For ASP I went here:

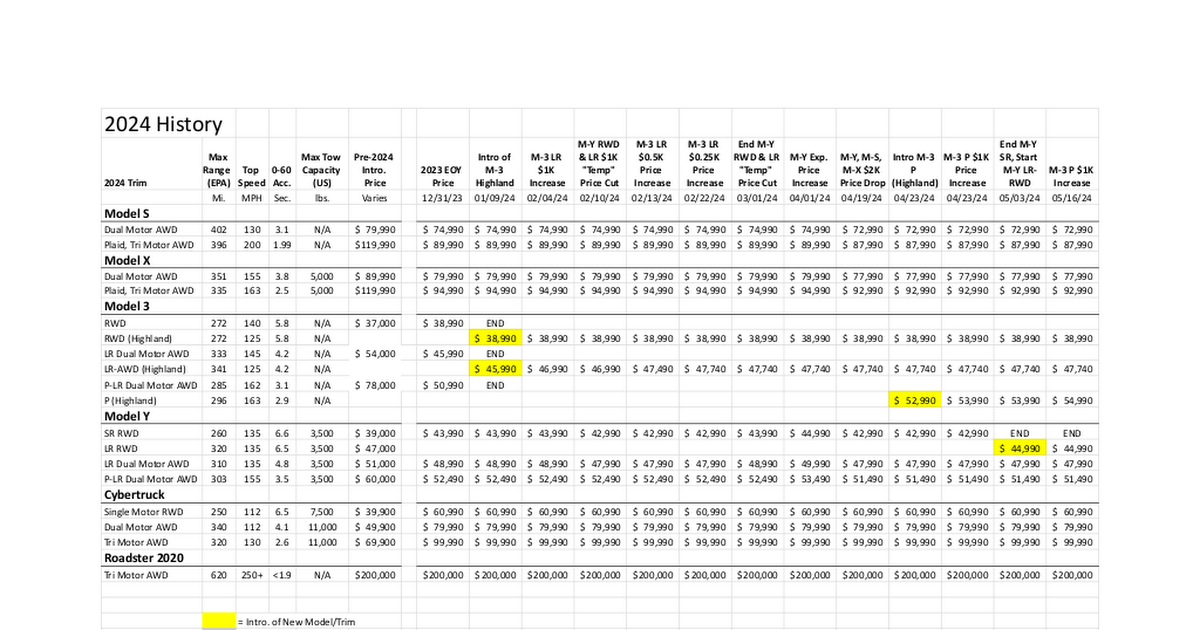

Tesla Car Price History

For COGS I followed the advice a few posts back about backing out the leasing (roughly 10% of S+X and roughly 3% of 3 + Y are leased) and then fitting the numbers against auto revenues. Same thing for costs.

For me, it made Q2 pretty ugly based on the 3 + Y. Assuming deliveries in the 440K range (quite a bit higher than Troy is reporting - we'll see what his next update says) and assuming 42.7K ASP for 3 + Y, against 37K for 3+Y COGS, I ended up with GAAP EPS in the $0.48 range for Q2. This is very low compared to the street consensus.

I ended up selling and I'll be buying back in when ASP trends back up.

EDIT: Zach said COGS for Q2 will decline, but the question is - how much. The new motor assembly is apparently going in which is somewhat cheaper to assemble, and Lithium prices are coming down. I assumed a drop of $600 vs. Q1 for 3+Y