You mean Santa Cruz?A 7 on the Hayward fault would be significantly closer to a major metro area than the Loma Prieta quake. Loma Prieta devastated Santa Clara, but it was some distance from the major cities of the Bay Area.

Welcome to Tesla Motors Club

Discuss Tesla's Model S, Model 3, Model X, Model Y, Cybertruck, Roadster and More.

Register

Install the app

How to install the app on iOS

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

-

Want to remove ads? Register an account and login to see fewer ads, and become a Supporting Member to remove almost all ads.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Long-Term Fundamentals of Tesla Motors (TSLA)

- Thread starter Robert.Boston

- Start date

-

- Tags

- elon is an ass investing TSLA

You mean Santa Cruz?

Whoops your right. I knew something was off when I wrote that but couldn't put my finger on it.

tftf

Member

Tesla's debt obligations and debt schedule...

$TSLA Debt Expiration Schedule, $MM What scares me the most is SolarCity toxic balance sheet full of leased assets, cash equity debt, etc. Moreover, $TSLA pledged $4.0 billion dollars worth of assets as collateral under debt obligations.

Source: Andrew Zakharov on Twitter

$TSLA Debt Expiration Schedule, $MM What scares me the most is SolarCity toxic balance sheet full of leased assets, cash equity debt, etc. Moreover, $TSLA pledged $4.0 billion dollars worth of assets as collateral under debt obligations.

Source: Andrew Zakharov on Twitter

neroden

Model S Owner and Frustrated Tesla Fan

I spent a while diving deep into SolarCity's balance sheet back before the merger. It's not toxic. It's just unreadable. It's actually all worth a lot more than it's carried at under GAAP.

The problem with SolarCity was that they were running a banking business: short-term borrowing financing long-term loans. They started dismantling this business a year before the merger, and it's taking a long time, but it looks to me like the portfolio is nearly all maturity-matched at this point. I look forward to a continuing decrease in the number of leases, though.

The non-recourse debt wouldn't have been on the balance sheet at all on pre-2008 accounting. Basically the only risk there is borrower default (which is why it now has to be on the balance sheet). But we have evidence that that's low.

For the recourse debt as long as Tesla is showing profits before March 2019, they'll be able to refinance all the recourse debt -- but in fact a bunch of it will probably convert to equity.

Musk outright stated that Tesla would be profitable in Q3 + Q4, which isn't normal for him, and could expose him to *serious* lawsuits if he was wrong.

Obviously, if there's some sort of crazy problem with the Model 3 rampup and they aren't showing profits in Q3 and Q4... then the refinancing becomes a problem.

The problem with SolarCity was that they were running a banking business: short-term borrowing financing long-term loans. They started dismantling this business a year before the merger, and it's taking a long time, but it looks to me like the portfolio is nearly all maturity-matched at this point. I look forward to a continuing decrease in the number of leases, though.

The non-recourse debt wouldn't have been on the balance sheet at all on pre-2008 accounting. Basically the only risk there is borrower default (which is why it now has to be on the balance sheet). But we have evidence that that's low.

For the recourse debt as long as Tesla is showing profits before March 2019, they'll be able to refinance all the recourse debt -- but in fact a bunch of it will probably convert to equity.

Musk outright stated that Tesla would be profitable in Q3 + Q4, which isn't normal for him, and could expose him to *serious* lawsuits if he was wrong.

Obviously, if there's some sort of crazy problem with the Model 3 rampup and they aren't showing profits in Q3 and Q4... then the refinancing becomes a problem.

Last edited:

MacRocket

Faster than Falcon 9

I have been wondering a lot lately how TSLA would perform in a recession?

Recessions usually start when consumers lose confidence in the economy and slow or stop spending.

This causes company sales and profits to fall resulting in lower share prices. A secondary effect occurs when companies have to reduce prices due to increased competition in a shrinking market. This causes further share price decline and further loss of confidence.

