in the methane and that is usually emitted as CO2 so, other than reduced particulate emissions, it is hardly an improvement from use of oil for deep sea ships.

Are there better ways to produce ammonia that are viable?

www.energymonitor.ai

www.energymonitor.ai

You need to do some math (and some googling): Typical container ship uses 56 MW to cruise at 24 knots. At 10 acres per MW, that's 560 acres of solar panels to power that ship (until the sun goes down). Then you STILL need batteries, AND 2x the no. of solar panels to both charge the batteries during the day, and propel the ship.

Care to guess the horizontal area (in acres) of a New Panamax ship?

1400 ft * 180 ft = 5.78 acres

So a solar array which entirely covers a Panamax ship could provide < 1% of the power required to propel it, and only while the sun is up.

BTW, a Panamax ship is NOT a typical container ship, so power required is even more than this estimate - call it about 1 Section of land (4 quarter-sections), or 2 sections with night running on batteries.

Not sure that Tesla will bother with ships. Elon thinks it is a simple engineering task and beneath him. I like the idea in the same way that I like mega packs. It would be a way for Elon to order even more batteries and raw materials to ensure that the premium products like cars never run out.

No don’t. Let’s leave some places in the world pristine without humans driving their monster equipment through and cutting down trees and bisecting and dividing the region with these roadways.Run down through the Darien

www.marinelink.com

www.marinelink.com

Mind you, the sums for intercontinental rail look equally competitive.

Trains are an interesting case. Each loco has ~3.7 MW drive unit (typically 2-3 locos per train), so that's very neatly about 1 Megapack container per hour per engine at max power output. Container wagons come in 2-3 TEU capacities, while each train can carry an average capacity of 66 TEUs per trip (Woodburn, 2011). So payload and range of a battery powered train depends strongly upon the average power demanded of the engines. Electric powertrain has the advantage of efficiency and minimal engineering effort required to fully convert from diesel-electric drive to battery-electric. Diesel-electric already achieves ~500 mpg/ton of cargo (better than a diesel Semi, which may achieve ~300 mpg/ton, based on 7.5 mpg and 40 ton payload). But train transport often requires a Semi for depot delivery.

As for delivering Megapack itself from the port of arrival (or from the Megafactory, if on the continental road network) each Megapack can provide ~3.9 MWh of energy to the tractor, Tesla Semi/trailer can haul that Megapack (0.9+3.9)*500 = 2,400 miles before both the Megapack and the Semi's batteries are depleted. Of course, you'd "Platoon" those truck deliveries (most sites likely to require >3 Megapacks) so that highway range could be stretched slightly due to aero (perhaps +10%). That's the distance between Lathrop, CA and New York City (2,278 mi), or only 1,750 miles from Giga Texas.

P.S. the possibility of adding REGEN BRAKING to the net efficiency of a 20,000 ton train should not be taken LIGHTLY!