Welcome to Tesla Motors Club

Discuss Tesla's Model S, Model 3, Model X, Model Y, Cybertruck, Roadster and More.

Register

Install the app

How to install the app on iOS

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

-

Want to remove ads? Register an account and login to see fewer ads, and become a Supporting Member to remove almost all ads.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Well, yeah, I've done a lot more than dipping my toes into Tesla. But if VW/Volvo/Daimler/BMW all suddenly get religion and somehow kill Tesla (no, I don't think this will happen) oil will still be toast.Actually, I think one of the best ways to profit from the demise of the oil industry is to invest in Tesla. Is it better to invest in the disruptor or short the disrupted?

adiggs

Well-Known Member

Well, yeah, I've done a lot more than dipping my toes into Tesla. But if VW/Volvo/Daimler/BMW all suddenly get religion and somehow kill Tesla (no, I don't think this will happen) oil will still be toast.

Heh - sounds like you're thinking that the death of oil is the safer investment

")

adiggs

Well-Known Member

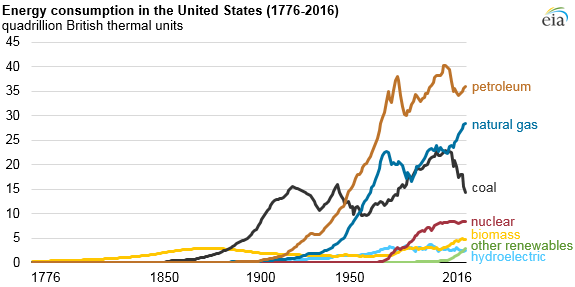

That sure is a whole heck of a lot of market share for "other renewables" to take. Especially because at least some of the biomass line is ALSO available for the taking, much less all the BTUs in fossil fuels.

To an earlier point made by @jhm (oil & gas throwing coal under the bus), that's about 15 units of demand that can be used to sustain the ~35+~30 units of demand currently consumed by the top two lines. I'm thinking that coal's demand doesn't hang around for too long, and the nat gas / coal curves certainly look that way too.

Good stuff.

adiggs

Well-Known Member

OMG, DRIP is up 10%. Thanks for the tip.

One of the basic things we have learned in this thread is that the market cap of oil companies will likely collapse long before EVs will trigger decline in oil consumption. Simply having the price of oil too low for too long will destroy market value of oil companies. So I am becoming more persuaded that shorting the oil companies may make more sense than shorting oil. Although at the outset of this thread I was more concerned about the impact of low oil prices on Tesla's share price, hence SCO as a hedge. But to make money on the demise of the oil industry, something like DRIP may be the better play.

If we pretend that past is prologue, and use the coal industry as our example of what happens to a fossil fuel provider that sees ~20% demand decline, then yeah - shorting the companies looks better than shorting the commodity. I actually don't know the prices of coal between 10 years ago and today, but I figure they're down nowhere close to 99.9%

Black swan!Well, yeah, I've done a lot more than dipping my toes into Tesla. But if VW/Volvo/Daimler/BMW all suddenly get religion and somehow kill Tesla (no, I don't think this will happen) oil will still be toast.

A few days ago I meant to make a prediction that WTI crude would begin to fall again once it reached $47/b. There is a pretty strong downward channel for oil.

Well hindsight is 20/20.

.png")

That was quite a tumble today. The last little blip is the start of tomorrow's trading day. API thinks there will be a draw of crude, but this is usually a poor predictor of the EIA weekly. So if the EIA reports weaker numbers than API, I would expect oil to continue to tumble.

Even so, I suspect that the price of oil really does need to go low enough to shut down production growth. They say, the solution for low prices is low prices.

Well hindsight is 20/20.

That was quite a tumble today. The last little blip is the start of tomorrow's trading day. API thinks there will be a draw of crude, but this is usually a poor predictor of the EIA weekly. So if the EIA reports weaker numbers than API, I would expect oil to continue to tumble.

Even so, I suspect that the price of oil really does need to go low enough to shut down production growth. They say, the solution for low prices is low prices.

"The wallpaper and I are fighting a duel to the death. One or the other of us has to go". -- Oscar Wilde, on his death bed.Heh - sounds like you're thinking that the death of oil is the safer investment

I very much want Tesla to succeed. But oil has to go, or we all do.

durkie

Member

Despite how closely I'm following and occasionally contributing to this thread, the limit of my investment behavior / activity is going to be moving indexed funds into an index that doesn't include energy (what I really want is something that excludes companies with fossil reserves - this is the closest I've found: https://us.spdrs.com/en/etf/spdr-sp...pdr-sp-500-fossil-fuel-reserves-free-etf-SPYX). I'll be moving from 0.03% fees to 0.25% fees, but I think that's a good trade to remove companies with fossil fuel reserves for that piece of my portfolio.