Companies supplying essential services to governments or utilities etc usually do best in a recession as sales in these areas don’t suffer much. Banks and consumer discressionary usually do worst (you don’t need that loan and no you can’t have that dress, have to keep the car going another couple of years too).

So, what happens to TSLA?

Innitially with recessions SP of all companies fall. Some companies will go out of business while others will do OK. The SP of the OK batch of companies will rise as investors get better than expected earnings reports. You won’t see bull market valuations but the money will move from the going bust lot do the doing OK lot, who incidently, probably have real businesses producing real things.

TSLA falls into this latter category.

Tesla energy is a utility business supplying fuel for transport (electricity) and battery storage to other utilities and governments. This market will still exist in a recession.

Tesla Semi will prosper as transport is cut throat in a recession. Companies will look to cut any way they can in hard times,- Tesla Semi will rock.

What about the car business you ask?

Tesla has 500,000 orders for model 3 and large pent up demand for model Y. Worst case scenario. Tesla loses half its model 3 orders in a recession due to one reason or another. They would still have 250,000 orders and with some new orders continuing to flow in (even in a recession) Tesla would take another 2 years to clear the backlog.

In other words the Tesla Auto business would continue to grow strongly.

But the car market will be shrinking you say. Yes this is true. Legacy ICE

Car manufacturers will be decimated.

They will be hit with increased Tesla competition and a shrinking market.

TSLA margins will not suffer as demand will outstrip supply for many years to come.

What about other EV’s?

They are 10 years behind Tesla and will never catch up. Tesla has the batteries (with a new secret sauce it is rumoured), the best auto pilot IMO and the best overall tech running their cars. Not to mention their advanced manufacturing (they will get there)

Well, I’ staying long for 20 years, I can’t imagine a better company to sit out a recession with.

Recessions usually start when consumers lose confidence in the economy and slow or stop spending.

This causes company sales and profits to fall resulting in lower share prices. A secondary effect occurs when companies have to reduce prices due to increased competition in a shrinking market. This causes further share price decline and further loss of confidence.

Companies supplying essential services to governments or utilities etc usually do best in a recession as sales in these areas don’t suffer much. Banks and consumer discressionary usually do worst (you don’t need that loan and no you can’t have that dress, have to keep the car going another couple of years too).

So, what happens to TSLA?

Innitially with recessions SP of all companies fall. Some companies will go out of business while others will do OK. The SP of the OK batch of companies will rise as investors get better than expected earnings reports. You won’t see bull market valuations but the money will move from the going bust lot do the doing OK lot, who incidently, probably have real businesses producing real things.

TSLA falls into this latter category.

Tesla energy is a utility business supplying fuel for transport (electricity) and battery storage to other utilities and governments. This market will still exist in a recession.

Tesla Semi will prosper as transport is cut throat in a recession. Companies will look to cut any way they can in hard times,- Tesla Semi will rock.

What about the car business you ask?

Tesla has 500,000 orders for model 3 and large pent up demand for model Y. Worst case scenario. Tesla loses half its model 3 orders in a recession due to one reason or another. They would still have 250,000 orders and with some new orders continuing to flow in (even in a recession) Tesla would take another 2 years to clear the backlog.

In other words the Tesla Auto business would continue to grow strongly.

But the car market will be shrinking you say. Yes this is true. Legacy ICE

Car manufacturers will be decimated.

They will be hit with increased Tesla competition and a shrinking market.

TSLA margins will not suffer as demand will outstrip supply for many years to come.

What about other EV’s?

They are 10 years behind Tesla and will never catch up. Tesla has the batteries (with a new secret sauce it is rumoured), the best auto pilot IMO and the best overall tech running their cars. Not to mention their advanced manufacturing (they will get there)

Well, I’ staying long for 20 years, I can’t imagine a better company to sit out a recession with.

Well, I’ staying long for 20 years, I can’t imagine a better company to sit out a recession with.

I don't have 20 years, maybe five. Perhaps there's current evidence of our optimism.

