Housing sales is collapsing before our eyes as rising interest rates are killing the market which was already very overheated.

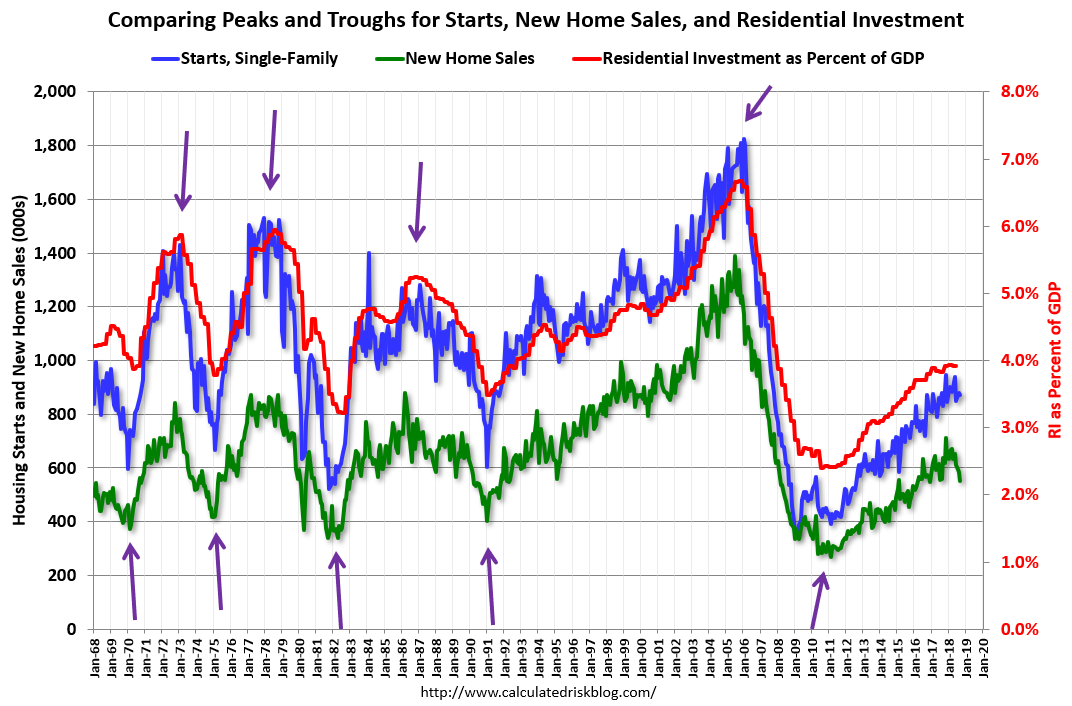

Note that even with yesterday's surprise weakening of the housing market it's still very, very far away from bubble levels that would get the Fed worried:

I.e. the housing decline isn't large (yet) in historic terms and it's very far from 'collapsing'.

Also note the currently very low Residential Investments percentage, there's been past recessions where the

bottom of the recession had similar levels as we have today. I.e. housing has a lot of room to go up, and the economy is far from overheated (tech and finance kind of skewed growth up but that's easily fixed with sector specific market corrections) and it would be surprising to see a broad based economic downturn from here.

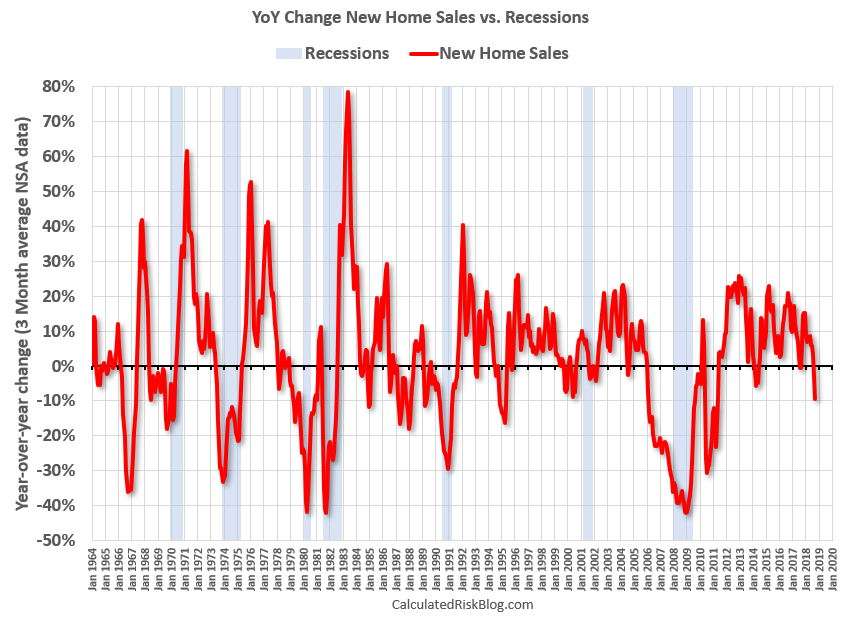

Also note the level of drop compared to drops before recessions:

In particular note the 80's and 90's drops that went deeper than the current drop and didn't result in a recession.

My expectation is that the Fed is probably going to slow down with the rate increases a bit to accommodate for the softening of the housing market - or at least tone down the hawkish language a bit, if inflation permits which it does currently.

Of course you never know with the Fed so a recession is still a possible outcome - but it's not a certainty at all at this point.

Also note that compared to traditional automakers Tesla possibly has a lot

higher recession resistance - we might even go as far and declare Tesla's business model counter-cyclical: a recession would allow Tesla to grow

even faster, because they are supply constrained, and because ICE carmakers wouldn't be able to invest into their EV conversion efforts as much, and because fire-sales of ICE car factory buildings and tens of thousands of expert auto workers to hire would speed up Tesla's growth as well.

Now that Tesla has earned enough cash in Q3 alone to pay back the $920m notes in March 2019 I think we can probably lean back and not worry too much about recessions.

")