Stealing

@petit_bateau's link about growth in PV manufacturing capacity because this is a big one:

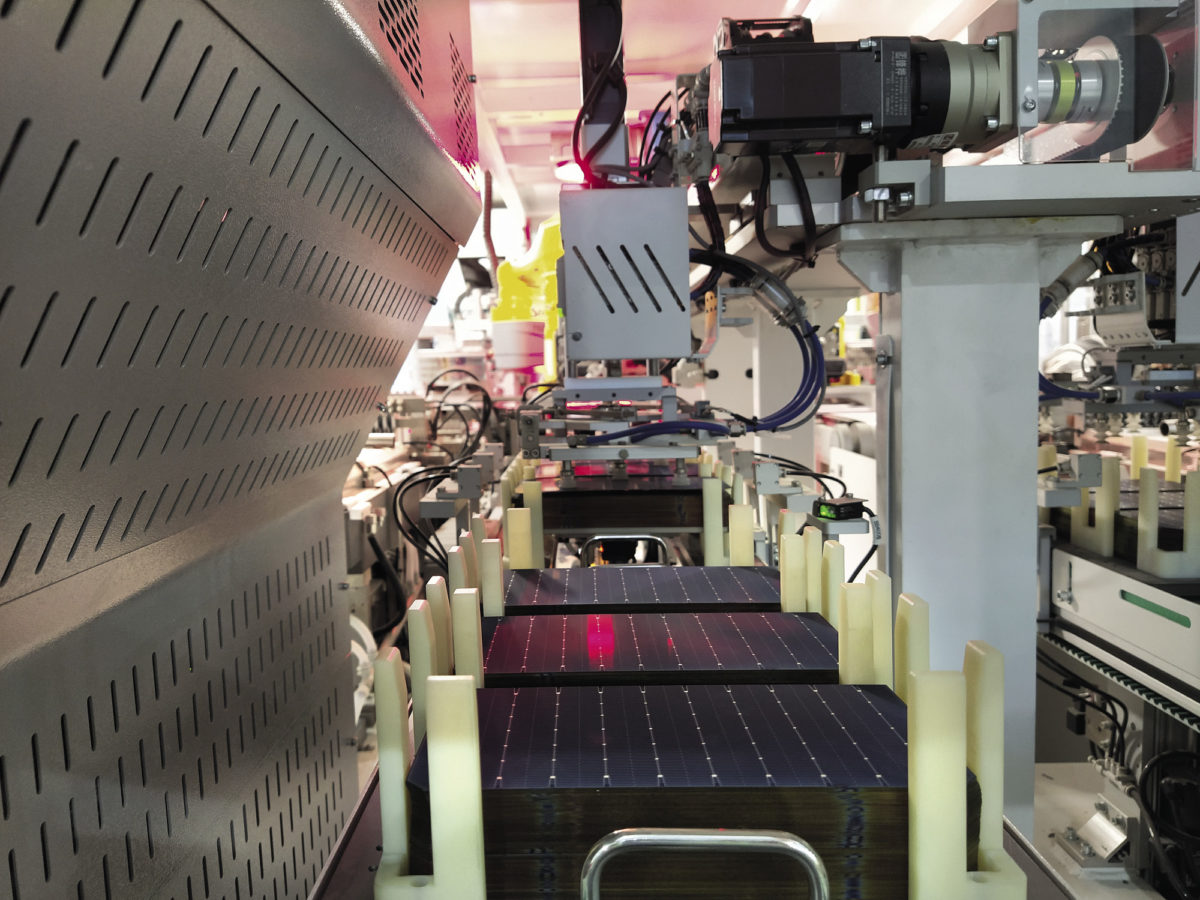

The new edition of the International Technology Roadmap for Photovoltaic (ITRPV), published this week, finds that 295 GW of PV modules was shipped in 2022, and that prices for silicon PV modules fell by 7% over the year. The report finds that price premiums for n-type modules are now marginal...

www.pv-magazine.com

The article says 295GW shipped in 2022, but 600GW capacity in 2023?

How so?

Because ...

Clean Energy Associates expects manufacturing capacity to exceed installations next year.

pv-magazine-usa.com

... the underlying supply chain is going to increase significantly this year.

And if you were wondering if you can really believe (as previously reported by

@petit_bateau) ...

India's plans to stop building new coal-fired power plants beyond those already under construction mark a significant victory for climate campaigners keen to cap pollution from the second-largest coal user after China.

www.reuters.com

... it might be because ...

India’s solar module manufacturing capacity could reach 110 GW by 2026. It will also have a notable presence in all upstream components of PV manufacturing, such as cells (59 GW), ingots/wafers (56 GW), and polysilicon (38 GW).

www.pv-magazine-india.com

... the Indian government,, which has been trying for years to shape policy to grow domestic solar manufacturing, is more confident that it's going to happen.

Also worth noting in the article I linked in this first post, isn't just the rapid total capacity increase, with the expansion in polysilicon supply, and ever-larger new solar panel manufacturing plants, but the new capacity is seeing growth in more efficient technologies. That offers the potential of a two-dimensional expansion both in installed capacity but also in capacity factors.

It's shaping up for rapid change in the next 5 years, somewhat like the LCD display shift.