Thread on 50% growth target, endorsed by Elon.

This shows that contary to recent FUD Tesla are ahead of their 50% growth in vehicle deliveries.

This shows that contary to recent FUD Tesla are ahead of their 50% growth in vehicle deliveries.

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

This shows that contary to recent FUD Tesla are ahead of their 50% growth in vehicle deliveries.

The actual source that explains why his own argument is bad but then dismisses the reason said:Some pundits point to Zach Kirkhorn and Elon Musk’s statements during the ’22 Q3 Earnings Call, claiming that they affirmed guidance of 50% above 2021 deliveries was for this year.

Respectfully disagree. Fourth option is to cancel the order. These are the decisions of real buyers that will impact Tesla's demand. We know supply is on the rise due to Giga Austin ramp, car loan interest rates are relatively very high, and I assure you that the "competition" (albeit inferior) will find a way to make that sweet sweet government subsidy nectar apply to their products. I agree that I assumed incorrectly, but, many others did too - influenced directly from Tesla's last earnings call...but I disagree that it's not a Tesla problem to solve.You assumed incorrectly. Tesla never stated it would qualify. This isn’t a Tesla problem, it’s your problem. You can either find one in the next three days, lease one, or add the third row.

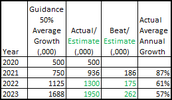

So, this is saying that if you interpret 50% annual growth target based on 2020's 500,000 vehicles, (500,000x1.5^t), they are way ahead of their targets.Thread on 50% growth target, endorsed by Elon.

This shows that contary to recent FUD Tesla are ahead of their 50% growth in vehicle deliveries.

Eh…..what is Larry smoking here???So Elon liked this thread, which maybe a nothing burger, but just agreeing that wallstreet is being brutal to Tesla by moving the goal post despite the over performance.

Larry's thread basically explains that Tesla's guide is 50% yoy compounded growth. However in years they over performed like last year, people are expecting Tesla to grow 50% over their overperformance for the year after.

2020->500k guide but hit 499k

2021->750k guide (but actually hit 936k)

2022->1125k guide (but now people are expecting 50% growth over 936k).

Now to be clear, Zach did express that hitting 50% growth will be difficult due to China shutdown, so obviously he didn't mean hitting 1125k, but 50% over 936k. However I guess Larry has a point that people lost track what Tesla's performance should be because they have been over performing so hard.

So, this is saying that if you interpret 50% annual growth target based on 2020's 500,000 vehicles, (500,000x1.5^t), they are way ahead of their targets.

Does Tesla interpret it that way? Or is it really 50% yoy?

nope - on earnings calls all year they have been targeting 50% growth over last years actual results (not some hypothetical 2021 results based on a several ywars old projection).So, this is saying that if you interpret 50% annual growth target based on 2020's 500,000 vehicles, (500,000x1.5^t), they are way ahead of their targets.

Does Tesla interpret it that way? Or is it really 50% yoy?

Eh…..what is Larry smoking here???

Tesla has had a great year of growth, no need for sycophants to twist a word pretzel together to try and justify how managements guidance for 50% growth in 2022 is somehow based on an extrapolation of figures from 2 years earlier - when in fact it would be clear to a 5 year old listening to this years earnings calls that it was based on growth over last years actuals.

Honestly 40% or more growth is bloody fantastic and there is no need to gaslight the situation into anything else.

Well, wouldn't be the first time...Yep.

70% down this year but we need 300%+ up next year to get back to where we were.

Elon liking a thread that emphasizes his long term multi year goals of 50% growth annually is not the same as Elon refuting management comments (including his own) made during 2022 earnings calls.I can't speak for Tesla, but Elon replied by

indicating that he approves.

Market share is always a relative number/percentage, no? Not sure what you mean.Particularly in the US, I see Tesla possibly gaining rather than losing EV market share for the next 3-4 years. If not in percentage terms, definitely in raw numbers.

A nothing burger. Elon was very clear on the calls that the 50% is the average for the coming years till 2030. Some years it will be less, some years it will be more.Elon liking a thread that emphasizes his long term multi year goals of 50% growth annually is not the same as Elon refuting management comments (including his own) made during 2022 earnings calls.

To try and claim that all those comments were in fact referencing a projection based on figures from years earlier (without clearly stating that during each earnings call) would likely be a clear cut violation of US securities laws.

YesYour own work I assume?

Not an answer to your question, but interesting data collection I just found while surfing the tesla-twittersphere:

Tesla Megapack Tracker

Map of Tesla and other big battery installations. And more info around battery storage...lorenz-g.github.io

Has among other goodies yearly estimates of percentage of storage cell capacity of total Tesla (automotive+storage).

I meant I expect them to increase the percentage market share, but if that doesn't happen the raw sales numbers will still continue to increase.Market share is always a relative number/percentage, no? Not sure what you mean.

I would really like to see another green day before judging this the bottom and accumulating...but it looks like the P&D report will come out Monday when the market is closed right?

Are other people weighing the same dilemma and planning on buying today anyway?

")

One of his regular planned sells... he may be shocked to see how much less he received this time...A Form 4 just dropped but don’t worry it was just Drew

The classifications boggle the mind, just bizarre... why have all these complex rules are bonkers, just give $7500 credit on all EV's below, say $75k and be done with itYou are 100% correct here. But the incentive does put Tesla in a weird place. I doubt insaneoctane is alone.

The IRS really put manufacturers in a weird place dropping this significantly different interpretation at the last minute.