In the interview Elon reiterated the aspiration to get to an annual vehicle production rate of 20 million. At a 50% growth rate, Tesla should be there by 2030. Despite being an automotive podcast, I wish Jason had asked a few questions about the energy side of Tesla's business. Still, it was an excellent interview and he did ask a lot of difficult questions especially in this third part.

Welcome to Tesla Motors Club

Discuss Tesla's Model S, Model 3, Model X, Model Y, Cybertruck, Roadster and More.

Register

Install the app

How to install the app on iOS

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

-

Want to remove ads? Register an account and login to see fewer ads, and become a Supporting Member to remove almost all ads.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Tesla, TSLA & the Investment World: the Perpetual Investors' Roundtable

- Thread starter AudubonB

- Start date

StealthP3D

Well-Known Member

In the interview Elon reiterated the aspiration to get to an annual vehicle production rate of 20 million. At a 50% growth rate, Tesla should be there by 2030. Despite being an automotive podcast, I wish Jason had asked a few questions about the energy side of Tesla's business. Still, it was an excellent interview and he did ask a lot of difficult questions especially in this third part.

Global car sales peaked in 2018 at 79 million. I expect them to continue to slide or maintain about that level over the next decade. 20 million cars would be over 20% of the total which I think is very doable.

Criscmt

Member

Subject: Trading around MMD

I did notice a few messages on this thread indicating some trading around MMDs.

I was wondering how you approach this? What influence your buy and sell timings.

For example, are technicals (mid-BB) part of the factors considered? Do you wait for a 1-2% drop to see it as a selling point? @Artful Dodger ?

I am not referring to those instances where you "just buy" on the dips, even if dip that's part of MMD.

One approach that crossed my mind is to stay with TSLA all the time (buy or sell). Switching between options/LEAPs with higher, lower deltas is one way to do this. Switch to relatively longer dated LEAP at sell points and to shorter date LEAP (let's say at same strike price) at buy point.

I have been HODLer for years, recently got into LEAPs where I did ok, and very recently into shorter-term options where I burnt my fingers.

I am not a trader, nor have any inclination to take steps in that direction.

That said, the whole MMD is tempting me into playing a minor amount around that pattern(deceit by MMs).

I did notice a few messages on this thread indicating some trading around MMDs.

I was wondering how you approach this? What influence your buy and sell timings.

For example, are technicals (mid-BB) part of the factors considered? Do you wait for a 1-2% drop to see it as a selling point? @Artful Dodger ?

I am not referring to those instances where you "just buy" on the dips, even if dip that's part of MMD.

One approach that crossed my mind is to stay with TSLA all the time (buy or sell). Switching between options/LEAPs with higher, lower deltas is one way to do this. Switch to relatively longer dated LEAP at sell points and to shorter date LEAP (let's say at same strike price) at buy point.

I have been HODLer for years, recently got into LEAPs where I did ok, and very recently into shorter-term options where I burnt my fingers.

I am not a trader, nor have any inclination to take steps in that direction.

That said, the whole MMD is tempting me into playing a minor amount around that pattern(deceit by MMs).

Global car sales peaked in 2018 at 79 million. I expect them to continue to slide or maintain about that level over the next decade. 20 million cars would be over 20% of the total which I think is very doable.

The 20 million number came from wanting to replace 1% of the global fleet per year.

Global car sales peaked in 2018 at 79 million. I expect them to continue to slide or maintain about that level over the next decade. 20 million cars would be over 20% of the total which I think is very doable.

Let's say Tesla car insurance takes off and gets 10% of that...

Driver Dave

Member

It feels like the SP is stepping down a notch to let more people get on before the next journey.

Like a kneeling bus.

Like a kneeling bus.

Sudre

Active Member

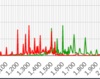

Looks like this week there are no significant Call strikes under 1500. Max Pain is at 1500.

How is that for grains of salt for you. All the volume today is hanging around the 1500 range on options. I think this is just everyone waiting for something to happen.

How is that for grains of salt for you. All the volume today is hanging around the 1500 range on options. I think this is just everyone waiting for something to happen.

Attachments

Tslynk67

Well-Known Member

Looks like this week there are no significant Call strikes under 1500. Max Pain is at 1500.

How is that for grains of salt for you. All the volume today is hanging around the 1500 range on options. I think this is just everyone waiting for something to happen.

Yup, someone please announce *something* for crying out loud...

