Joe F

Disruption is hard.

No one said there was going to be math.

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

People get very aggravated about debate on this. It doesn't have to be black and white.I am not a fan of shared buyback for Tesla. The factory, technological, market and other risks are very large, as is the negative consequences of being profligate with capital. A large part of the Tesla success story is a positive cash generation cycle, virtually unprecedented for any industrial company.

Being nearly debt-free except for securitizations is a huge virtue. It would be unwise and imprudent to risk that in the face of huge risks, specifically including environment risks in Fremont and Lathrop from earthquakes and drought, Flooding for Shanghai and so on. These have not yet been major issues for Tesla.

Not yet...

All this encouragement to do share buybacks, lengthening loan tenors and doing broadcast advertising terrifies me. Those are tactics to encourage risk of disaster, not minimize that probability.

No one said there was going to be math.

Tesla is charging an extra 50bps for the 7th year of tenor - hopefully that is enough to offset additional losses. I'd expect Tesla to bump that rate up a little more if they get too much portfolio concentration in the long tenors. There is still quite a bit of room to push up the rate on the 7y and have the rental come in lower than the 6y loan. We did similar when I was working auto finance as our funding lines had concentration limits on longer tenors.Sure, and ties buyers into perpetual underwater equity. Stupid and dangerous move. Somebody should ahem show Tesla executives the default rates by tenor. The longer the tenor the higher the default rate. The slope and size of that path varies by percentage equity going in, but is always there.

My data is from OEM proprietary sources so I cannot post details. Anybody with access to securitized auto loan portfolio details can find confirmation, although the longest tenors are rarely included in pools. The major rise in loss frequency and severity is in tenors above 60 months, with origination loan value to purchase price and origination interest rate being closely related variables.

I wish I could share the data. It is compelling.

People get very aggravated about debate on this. It doesn't have to be black and white.

If Tesla had $200Billion in cash, would you be opposed to a dividend or share buyback? I think most people would not. So it really comes down to a decision regarding at what point a buyback/dividend makes sense.

You can't snap your fingers and build 10 factories in a year, or 100,000 superchargers. Tesla's cash balance is a victim of its own success. They are generating money literally faster than they can spend it. There is zero evidence they are cash constrained in any area of expansion.

So what would you do? at what point does the cash pile become ludicrous and the buyback route seem obvious? 30 Billion? 60? 100?

Most of us here agree the stock price fall since Q2 earnings is silly. If I was elon, I'd very happily take advantage of that.

Yah, adding in disposal costs majes it more real. I'm working from a mobile and Google Sheets is not the greatest. Main point was to show yeild was higher that suggested. My calc, while better, is still lower than I would expect.DREW BAGLINO "Yes. First, I’ll just start with a little bit of a production update. So, in Texas, 4680 cell production increased 80% Q2 over Q1, and the team surpassed 10 million production cells produced here in Texas. So, congrats to the team for that. Their focus on yield reduced our scrap bill by 40% quarter-over-quarter, and that resulted in a 25% reduction in cell COGS.

I've been fiddling with this.

Your calculation @Optimeer seems to me to be fine, but I cannot square the result you present - a yield of approximately 30-38% - with other previous information, and I think I can see how to solve this issue.

If you go back to Jan-2022 there were some leaded Kato Rd yield documents that indicated a 92% yield from a line consisting of 14 machines