I'm not good at statistics but I do have a spreadsheet on our portfolio with a column devoted to percentage gain/loss compared to the average of three relevant large cap indices. By casual inspection, sometimes there's a macro market slump, yet we gain a lot over the market (or fewer losses) with TSLA. Combined TSLA and BIDU total almost 60% of our holdings. I didn't plan it that way; things just got out of control much to the consternation of our wealth manager when I buy slivers more of TSLA.

sdtslafan

Member

I'm trying to better understand Tesla's valuation compared to Netflix and what Tesla's share price could potentially be if it overcomes current hurdles.

Netflix is aiming for $15 Billion in revenue this year.

Very conservatively, Tesla will have similar revenue (probably more).

Netflix is making minimal profit, PE 223, so less than 1 B / year. Tesla is losing money but is spending huge amounts on capital investment for the future.

Tesla revenue will likely grow faster than Netflix.

Why is NFLX valued 3x more than TSLA?

Tesla needs to prove it can produce the 3 at scale, with good margins, and be able to use this money to fund growth rather than through capital raises. There is some uncertainty if whether Tesla can do this and I think that is understandable. But, if Tesla can do this, I don't see why it could 't be valued similar to NFLX in terms of 150B valuation, share price $800-900.

The reason the stock is trading at 290 is that most people don't believe Tesla can deliver on its promises. What are your thoughts?

Netflix is aiming for $15 Billion in revenue this year.

Very conservatively, Tesla will have similar revenue (probably more).

Netflix is making minimal profit, PE 223, so less than 1 B / year. Tesla is losing money but is spending huge amounts on capital investment for the future.

Tesla revenue will likely grow faster than Netflix.

Why is NFLX valued 3x more than TSLA?

Tesla needs to prove it can produce the 3 at scale, with good margins, and be able to use this money to fund growth rather than through capital raises. There is some uncertainty if whether Tesla can do this and I think that is understandable. But, if Tesla can do this, I don't see why it could 't be valued similar to NFLX in terms of 150B valuation, share price $800-900.

The reason the stock is trading at 290 is that most people don't believe Tesla can deliver on its promises. What are your thoughts?

I'm trying to better understand Tesla's valuation compared to Netflix and what Tesla's share price could potentially be if it overcomes current hurdles.

Netflix is aiming for $15 Billion in revenue this year.

Very conservatively, Tesla will have similar revenue (probably more).

Netflix is making minimal profit, PE 223, so less than 1 B / year. Tesla is losing money but is spending huge amounts on capital investment for the future.

Tesla revenue will likely grow faster than Netflix.

Why is NFLX valued 3x more than TSLA?

Tesla needs to prove it can produce the 3 at scale, with good margins, and be able to use this money to fund growth rather than through capital raises. There is some uncertainty if whether Tesla can do this and I think that is understandable. But, if Tesla can do this, I don't see why it could 't be valued similar to NFLX in terms of 150B valuation, share price $800-900.

The reason the stock is trading at 290 is that most people don't believe Tesla can deliver on its promises. What are your thoughts?

- Less capital expensive : there isn't any infrastructure needed : factories, service centers, ...

- More spread out : Netflix is in almost each household, whereas tons of people still don't know what a Tesla is.

So basically Netflix is less scary, and more popular (in the sense of awareness) than Tesla.

sdtslafan

Member

- Less capital expensive : there isn't any infrastructure needed : factories, service centers, ...

- More spread out : Netflix is in almost each household, whereas tons of people still don't know what a Tesla is.

So basically Netflix is less scary, and more popular (in the sense of awareness) than Tesla.

Thanks.

Understood, but isn't content capital expensive (to the tune of 7-8 Billion this year)?

And isn't Tesla's potential for growth much bigger?

I understand your point. It is so important that Tesla gets good at manufacturing a car that is so reliable it rarely needs to go to a service center. This could make all the difference between success and failure.

Why is NFLX valued 3x more than TSLA?

