No. It's not Trump, it's the Federal Reserve making the V shaped recovery possible. He is going to try and take credit for it of course.

(Not picking on you

@ripper88 - just using your post as a jumping off point)

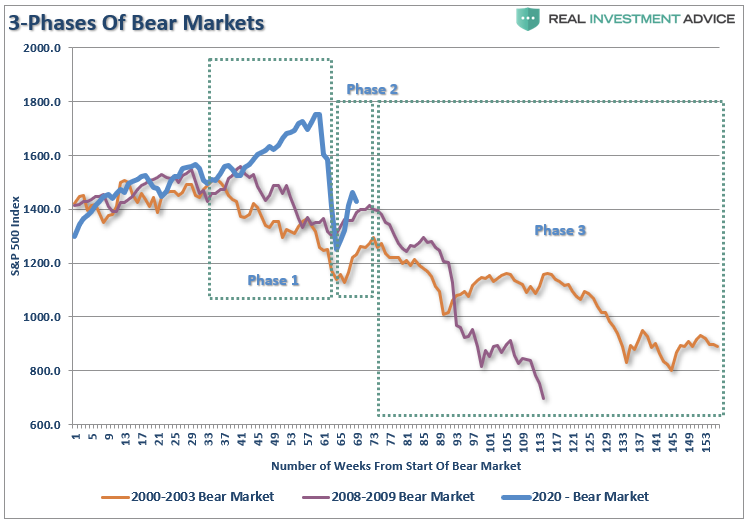

I see the v-shaped recovery in the stock market. I don't see the v-shaped recovery in the economy.

So that's what has me cautious (and still in cash, outside of TSLA). I am looking for evidence of the economy improving to match up with the stock market, or the stock market coming down to better match up with the economy. That's my choice of course, and it's more than a guess - it's what I'm doing with my portfolio (so I have $ in it).

An observation in another thread that was eye-opening for me; an economics thread, talking about MMT and other schools of economic thought. The observation is that no, there isn't inflation in our commonly used measure of inflation. The problem is that measure of inflation is a restricted view into the world - it focuses on 'core' stuff (energy, food, clothing, housing) for living. It doesn't include rare art, stock market, commodities, high tech, etc..

There is inflation going on in the world, and it's going on in the stock market right now (or at least, I agree with that observation). So it's possible that this time is different, and that the value of $1 of earnings per share is changing to a new baseline from what it's been historically. It's possible that the long term risk free rate of return is going to be ~0%.

I even subscribe to the notion that we're at the start of a pretty significant reset in our economy similar to the what we experienced in the late 1800s, early 1900s, with that wave of new technologies that so radically changed society and the economy. Cars, electricity, telegraph / telephone. We pretty much hit the trinity of the basis for economic activity (communication, energy, transportation).

I see the internet as being our new communication revolution, with it bringing us approximately zero marginal cost communication.

I see renewable energy bringing us approximately zero marginal cost energy (we've got a few decades for this to manifest, but the cost of energy in the economy is going to be falling steady during that period).

We don't yet have a comparable change in transportation starting, though lower energy cost will help, and autonomous vehicles might bring us approximately zero marginal cost ground transportation (due to the approximately zero marginal cost energy).

EDIT: And the combination of these things will bring about a period of good deflation - cost to get things done in the economy will come down, enabling new economic activity not previously available.

Anyway - back to the original point - maybe those historical measures of valuation and market health are going to revert to their historical values, and maybe they're establishing a new normal. I don't know of course, but I'm positioned assuming regression to something closer to the historical values.