OK let's compare all 3;

My advice, the translation of his advice, and his advice.

Here we go

My advice:

Maintain FULL CORE TSLA (for 5+ years),

In common only, under current and impending macro risk;

Not leveraged in Options or margin (only discretionary, roulette for those)

So that you can comfortably ride through a much elevated accute macro risk (historically new territory)-

To assure capture of potentially massive increase in TSLA, while riding thru the afore mentioned historically elevated macro risk-

not yet calling for Recessive or secular Bull to Bear transition- but extreme risk of event driven corrections, that may well lead to this -

timeframe 0-6 months hard watch - keep core fully in but unleveraged...

Translation of Shiller's advice producing a disconnect:

"Schiller is advising to stay in the market for another 50% run!

Bullish sentiment- from a so called perma-bear"

Schiller' advice untranslated:

"I would say have

some stocks in your portfolio. It

could go up 50 percent from here. That's what it did around 2000, after it reached this level, it went up another 50 percent."

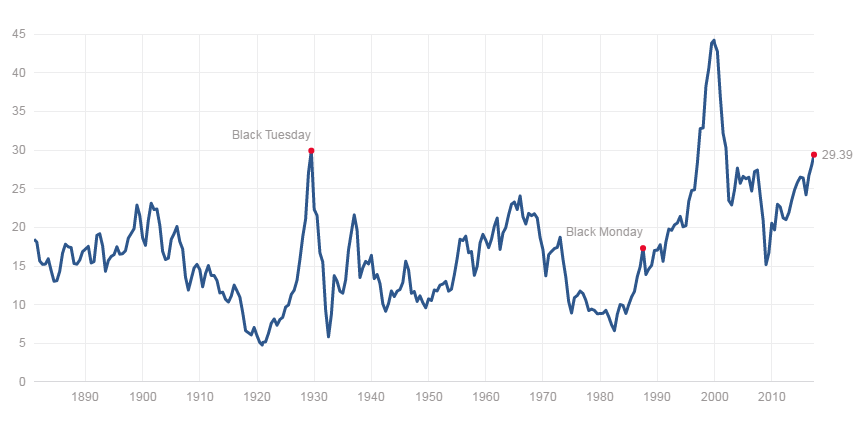

Shiller CAPE PE Ratio

{Not specified by Schiller words, but communicated from his graph of his market valuation method -

THE ONLY TIME IN ALL OF HISTORY, including the Great Depression, it went up from here AT ALL much less 50%, was 2000. And that, Without any corresponding socio-political risks we currrenlty have, historically never experienced, and Without any of he Fed balance sheet and interest rate challenges, also historically never experienced.}

More from Schiller:

"So I'm

not against investing in the stock market when you consider the alternatives.

But I think if one wants to diversify, US is high in its CAPE ratio. You can go practically anywhere else in the world and it's lower," Shiller said. "We

could even set a new another record high in CAPE,

that's not a forecast."

However, even though the current CAPE ratio is at 29, which is above the 17 historical average, the economist is

not calling for a market decline.

"I can see it as a real possibility that stocks prices and house prices would both keep going up for years,

but I'm not forecasting that by any means," he added.

--

{The following Exhibit 2 posting I made in the macro thread, shows exactly Schiller's cautionary tale, investments are seeking better Equity risk values

outside the US,

and additionally shows (not pointed out by Schiller),

Bond funds are also beneficial receivers of these flows- further driving down long term Bond Yields, which includes the market assessment of Equity futures relative to these 'anemic other alternatives' Schiller references -

this strongly signals a very new macro dynamic and a possible strong correlation to the new US current relationship fomented by our new international interactions- never before undertaken by our government - of course, it could be something else less ominous, regardless the result is the same and duly recorded in the data}

View attachment 230757

Additional closing comments from me:

The 'saving grace' prevalent in counter arguments utilizes current low interest rates, compared to the only other time in history the market went higher from here (2000).

In 2000 Fed rates were about 6% (precipitacely dropping over the following year to 2%) with 2000 GDP running about 4%.

Today we have a Fed rate of 1% (next week very likely moving higher) and GDP about 2%.

Each will make their own assessment of how that net difference produces an effective, first-time-in-history, deterrent to market correction risk, given current dynamics (Other economic data, Fed balance sheet, Socio-Political, World events, etc.).

My assessment is

that once effective argument is quickly diminishing and running its course-

Is scheduled to become an unreliable hedge.

hence my heightened warnings--