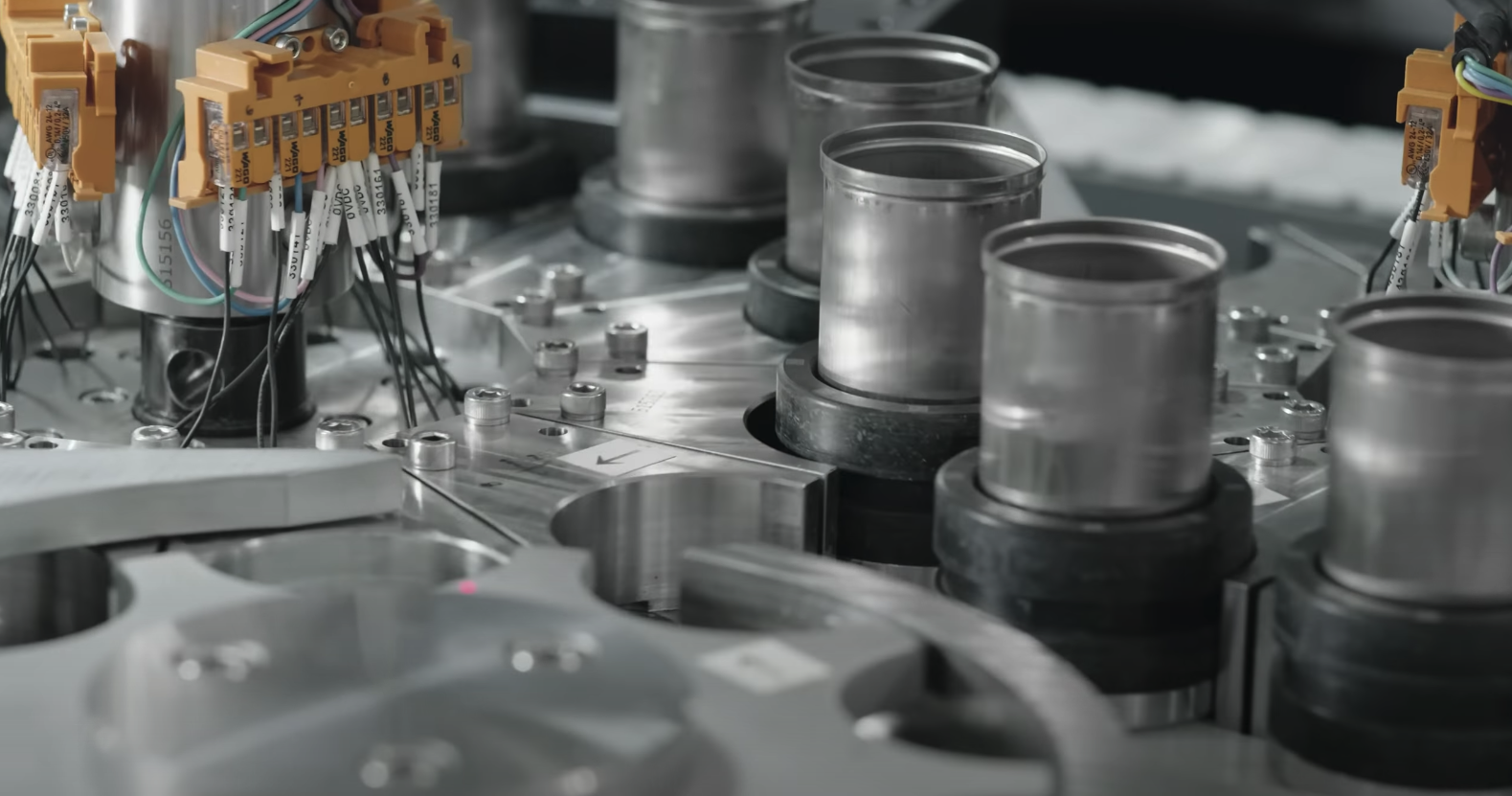

Leaked document shares a glimpse into Tesla’s current 4680 production yields

Tesla has been working hard at perfecting the production process of their new 4680 battery cells at their facility on Kato Road. The process is a balance between increasing throughput (the number of cells produced) […]driveteslacanada.ca

I find it difficult to believe that they would knowingly operate at a 30% yield, if they also know how to operate at a 92% yield. Speaking from bitter experience of operating/commissioning process machinery you simply drown in scrap if you turn the rate up before the yield is under control.

The only way I can make sense of Drew's statement is if there is a very significant cost in dealing with reject cells. Setting aside the complexity of how soon in the various stages of production they can identify a dud cell, I can absolutely believe that this is a costly exercise (however much we might wish otherwise). And the more I think about it the more I suspect that they have very little chance of detecting a dud cell before it is fully produced. So the recycling/disposal/etc is by then as expensive as it possibly could be for a single cell (i.e. one that has yet to go in a pack).

Also remember that the machinery installed at Austin has a theoretical design rate of far in excess of the current rate. So does not have to 'solve' the 80% increased production through a yield increase as it is in fact a throughput increase. The scrap and CoGS improvements that Drew stated are (imho) on a cetus paribus basis, for two lines operating at the same production rate.

One cannot be absolutely sure of the actual yields because there are too few pieces of information. But by knowing the scrap improvement we can see the (infinite) possible pair-wise situations, of which here are two that would fit the situation Drew describes. Of course in this example the cost per cell is notional, but the real issue is the relative cost of making vs scrapping a cell.

View attachment 958612

The 80% rate increase does help in one respect. It enables a fix on the likely Q1 rate from Austin. I'm considering the implications of that.

EDIT : I see @mongo is higlighting much the same thing as I am. But for various reasons I think Tesla are now operating in a high 90s% yield environment, but a very high per cell scrap cost. As I set out above.

Only from a fixed asset amortization basis. CapEx machinery cycle based depreciation and materials are both variable cost and track production.I would be very careful interpreting the Kato road data. We don’t know for certain that the line was running at its full rate.

92% yield running at half line rate is really 46%.

I think - and hope - that your CT ramp is way too slow. I’m about res# 100k and expect about 50% dropout, and hope to take delivery by the end of next year.I've put the various additional snippets of info into my 4680/etc spreadsheet.