They are making PROFITS and will increase their profits immensely in the coming years, whereas the business case of Tesla is still very unclear. They can maybe break-even in the next years (best case) and the competition is coming...

Having said that I am not only short Tesla but also Netflix...

")

I'm just opining, haven't taken a good look at either of them in a while, but I would check out the fundamentals, what is the price to book of each? The other thing is ntflx is basically an intangible company, they don't really have or make much that is capital intensive, which is generally seen as a good thing in terms of risk/nimbleness/opportunity. Tesla is the other end of the spectrum a lot of employees and major investments in tangible things. And lastly, a minimal profit is generally considered better than a loss, not to mention tsla credit rating has been downgraded. Ntflx isn't that bad of a comparison to tsla, maybe better than comparing it to other car companies, although amzn and maybe a few others are closer to apples to apples. They all have taken the approach of losses are okay as long as you have good cashflow and are eating market share of incumbents. The other big thing, probably the main thing, is that Tesla only has a few products, most of which are in growth phase right now, so lot's of "they might fail, they are unproven" type thinking. For example if for some reason the model 3 turns out to be just un-makable or un-sellable, it would be a dire situation for tsla, and while those are extremely remote possibilities, the market climbs a wall of worry I guess. I suspect things will change dramatically over the next six months or year. To put that in perspective I think it's likely model 3 will outsell bmw 3 series next year as long as their supply chain holds up, and that is assuming they make no additional progress on autopilot. Just blue skying but I think there's a chance autopilot will advance so much that they basically have to give it away to all other automakers (for safety), at least that's what I hope they do, give away the safety part, license the convenience part. My question is will tsla just do a few profitable quarters or a year and go back to profitless growth phase or are they really trying to go with profits permanently?I'm trying to better understand Tesla's valuation compared to Netflix and what Tesla's share price could potentially be if it overcomes current hurdles.

Netflix is aiming for $15 Billion in revenue this year.

Very conservatively, Tesla will have similar revenue (probably more).

Netflix is making minimal profit, PE 223, so less than 1 B / year. Tesla is losing money but is spending huge amounts on capital investment for the future.

Tesla revenue will likely grow faster than Netflix.

Why is NFLX valued 3x more than TSLA?

Tesla needs to prove it can produce the 3 at scale, with good margins, and be able to use this money to fund growth rather than through capital raises. There is some uncertainty if whether Tesla can do this and I think that is understandable. But, if Tesla can do this, I don't see why it could 't be valued similar to NFLX in terms of 150B valuation, share price $800-900.

The reason the stock is trading at 290 is that most people don't believe Tesla can deliver on its promises. What are your thoughts?

Last edited:

tftf

Member

NFLX vs TSLA?

Let’s compare two bubbly stocks (granted, from two very different sectors) in a late-stage bull market (as of early 2018)?!

Comparative valuations of bubble stocks make little to no sense imho - except for chasing momentum and selling to a bigger fool before the bubble pops.

A dotcom example:

'What Were You Thinking?' | The Felder Report

And, from the same source:

(That was as of autumn of 2017, the time the column was written, things got worse in terms of valuation in the meantime).

Let’s compare two bubbly stocks (granted, from two very different sectors) in a late-stage bull market (as of early 2018)?!

Comparative valuations of bubble stocks make little to no sense imho - except for chasing momentum and selling to a bigger fool before the bubble pops.

A dotcom example:

Scott McNeely was the CEO of Sun Microsystems, one of the darlings of that (dotcom) bubble. At its peak his stock hit valuation of ten-times revenues. A couple of years afterward he had this to say about that time (via Bloomberg):

