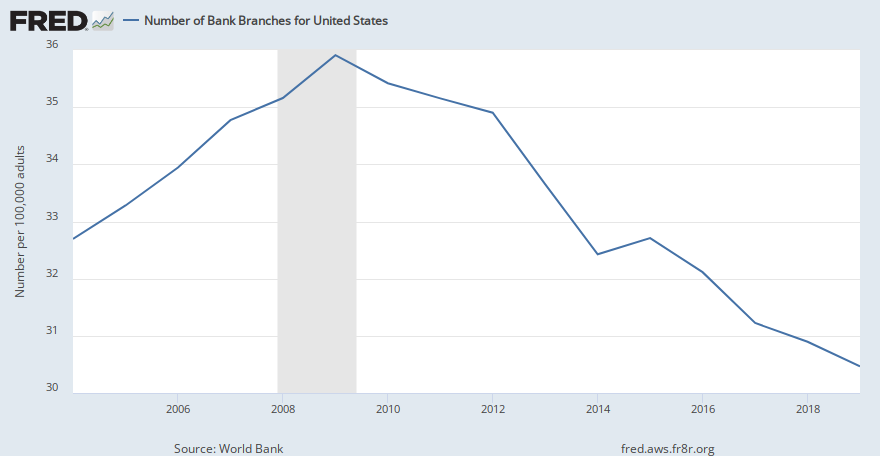

The reduction in bank branches dates from the 1980's with massive growth of "non-bank-banks" (look them up if you care) and with the 2008 crisis that caused the failures of many Savings and Loans in the US, plus deregulation. and the elimination of the Glass-Steagall Act and McFadden Act ((look those up if you care). Those eliminated more bank branches than did technology changes, but ATM's were a factor at the same time. Beginning around 1995, though, online banking became a thing, and many former non-bank-banks (most recognizably CapitalOne) bought small commercial banks but grew with online banking. Today most banking transactions take place online, many related to e-commerce (does anyone here misunderstand the impact of Amazon, Alibaba. Google etc on use of cash, in-person bank use by consumers?) and all of them via remote payment processing.From what I've read that's overwhelmingly more due to massive consolidation of small banks bought out by large ones and closing redundant/unprofitable locations than due to ATMs existing (not that I doubt that, and much moreso online banking, has had SOME impact)

Many people (including me, one of the oldest people around this board I suspect) no longer use bank branches at all. I have never been to a physical location of any of my US banks (four of them). Two of my banks, one in Brazil one the US) do not have branches at all. The truly amazing fact is that so many bank branches still exist at all.

This process is quite directly related to Tesla and TSLA. Remote on-line processing is cheaper, more accurate, compatible with long service hours, and is easily software upgradable. Bank branches are analogous with car dealers Both provided necessary services in the pre-internet world. Both are very, very expensive and are labor intensive. Is it any wonder that both are durable, but declining?

Now consider that TSLA is gradually moving towards financial services with car leasing, car insurance, energy sales and more evolving. All of those are ones which pre-Glass-Steagall repeal. pre-internet were more expensive and and less efficiently processed than they are now, with consumer behavior much harder to track and use for risk management. TSLA and FWIW, Twitter, are rapidly heading towards the visions Elon Musk had when X.com morphed into PayPal. Those two were only possible because fo the banking deregulation mentioned above. TSLA is preparing for the expansion of such services globally, several of them likely to reach maturity when RoboTaxi eventually happens, but also be productive long before that eventuality.

I understand that this post goes directly from bank branches to TSLA. That really is because Elon went on the same path beginning even before X-com, when Zip2 became the genesis of hyperlocal remote marketing.

Last edited: