That Sacconaghi guy may be looking at the quarterly data and use more than 2 datapoints. Since i don't have access to the full report i can't verify that, someone else may want to do that. The chart is taken from the SA article i linked below. While you don't have to agree with the authors conclusions, i'd assume he is able to represent the numbers from the quarterly reports accuratly.

Is Tesla Overstating Margins? - Tesla, Inc. (NASDAQ:TSLA) | Seeking Alpha

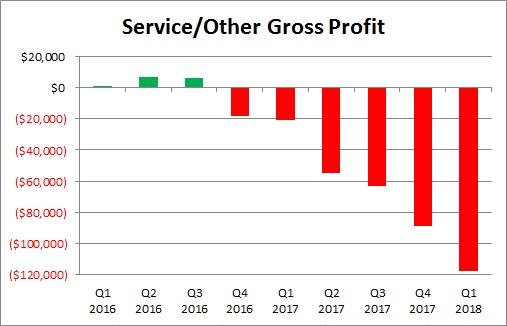

Q1 2018, first revenue then costs

services and other 263,412

services and other 380,969

Q4 2017

services and other 288,017

services and other 376,576

Q3 2017

services and other 304,281

services and other 367,401

Q2 2017

services and other 216,161

services and other 271,169

Q1 2017

Services and other 192,726

Services and other 213,876

OK so first of all, you don't look at margins in dollars, you look at %.

Then you add context, what do you have here, should be mostly the service centers and used car sales.

Used cars sales tend to be break even but vols went up recently as leases expire.

And then they got the scaling ahead of Model 3 and margins are gonna be low because of underutilization.

Not sure if the Superchargers are reported here but likely and again that's an underutilization issue - do remember that almost all the current fleet has it for free but the balance will shift soon.

This is people looking for a negative and pushing a narrative at any cost.

Edit: The argument that can be made is that by delivering cars with issues that need to be serviced right away, Tesla is shifting margins from Auto to this segment. That would mean a large spike in costs and no increase in revenue and we aren't seeing much of that at all. There is some but that can be put on them scaling this ahead of the increase in fleet size with M3. Notable here that M3 deliveries have been low in the reported quarters so any margin shifting would have to be mostly for S&X and that's a bit extravagant.

")