This is another area that I disagree with common financial "wisdom". I've been retired for over 20 years without any income other than a small amount of dividend income that is mostly incidental. And I'm only 57 now so I still have a long ways to go (I hope). If I had retired with the plan to live off dividends, etc. I could have done that but I would of had to sell off most of my investments and buy dividend bearing stocks and/or bonds, annuities, etc. I could not have spent at the same level as I did. It's more capital efficient to make income from capital appreciation and continually sell off a small percentage of your stock (profit taking) and consider that your income.

It's a false distinction to create an imaginary line between income and capital appreciation. It's all capital, make it work for you. In retirement it's normal to spend down your capital. Ours has been increasing over the years even though our lifestyle is far from minimalistic. I attribute this to NOT making a false distinction between income and capital appreciation.

Not to mention that capital gains are usually more tax efficient than dividends.

J

jbcarioca

Guest

the most part these are CCS+CHAdeMO so the standard EU CCS should work fine. For some time the Moscow Tesla Club had at least two Superchargers, with at least some stations accepting both US and EU style plugs, as most EU Superchargers do. A quick check with the Moscow Tesla Club will give current information.I'm over-reliant on A Better Route Planner. Interesting... I wonder what the limit is now in terms of going east from Western Europe. At what point do I need to use the CCS/China (GB/T?) connector? (does it exist?)

I'm wondering if (in a few years) - fully possible to travel trans-siberian > Mongolia > China type routes.

I'll stick to Europe for now.

Jack6591

Active Member

This is another area that I disagree with common financial "wisdom". I've been retired for over 20 years without any income other than a small amount of dividend income that is mostly incidental. And I'm only 57 now so I still have a long ways to go (I hope). If I had retired with the plan to live off dividends, etc. I could have done that but I would of had to sell off most of my investments and buy dividend bearing stocks and/or bonds, annuities, etc. I could not have spent at the same level as I did. It's more capital efficient to make income from capital appreciation and continually sell off a small percentage of your stock (profit taking) and consider that your income.

It's a false distinction to create an imaginary line between income and capital appreciation. It's all capital, make it work for you. In retirement it's normal to spend down your capital. Ours has been increasing over the years even though our lifestyle is far from minimalistic. I attribute this to NOT making a false distinction between income and capital appreciation.

If I had a mulligan on any life decision, it would be retirement age. I wish I had retired much sooner.

@StealthP3D Great choice.

Edit: I misspoke, my official retirement date is 1 September 2020.

Hear me out guys.. Why doesn't Tesla buy TikTok?

1) China loves Tesla and Elon Musk

2) Elon Musk wants to get to Mars; he needs social media FU resources to expedite this

3) Elon Musk loves social media; why not own your own company?

1) China loves Tesla and Elon Musk

2) Elon Musk wants to get to Mars; he needs social media FU resources to expedite this

3) Elon Musk loves social media; why not own your own company?

Yeah I'm getting sleepy.Yup, someone please announce *something* for crying out loud...

.gif")

Motor Mouth

Member

No. Has nothing to do with the mission.Hear me out guys.. Why doesn't Tesla buy TikTok?

1) China loves Tesla and Elon Musk

2) Elon Musk wants to get to Mars; he needs social media FU resources to expedite this

3) Elon Musk loves social media; why not own your own company?

I am going to take a nap!Yup, someone please announce *something* for crying out loud...

Is that when S&P inclusion is going to be announced?If I had a mulligan on any life decision, it would be retirement age. I wish I had retired much sooner.

@StealthP3D Great choice.

Edit: I misspoke, my official retirement date is 1 September 2020.

")

ByeByeJohnny

Active Member

About friggin time we get some new cars to Europe. TT, the Swedish version of AP just put out an article about how Tesla only sold 11 cars in all of July here. The only explanation they gave was that the factory had been partially closed because of Corona. Guess they had no idea there are no Teslas available to buy in the country. Looking at the site now there are zero S or X listed and every single 3 listed is listed as being 'under transport' so I assume they are on the ship arriving to Europe tomorrow.

My second Model 3 is probably on that ship

Tes La Ferrari

Active Member

I hope everything works out for you and your significant other. I am sure you have shared many memorable memories. I have this quote a good friend sent me and every time we encounter bad situations, i look at it, sometimes more than once:

View attachment 572286

aka HODL’ing in your marriage.

just make sure your partner is a TSLA and not a NKLA.

Similar threads

- Locked

- Replies

- 0

- Views

- 3K

- Locked

- Replies

- 0

- Views

- 6K

- Locked

- Replies

- 11

- Views

- 10K

- Replies

- 6

- Views

- 5K

- Locked

- Poll

- Replies

- 1

- Views

- 12K