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

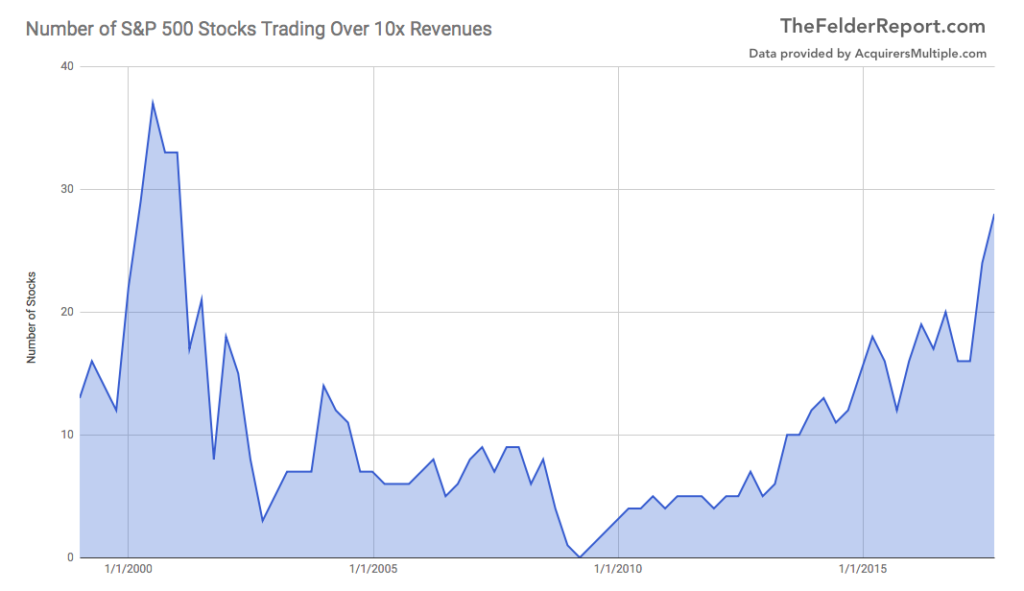

Below is a chart of Sun Micro from 1996 to 2006. It started around $5 ran up to that $64 Scott mentions and then fell right back to $5. And you would think this might serve as a cautionary tale for investors today.

'What Were You Thinking?' | The Felder Report

And, from the same source:

Interestingly, there were 29 stocks within the S&P 500 that traded above ten times revenues at the peak of the dotcom mania (though that number did surge higher after prices had already peaked). Today, there are 28.

(That was as of autumn of 2017, the time the column was written, things got worse in terms of valuation in the meantime).

Last edited:

Netflix is a very good business, but Tesla's growth profile is much, much faster. Netflix is growing at about 30% a year. Tesla is growing at 50%-100%. Once Tesla turns the corner into profitability and is cash flow positive, we will be in a different place.

That's all really cute. But I'd like to point out that Tesla is not one of those companies. Their 2017 revenue was $11.76B, and their market cap today is $49.02B, for a multiple of 4.16.NFLX vs TSLA?

Let’s compare two bubbly stocks (granted, from two very different sectors) in a late-stage bull market (as of early 2018)?!

Comparative valuations of bubble stocks make little to no sense imho - except for chasing momentum and selling to a bigger fool before the bubble pops.

A dotcom example:

'What Were You Thinking?' | The Felder Report

And, from the same source:

(That was as of autumn of 2017, the time the column was written, things got worse in terms of valuation in the meantime).

Esme Es Mejor

Member

Netflix is a very good comparison with where we hope Tesla will be within 6-12 months. With Model 3 ramped, Tesla should be able to continue growing at a 50% rate while showing profits. The profits will likely be modest and the P/E high— and the bears will, no doubt, jump on that— but it will reassure most investors.

I’ll have to look more in Netflix’s debt & capital obligations— if they have less debt & more flexible capital obligations, that would be another reason investors would give Netflix a higher valuation.

But yeah, consistent profits of over $100 million per quarter (~$500 million/year) could very well push Tesla’s market cap over $100B. Show profitable and growing businesses in energy & commercial (Semi and/or Tesla Network), and Tesla looks more like Amazon than Netflix. But that’s many years— and a whole lotta execution risk— away.

I’ll have to look more in Netflix’s debt & capital obligations— if they have less debt & more flexible capital obligations, that would be another reason investors would give Netflix a higher valuation.