I like the idea of shorting exploration companies, the exploration equipment suppliers, and fossil reserves owners. But not enough to violate my personal "no shorting" rule (a rule derived from the idea that the market can be irrational far longer than I can remain solvent).

One strange thing about SPYX is that if you download their holdings it does still have several companies in the energy sector for some reason (like Valero, Halliburton and Phillips 66). It could be that they're in the process of winding these down, but it seems kind of against the whole point of the ETF, especially given the higher fees.

SPXE seems to be completely energy free and has lower fees, but is extremely thinly traded.

The Shale Gas Revolution Is A Media Myth | OilPrice.com

Berman is back. Berman claims that the breakeven for US natural gas is about $4/mmBtu. The basic evidence is that gas producers remain unprofitable with gas prices just under $4, and that rig counts decline as gas price fall below $4. There is presently a 4bcf/d deficit. So Berman sees gas scarcity approaching as prices remain stubbornly too low.

Elsewhere we have learned that the coal crossover price is also with gas at about $4/mmBtu. So if gas prices rise to profitable levels, we could see a rise of coal in power generation.

So ultimately we need renewables to step in with prices below $40/MWh. Remember at $4/mmBtu, the cost of fuel in an average CCNG plant is about $32/MWh. So wind and solar below $40/MWh can both coal and gas as a fuel above $4/mmBtu. Renewables below that level will continue to push both gas and coal out of power generation. And batteries at $250/kWh will also drive gas out of peak power markets.

So those are the price parameters, and renewables can meet them. But the hold up is if gas were to return to a glut. But if the deficit persists, then we could see a wave of renewable investment. I do wonder if this talk of O&G companies entering the renewable space may be that they know gas cannot remain long in the power markets. There may well be better markets for gas in heating and petrochemicals, but power generation seems to be a market of last resort (that and LNG). So this could be really big news for solar and wind.

Still piecing this together...

Berman is back. Berman claims that the breakeven for US natural gas is about $4/mmBtu. The basic evidence is that gas producers remain unprofitable with gas prices just under $4, and that rig counts decline as gas price fall below $4. There is presently a 4bcf/d deficit. So Berman sees gas scarcity approaching as prices remain stubbornly too low.

Elsewhere we have learned that the coal crossover price is also with gas at about $4/mmBtu. So if gas prices rise to profitable levels, we could see a rise of coal in power generation.

So ultimately we need renewables to step in with prices below $40/MWh. Remember at $4/mmBtu, the cost of fuel in an average CCNG plant is about $32/MWh. So wind and solar below $40/MWh can both coal and gas as a fuel above $4/mmBtu. Renewables below that level will continue to push both gas and coal out of power generation. And batteries at $250/kWh will also drive gas out of peak power markets.

So those are the price parameters, and renewables can meet them. But the hold up is if gas were to return to a glut. But if the deficit persists, then we could see a wave of renewable investment. I do wonder if this talk of O&G companies entering the renewable space may be that they know gas cannot remain long in the power markets. There may well be better markets for gas in heating and petrochemicals, but power generation seems to be a market of last resort (that and LNG). So this could be really big news for solar and wind.

Still piecing this together...

These firms do not have reserves. They are refiners and service providers. The ETF description says its reserves free, not ex-fossil fuels firms. I like this position from an investment perspective because refiners have been minting a pretty penny.One strange thing about SPYX is that if you download their holdings it does still have several companies in the energy sector for some reason (like Valero, Halliburton and Phillips 66). It could be that they're in the process of winding these down, but it seems kind of against the whole point of the ETF, especially given the higher fees.

SPXE seems to be completely energy free and has lower fees, but is extremely thinly traded.

The Shale Gas Revolution Is A Media Myth | OilPrice.com

Berman is back. Berman claims that the breakeven for US natural gas is about $4/mmBtu. The basic evidence is that gas producers remain unprofitable with gas prices just under $4, and that rig counts decline as gas price fall below $4. There is presently a 4bcf/d deficit. So Berman sees gas scarcity approaching as prices remain stubbornly too low.

Elsewhere we have learned that the coal crossover price is also with gas at about $4/mmBtu. So if gas prices rise to profitable levels, we could see a rise of coal in power generation.

