While Tesla's master plan has proven exceedingly sound, there's more the company could do to help maintain everyone's focus.

Wall Street's affliction with quarterly "results" is not the mindset that leads to long term success, and it can be pointed out until the mantra sticks, which is well after eyes glaze over. Sufficient cash on hand helps too.

Throwing kindling on the detractors' bonfires of vanities by overpromising may also be rethought. Will Elon Musk slow down if those timelines aren't out there? [I don't know.] Internal targets that escape are not the same as public pronouncements by the leadership.

... I reoptimized myself for a slow, steady climb, but mostly doldrums (17 may $330s covering nearer-term sold calls, plus a couple sold far-OTM put spreads). Would have been far better off if I'd just held onto my 18 Apr calls. But here we are again, another day of strong price support. If Monday is strong too, I may need to go more aggressively bullish.

One of those two has been characteristic for Tesla's stock over the company's listed life.

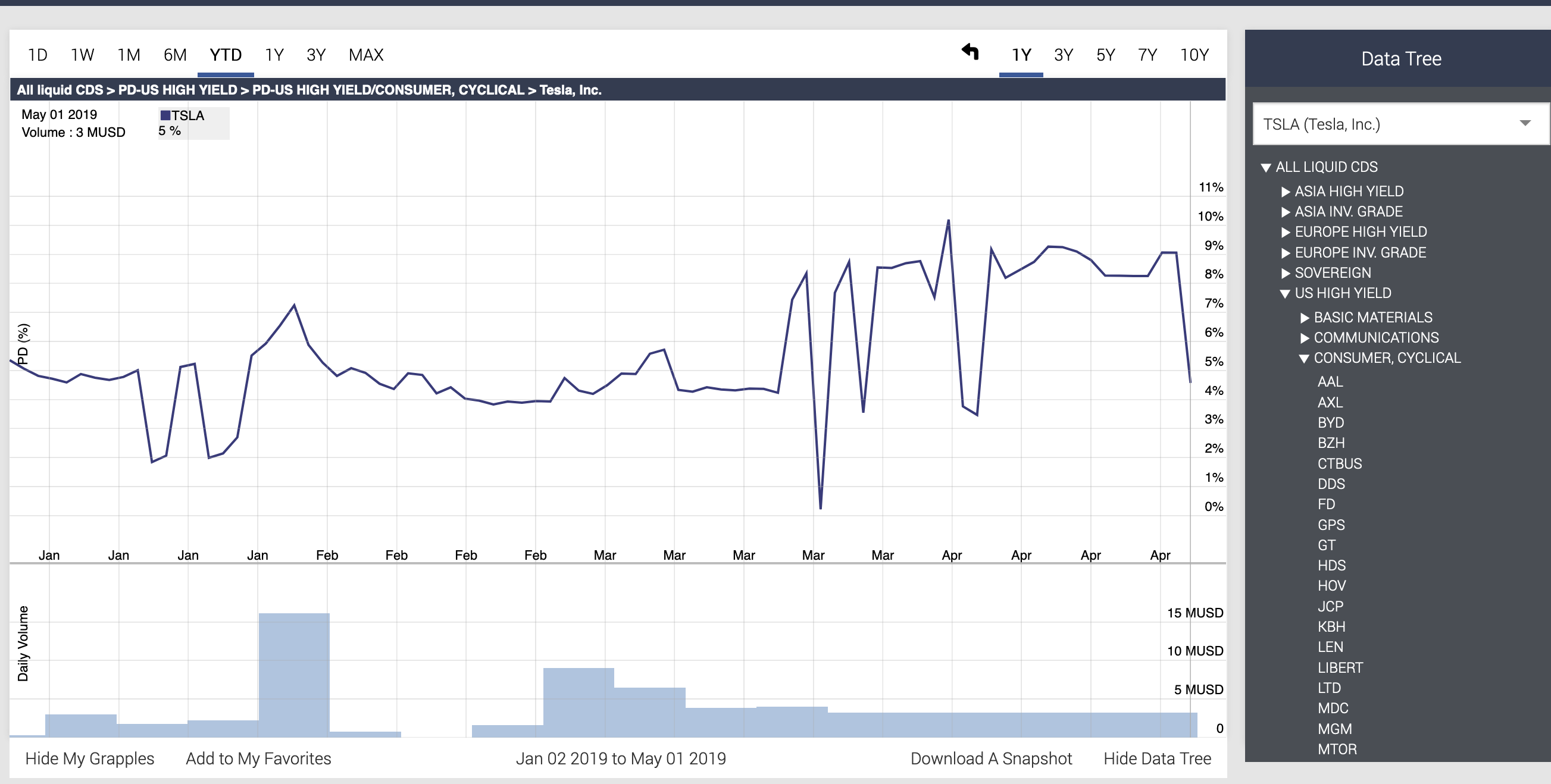

Tesla's current valuation is not low. That's very simple, but simple sometimes does it. The mission is not constantly rocketing stock, and the mission drives real world results.

I think a partnership on any of their future projects that suggests a derisking would be useful.

I like the idea, but wonder who can keep up [and live with the recent level of radiation]. Panasonic remains a cornerstone of Tesla's success. Tesla has also done more limited partnerships, of course. Viz, Mercedes and Toyota a while back. They can both work or be detrimental - the goals and mutually expected benefits matter.

However, it confounds me that Tesla avoids acknowledging and fully addressing US demand and actively attempts to distract from it. Moves such as touting FSD, robo taxis and insurance takes all the air out of the room and do not increase Tesla's appeal to mainstream buyers.

Underlined by moi. I very much like the analogy.

Why don't we see $TSLA boosted by a similar amount?

Excellent question not quite sufficiently answered in subsequent posts?

Earlier today, Paul Graham (founder of Y Combinator) shared some interesting tweets about Tesla.

...

I decided to share my thoughts regarding these tweets and Tesla's software advantage in the following video:

Thank you for a fantastic post.

I do see Tesla as an ever hungry full-stack problem solver par excellence. Software is crucial inasmuch as its mastery helps to mesh with solutions and keep the speed up. In my humble opinion, the habit of always attacking new challenges is the crucial differentiator, coupled with Elon Musk's "intellectual fearlessness". Cannot recall who coined that phrase or where, but it's apt.

What can Tesla do to get out of the SP death spiral it is stuck in ? I have some thoughts.

Helpful post!

One thing I'd like to come back to - my earlier pointer to BMW's pioneering work with flexible production lines that's subsequently been emulated by its German rivals. VW is expressly banking on this capability to manufacture the slew of EVs planned for all its different marques [VW, Audi, Seat, Skoda... ]. I know of one automotive company still greatly puzzled by this ability to create one vehicle offshoot after another, and it helps in the market place. It's not about unifying only two lines - that's just how it started.

Once more, I'll raise the flag for station wagons in Europe and long wheelbase cars in China. It really helps to give customers what they want - nay, crave. Model Y can't come fast enough, albeit in a smoothly orchestrated manner. This is the world's hottest vehicle segment, and I'd be happier if it arrived on the scene earlier.

Reading this thread is rewarding, can expand horizons, and hopefully, just maybe incubate one or the other useful idea in support of Tesla's mission, which should eventually feed through. Thank you!