If they have a dud-handling constraint then that in turn may mean that the yield-improvement rate is also what sets the speed ramp rate. So the information that they have managed an 80% rate increase from Austin 4680 is tremendously helpful. We know that back in the beginning Kato was at 92% yield even prior to starting Austin production, so that is likely a lower bound on yields.

The overall 4680 project is behind plan imho. By now it should have been supplying both Austin and Berlin. Fortunately the Chinese LFP has bailed out Berlin. And Austin has been reliant for most of its Y production on non-structural Panasonic 2170 I think, at least that is the best match I can get with the snippets of data I can see. (Please correct me if I have missed something significant. ) And in turn that is why Austin production (and stated capacity, per latest Q2 call) is less than Berlin production and capacity. It was not supposed to be this way.

The 868k cells/wk announcement re Kato Rd 4680 at the beginning of the year suggests Kato Rd has flatlined at 1 GWh/yr, which is a long ways off the 10 GWh/yr that came out way back in Oct-2020. We also know the amount of cars produced, and other info re Austin milestones for 4680. This in turn suggests that the focus at present is on improving Austin 4680 throughput (4-lines) , rather than on improving Kato Rd (1-line, I think).

The Austin Y vehicle assembly rate is constrained by the cell supply rate imho.

If the 80%/qtr Austin cell ramp rate can be maintained then by the end of 2024 it might be possible for Austin Y production to be at the max throughput for the originally intended machinery, i.e. 4 lines of 4680 @10GWh/yr per line feeding into 500k per year of Y production @80kWh pack per Y. That seems to have been the original intent.

I think it requires the full intent of the 4680 project to realise the 10 GWh/line capacity. So there are some as-yet-unproven bits that are vital ingredients.

(I also think that the 10% energy per cell improvement in the v2 4680 cell tht was discussed on the Q2-2023 call is less important than the 80% volume increase. Ultimately both are important, but volume matters more at present).

This in turn just about leaves enough room (ullage) in the system to bring the first year of Cybertruck production to market at a low ramp rate, indirectly reliant (via the Austin Y as a decoupling mechanism) on the Kato 4680 and the Panasonic 2170. The Cybertruck will be a real cell hog, so I hope its profitability is commensurate in both GM% terms and GM/kWh terms. It would only be when additional 4680 lines are built (and raw materials found) that the Cybertruck can further ramp. Ditto for the Semi, hence the Sparks expansion.

Berlin will also desperately need 4680 machinery due to the EU equivalent of the US-IRA starting to bite in a couple of years, i.e. the machinery needs to be going in during 2024. (Back where it came from, as it was about to be installed there when US-IRA dragged it across the pond).

Anyway here is my latest reading of the chicken bones regarding the likely implications for Y and CT at Austin if everything goes very well indeed:

(For simplicity I am pencilling in an average CT pack size of 200kWh. Of course it may not be that, we will find out.)

View attachment 958648

View attachment 958655

or graphically

View attachment 958658

and for completeness, re yield implications, using notional cost/cell for explanation ( this table is a repeat of an earlier post to keep it in one place)

View attachment 958657

90%+ yields are indicated in articles like this below, months ago.I won't be able to find a source since it was long ago, but from some insider info yields were 80%+ months ago, but that could have been just for Kato Rd. without DBE being used on both anode and cathode

driveteslacanada.ca

I think I have it figured out: the 40% reduction in scrap bill was total, ... not, per unit.DREW BAGLINO "Yes. First, I’ll just start with a little bit of a production update. So, in Texas, 4680 cell production increased 80% Q2 over Q1, and the team surpassed 10 million production cells produced here in Texas. So, congrats to the team for that. Their focus on yield reduced our scrap bill by 40% quarter-over-quarter, and that resulted in a 25% reduction in cell COGS.

I've been fiddling with this.

Your calculation @Optimeer seems to me to be fine, but I cannot square the result you present - a yield of approximately 30-38% - with other previous information, and I think I can see how to solve this issue.

If you go back to Jan-2022 there were some leaded Kato Rd yield documents that indicated a 92% yield from a line consisting of 14 machines

Leaked document shares a glimpse into Tesla’s current 4680 production yields

Tesla has been working hard at perfecting the production process of their new 4680 battery cells at their facility on Kato Road. The process is a balance between increasing throughput (the number of cells produced) […]

I find it difficult to believe that they would knowingly operate at a 30% yield, if they also know how to operate at a 92% yield. Speaking from bitter experience of operating/commissioning process machinery you simply drown in scrap if you turn the rate up before the yield is under control.

The only way I can make sense of Drew's statement is if there is a very significant cost in dealing with reject cells. Setting aside the complexity of how soon in the various stages of production they can identify a dud cell, I can absolutely believe that this is a costly exercise (however much we might wish otherwise). And the more I think about it the more I suspect that they have very little chance of detecting a dud cell before it is fully produced. So the recycling/disposal/etc is by then as expensive as it possibly could be for a single cell (i.e. one that has yet to go in a pack).