So ultimately we need renewables to step in with prices below $40/MWh. Remember at $4/mmBtu, the cost of fuel in an average CCNG plant is about $32/MWh. So wind and solar below $40/MWh can both coal and gas as a fuel above $4/mmBtu. Renewables below that level will continue to push both gas and coal out of power generation. And batteries at $250/kWh will also drive gas out of peak power markets.

So those are the price parameters, and renewables can meet them. But the hold up is if gas were to return to a glut. But if the deficit persists, then we could see a wave of renewable investment. I do wonder if this talk of O&G companies entering the renewable space may be that they know gas cannot remain long in the power markets. There may well be better markets for gas in heating and petrochemicals, but power generation seems to be a market of last resort (that and LNG). So this could be really big news for solar and wind.

Still piecing this together...

JHM, first of all great job hosting this thread and this has lead me to explore a lot more in the area of renewables replacing gas plants. If you are not already familiar with it, there is a podcast on energy transition by Chris nelder, that is extremely interesting. It is a paid podcast, but is worth every penny at 60 bucks for an annual subscription.

The reason I bring it up is, there are several other grid management considerations when renewables go above a certain level. Of course batteries can help, but my sense is they may not be able to scale for the next 3-5 years, Gigafactory notwithstanding.

http://ir.eia.gov/wpsr/overview.pdf

EIA Weekly is out.

Crude stock: -6.3 mmb

Total stock: -13.4 mmb

This kind of decline in total stock is quite suspicious. How did they move an extra 1.9 mb/d out of the system?

Crude net import: -274 kb/d

Total net import: +684 kb/d

So it was not a decline in total net imports that reduced total inventory, but reduced crude imports do explain a 1.9 mmb reduction in crude stock.

How about products supplied to the domestic market?

Total chg w/w: +2579 kb/d, +13%

Other prod chg w/w: + 1458 kb/d, +47%

BINGO!!! The industry is channel stuffing again. Other products excludes gasoline, distillates, jet, residual fuel and propane. How in the world does demand for this grow from 3075 kb/d to 4533 kb/d in the span of just one week, a 47% increase?

We saw this sort of thing several weeks ago. "Product Supplied" is supposed to be a measure of domestic consumption, but now it appears to be for form of storage.

So, sure, commercial inventories shrank 13.4 mmb, but an extra 18.1 mmb just rolled into retail storage.

Look out below!!!

EIA Weekly is out.

Crude stock: -6.3 mmb

Total stock: -13.4 mmb

This kind of decline in total stock is quite suspicious. How did they move an extra 1.9 mb/d out of the system?

Crude net import: -274 kb/d

Total net import: +684 kb/d

So it was not a decline in total net imports that reduced total inventory, but reduced crude imports do explain a 1.9 mmb reduction in crude stock.

How about products supplied to the domestic market?

Total chg w/w: +2579 kb/d, +13%

Other prod chg w/w: + 1458 kb/d, +47%

BINGO!!! The industry is channel stuffing again. Other products excludes gasoline, distillates, jet, residual fuel and propane. How in the world does demand for this grow from 3075 kb/d to 4533 kb/d in the span of just one week, a 47% increase?

We saw this sort of thing several weeks ago. "Product Supplied" is supposed to be a measure of domestic consumption, but now it appears to be for form of storage.

So, sure, commercial inventories shrank 13.4 mmb, but an extra 18.1 mmb just rolled into retail storage.

Look out below!!!

ValueAnalyst

Closed

http://ir.eia.gov/wpsr/overview.pdf

EIA Weekly is out.

Crude stock: -6.3 mmb

Total stock: -13.4 mmb

This kind of decline in total stock is quite suspicious. How did they move an extra 1.9 mb/d out of the system?

Crude net import: -274 kb/d

Total net import: +684 kb/d

So it was not a decline in total net imports that reduced total inventory, but reduced crude imports do explain a 1.9 mmb reduction in crude stock.

How about products supplied to the domestic market?

Total chg w/w: +2579 kb/d, +13%

Other prod chg w/w: + 1458 kb/d, +47%

BINGO!!! The industry is channel stuffing again. Other products excludes gasoline, distillates, jet, residual fuel and propane. How in the world does demand for this grow from 3075 kb/d to 4533 kb/d in the span of just one week, a 47% increase?

We saw this sort of thing several weeks ago. "Product Supplied" is supposed to be a measure of domestic consumption, but now it appears to be for form of storage.

So, sure, commercial inventories shrank 13.4 mmb, but an extra 18.1 mmb just rolled into retail storage.

Look out below!!!

