No visual data is being collected. Can't be done over CAN, it is very low bandwidth and very few bits are programmable.they're collecting visual data about road markings, traffic signs, and are also sending CANbus data. How they take visual data from the cameras and convert it into 10kb per kilometer, I have no idea.

Mobileye could be flagging and classifying road data like signs and encoding the type and location, but that is it.

I'd love to see Mobileye improve their data collection and demonstrate it, but when I worked with them it was like pulling teeth for them to innovate.

Edit: I'm done clogging this thread with this conversation. Take it to the engineering thread in the future.

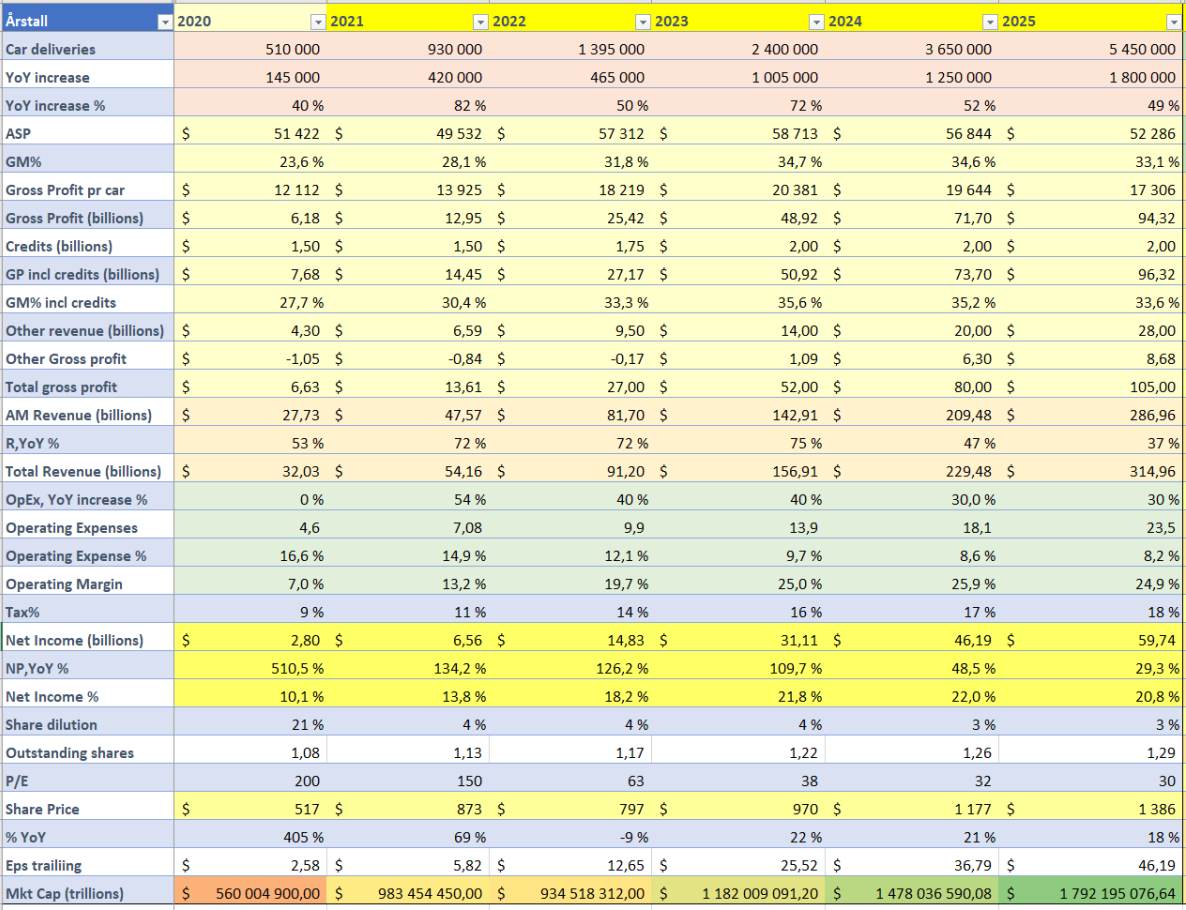

Let's just say, I very much disagree with those share price numbers. I also disagree with the dilution amounts per year. 2020 and 2021 were heavily influenced by Elon's compensation plan, dilution going forward will likely be 2% or 0% if Tesla does just a minor stock buy back

Let's just say, I very much disagree with those share price numbers. I also disagree with the dilution amounts per year. 2020 and 2021 were heavily influenced by Elon's compensation plan, dilution going forward will likely be 2% or 0% if Tesla does just a minor stock buy back

!

! Because I mean, 970$ for next year and 1,386$ by 2025 seems kind of low.

Because I mean, 970$ for next year and 1,386$ by 2025 seems kind of low.

PE isn't saying much of how they're actually performing (only how bullish people are for the next 5+ years).

PE isn't saying much of how they're actually performing (only how bullish people are for the next 5+ years).