Also remember that the machinery installed at Austin has a theoretical design rate of far in excess of the current rate. So does not have to 'solve' the 80% increased production through a yield increase as it is in fact a throughput increase. The scrap and CoGS improvements that Drew stated are (imho) on a cetus paribus basis, for two lines operating at the same production rate.

One cannot be absolutely sure of the actual yields because there are too few pieces of information. But by knowing the scrap improvement we can see the (infinite) possible pair-wise situations, of which here are two that would fit the situation Drew describes. Of course in this example the cost per cell is notional, but the real issue is the relative cost of making vs scrapping a cell.

View attachment 958612

The 80% rate increase does help in one respect. It enables a fix on the likely Q1 rate from Austin. I'm considering the implications of that.

EDIT : I see @mongo is higlighting much the same thing as I am. But for various reasons I think Tesla are now operating in a high 90s% yield environment, but a very high per cell scrap cost. As I set out above.

@Mungo calculated a increase in yield from 55% to 73%, for the record I calculated ,70% to 98%, but I have low confidence in my calculation.I find it difficult to believe that they would knowingly operate at a 30% yield, if they also know how to operate at a 92% yield. Speaking from bitter experience of operating/commissioning process machinery you simply drown in scrap if you turn the rate up before the yield is under control.

My other thought was that from memory Battery Day occurred before the IRA was proposed or certainly well before any details were clear.Berlin will also desperately need 4680 machinery due to the EU equivalent of the US-IRA starting to bite in a couple of years, i.e. the machinery needs to be going in during 2024. (Back where it came from, as it was about to be installed there when US-IRA dragged it across the pond).

Tesla market cap is bigger than the next nine bigger companies combined. I would say they are the 800 lb gorillaIt is good promotional content. The number of people working on this gear is small and very likely has little to no overlap with the FSD/ Cybertruck teams.

Tesla is no longer a tiny company with just a few engineers to work on a given product.

Guy who‘s brain is as thick as a 2x4 here: I must be missing something. Everything in your post indicates nothing has legally changed. Has a new paragraph four been promulgated and put out into the public domain? Sorry if this comes across as pedantic but I’m truly not seeing any material change in the posted rules based on what your post indicates.Clause 4 on FSD transfer has been updated, new car keeps FSD when sold to someone else.

View attachment 958689

The pic is the new version.Guy who‘s brain is as thick as a 2x4 here: I must be missing something. Everything in your post indicates nothing has legally changed. Has a new paragraph four been promulgated and put out into the public domain? Sorry if this comes across as pedantic but I’m truly not seeing any material change in the posted rules based on what your post indicates.

I'm still not sure the semi doesn't take the 2170 production as the powerwall moves to LFP and Y to 4680. The planned semi production could consume Reno GF 2170 production. I just don't know if the 4680 ramp, behind schedule as it is, will ramp fast enough to get the 4680 production up by 2024 to build Semi with 4680. The 2170 is going somewhere and I assume other than the M3 (due to revamp).My other thought was that from memory Battery Day occurred before the IRA was proposed or certainly well before any details were clear.

In house 4680 production, a cathode plant and Lithium refinery are the perfect response to IRA in addition to any other benefits.

According to Battery Day Cathode changes were an additional 12% per kWh cost reduction, obviously that doesn't kick in until the Cathode plant is built.

My overall take on Drew's comments is that Tesla has fallen over the line on the energy density and cost needed to start CT production, ramping volumes is a work in progress,

The next locations for 4680 production are:-

It is hard to guess what the relative priorities will be, my hunch is that most of the hard slog on the Austin ramp will be complete by the middle of 2024. As far as we know Mexico and Sparks construction has not yet started.

- Berlin (Model Y)

- Mexico (Gen 3)

- Sparks Nevada (Semi)

They may do Berlin next and it may be a simple copy-and-paste of the final Austin lines, IMO Berlin could be a 6 month project, and could be largely complete by the end of 2024, or at least at a stage where local teams can take over.

Anything they learned along the way at Austin, they don't need to learn twice. Austin was the first attempt at high volume 4680 production.

I did ask him once if he owns Tesla shares. He said no, which is great newsI wouldn't get too excited by that tweet. Green seems to live for the days when he can accuse tesla of screwing up. He also rushes out information based on features he sees in code that are not even active.

. But he does make money from Tesla’s bug bounty program - so he does serve a useful purpose.

. But he does make money from Tesla’s bug bounty program - so he does serve a useful purpose.I think I have it figured out: the 40% reduction in scrap bill was total, ... not, per unit.

Mungo? Is that when Sandy and I combine powers?@Mungo calculated a increase in yield from 55% to 73%, for the record I calculated ,70% to 98%, but I have low confidence in my calculation