But yeah, consistent profits of over $100 million per quarter (~$500 million/year) could very well push Tesla’s market cap over $100B. Show profitable and growing businesses in energy & commercial (Semi and/or Tesla Network), and Tesla looks more like Amazon than Netflix. But that’s many years— and a whole lotta execution risk— away.

sdtslafan

Member

NFLX vs TSLA?

Let’s compare two bubbly stocks (granted, from two very different sectors) in a late-stage bull market (as of early 2018)?!

Comparative valuations of bubble stocks make little to no sense imho - except for chasing momentum and selling to a bigger fool before the bubble pops.

A dotcom example:

'What Were You Thinking?' | The Felder Report

And, from the same source:

(That was as of autumn of 2017, the time the column was written, things got worse in terms of valuation in the meantime).

For Tesla to reach 10x revenue it would have to be a 150 billion dollar company. Share price $900. It's nowhere even close to that...but I do like your optimism! Nice to know Tesla has long way to go before it reaches dot com valuation.

brian45011

Active Member

For the recourse debt as long as Tesla is showing profits before March 2019, they'll be able to refinance all the recourse debt -- but in fact a bunch of it will probably convert to equity..

None of the $230 million in SCTY convertible notes, that must be repaid to holders in November 2018, will be converted to equity--the conversion share price is $561/share.

The $920 million in TSLA 2019 convertible notes can be redeemed by holders beginning December 1, 2018. Most holders will redeem them as soon as they can since the those notes only pay 1/4 of one percent, and market interest rates are rising. The prospectus stated:

" conversions of 2019 notes occurring on or after December 1, 2018 (the applicable Free Conversion Date for the 2019 notes) will be settled using the same relative proportion of cash and/or shares of our common stock as all other conversions occurring on or after December 1, 2018. We will inform holders of the settlement method we elect for any conversions occurring on or after December 1, 2018 no later than December 1, 2018. If we do not timely elect a settlement method, we will no longer have the right to elect cash settlement or physical settlement and we will be deemed to have elected combination settlement in respect of our conversion obligation, as described below, and the specified dollar amount (as defined below) per $1,000 principal amount of notes will be equal to $1,000. If we elect combination settlement but we do not timely notify converting holders of the specified dollar amount per $1,000 principal amount of 2019 notes, such specified dollar amount will be deemed to be $1,000."

Any refinance of these two issues of recourse debt in 2018 would be a capital raise, and Elon has reiterated there will be no capital raises in 2018. Apparently un-drawn commitments under the ABL line will be available to fund redemptions of these two issues during 2018.

JRP3

Hyperactive Member

Technically I believe he's said there is no need to, but that's not the same as saying they won't if there is a good reason to.and Elon has reiterated there will be no capital raises in 2018.

Technically I believe he's said there is no need to, but that's not the same as saying they won't if there is a good reason to.

If I can interpret EM speak and intent: I believe his statement was to allay fears that a cap raise would be needed to get the '3' to scale to a point where it could sustain itself financially. We all know that if Tesla is to continue to grow rapidly, especially putting out the Y, semi a pick up and additional battery production needed for them that multiple factories and Cap raises will be needed.

If he can get free cash flow in Q3/4 and then goes to the markets for cap infusion for the above mentioned growth EM will have no problem getting the cap needed and I would suggest (not that he listens to me) he raise a ton of cap to grow asap.

I doubt anyone would fault him to go for a cap raise in 2018 under those circumstances

You are a good laugh.They are making PROFITS and will increase their profits immensely in the coming years, whereas the business case of Tesla is still very unclear. They can maybe break-even in the next years (best case) and the competition is coming...

Having said that I am not only short Tesla but also Netflix...

Similar threads

- Replies

- 0

- Views

- 90

- Locked

- Replies

- 0

- Views

- 4K

- Replies

- 1

- Views

- 500

- Replies

- 23

- Views

- 851

- Replies

- 21

- Views

- 6K