Can you elaborate further on the part I bolded above?

Read the EIA report I linked to. "Products Supplied" is the next to last box on the first page. This section accounts for products that are being supplied to retail distribution channels. It is considered a measure of domestic consumption, and ultimately it will be consumed. But even retailers have some storage capacity which can be exploited for getting inventory out of the commercial lots.Can you elaborate further on the part I bolded above?

So if inventory is piling up in retail channels, it could indicate logistical problems or it could be an effort of manipulate the market. I do not know which is happening. But even logistic problems are not a good basis for bullishness about commercial stocks. When retailers sit on too much inventory, they will eventually have to pull back on future deliveries. So in the next week or two we could see this reverse. Products Supplied will decline, and stocks may well build again. Once the market figures this out the price of oil will drop.

This is why I worry about market manipulation as a source. Traders in on the scam can make money on the price upswing right now, and then short to make money as it falls apart. Even so, it is possible that logistical problem are the root here.

ValueAnalyst

Closed

Read the EIA report I linked to. "Products Supplied" is the next to last box on the first page. This section accounts for products that are being supplied to retail distribution channels. It is considered a measure of domestic consumption, and ultimately it will be consumed. But even retailers have some storage capacity which can be exploited for getting inventory out of the commercial lots.

So if inventory is piling up in retail channels, it could indicate logistical problems or it could be an effort of manipulate the market. I do not know which is happening. But even logistic problems are not a good basis for bullishness about commercial stocks. When retailers sit on too much inventory, they will eventually have to pull back on future deliveries. So in the next week or two we could see this reverse. Products Supplied will decline, and stocks may well build again. Once the market figures this out the price of oil will drop.

This is why I worry about market manipulation as a source. Traders in on the scam can make money on the price upswing right now, and then short to make money as it falls apart. Even so, it is possible that logistical problem are the root here.

Got it. I look forward to your commentary following next week's report.

Yep, I comment on it almost every week. I've found that I cannot trust the articles in the news that cover it. When I read the report for myself, I see things that are not picked up by the media. Of course, my reading may be flawed as well, but I put it out here where others can pick it apart. So I'd very much would appreciate your participation as well.Got it. I look forward to your commentary following next week's report.

adiggs

Well-Known Member

Interesting trading today.

EIA report posted at 9:30 central.

Initial decline in price 10:35.

News is piblished.

Price spikes up at 10.

I tweet channel stuffing at 11:30.

Price falls 11:55

Big fall 12:25.

Coincidence???

View attachment 234389

@jhm, mover of markets

The good thing about this possible coincidence, is that the channel stuffing insight is valuable to people that are trading this market. If that repeats a few times, they'll learn to look for signs of channel stuffing (or channel draining! lean channel!) to see how the retail channel is influencing the relatively easy to measure commercial channel. With a few repetitions, it'll be market participants and analysts that will also be looking for mechanisms to manipulate the headline numbers and try to get oil prices up.

Ultimately it seems like a foolish activity to engage in. I don't know much about the retail channel for oil products, but the little I've read suggests it's a lot more about managing a big pipeline of stuff in motion - not storing much of anything. In the aggregate, I figure there can't be very much for storage if for no other reason, the companies in the distribution business work on razor thin margins. They can't own much of the stuff at any point in time, much less own or lease the space to store the stuff.

So maybe you couldl stuff the channel for a few weeks? I figure no way you can keep it up for a month or 2. And that means you get a story that is friendly for oil demand for at most a month and at that point, you turn the story upside down and make it really bad for a month while the channel returns to equilibrium.

Good for market manipulators that are trading short swings in the market, but it seems bad for big scale producers of the raw material, big scale processors of the raw material, and big scale consumers (or more likely, mostly a source of indifference for the end consumers).

Then again, if you're desperate, it's easy to lose sight of the bigger picture and only see a short term path to bett

The weekly report was for the week ending June 30. That is a quarter end. So it is possible that refiners were looking to hit quarterly numbers and so offered low prices to retailers along with the expectation that prices would be increasing. Retailers can get into playing this game as well by holding off on orders until producers make price concessions. Perhaps well see more of this sort of behavior going forward.

So channel stuffing need not be a direct market manipulation, but just reflect a sort of negotiation process between suppliers and retailers.

So channel stuffing need not be a direct market manipulation, but just reflect a sort of negotiation process between suppliers and retailers.

Similar threads

- Replies

- 101

- Views

- 3K

- Replies

- 1

- Views

- 659

- Replies

- 0

- Views

- 964

- Replies

- 22

- Views

- 5K