ElectricIAC

Good-Natured Rascal

Not only that but having to be seen in it when they get it back.HAHAHAHA Bolt EV? Then he would be without a car since they are all being recalled, given the repair should be quick. Should be.......

Simply dreadful.

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

Not only that but having to be seen in it when they get it back.HAHAHAHA Bolt EV? Then he would be without a car since they are all being recalled, given the repair should be quick. Should be.......

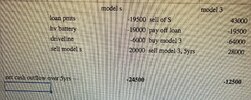

64k - 23k = $41k?Slight correction to your post and the other post, the new car will be 60k with taxes and delivery (plus another 4k to finance for 5 hrs at 5.3%). So really 64k

Right! I attached a spreadsheet with my calculations, but there are assumptions in there, ie depreciation over 5 years of each car64k - 23k = $41k?

Versus $19k remaining loan?

So $22k difference?

Except you don't need to sell the 3 in 5 years, whereas it's more likely you would replace the S. Though that is also dependent on if the part replacements happened, the rest of suspension and such will gave aged too.Right! I attached a spreadsheet with my calculations, but there are assumptions in there, ie depreciation over 5 years of each car

20k was just my best guess of what a 3sec 13yo model s with unlimited super charging and internet assuming 125k milesExcept you don't need to sell the 3 in 5 years, whereas it's more likely you would replace the S. Though that is also dependent on if the part replacements happened, the rest of suspension and such will gave aged too.

Residual value also dependant on what's newer on the car, would recoup some of the cost, unless 20k has that baked in already.

Sure, just expressing the values are interdependent.20k was just my best guess of what a 3sec 13yo model s with unlimited super charging and internet assuming 125k miles

20k was just my best guess of what a 3sec 13yo model s with unlimited super charging and internet assuming 125k miles

That’s impossible. I don’t have a crystal ball… how am I supposed to know if nothing will break down or I’ll have $40,000 of repairsCome on. We need clear math to decide which one is cheaper: buying a brand-new car or keep fixing an old car.

Which math is it?

Well, if you have a warranty...That’s impossible. I don’t have a crystal ball… how am I supposed to know if nothing will break down or I’ll have $40,000 of repairs

My strategy:That’s impossible. I don’t have a crystal ball… how am I supposed to know if nothing will break down or I’ll have $40,000 of repairs

Even with payments on the current car of more than than $15k ?My strategy:

Keep the car until it dies or you’ve achieved your goal of homeownership. Sock away the extra money in the mean time to deal with either or both of those eventualities.

Worst case: battery dies, you decide you don’t want to deal with expensive repairs, and sell it non-running for $15k or so and use the money you’ve been saving to help finance a new car when you actually need one.

Best case: you’ve saved more money for your home down payment, have paid off your car loan in the meantime, and have an easier time qualifying for a mortgage.

I really think this is a terrible terrible time to buy a new car. So much uncertainty related to the economy, upcoming EV tax credits and manufacturer responses to the rules, etc etc etc.

That's why the maths needs to be clear: What if you got the worst?That’s impossible. I don’t have a crystal ball… how am I supposed to know if nothing will break down or I’ll have $40,000 of repairs

Yes, as that outstanding principal will decline rapidly and worst case he can sell the car for scrap to cover the loan, so there’s little to no risk of ending up significantly upside down.Even with payments on the current car of more than than $15k ?

Not upside down, sure. But 20k in equity to 0 is not better off.Yes, as that outstanding principal will decline rapidly and worst case he can sell the car for scrap to cover the loan, so there’s little to no risk of ending up significantly upside down.

I can understand this. As fast as battery/EV technology is likely to advance in the next five years, it may not make sense to sink a lot of money into an 8 year old car. I still think this is just a really low probability though.So in my case I do have cash on hand, however, in my mind I’d be throwing 20k at an 8 year old car with 100,000 miles. Just doesn’t feel right

I’d argue it’s better than pouring that $20k in equity into another depreciating asset with significant associated debt service.Not upside down, sure. But 20k in equity to 0 is not better off.

Sometimes I look at the longer view too, in 7 years will they have needed to get a car? If so, when was the best time to?I’d argue it’s better than pouring that $20k in equity into another depreciating asset with significant associated debt service.

Plus you have to consider the odds of that happening. That would represent the true “worst case”. It’s far more likely that OP will come out ahead. In any case, spending a guaranteed ~$70k to avoid a potential $20k repair is rarely if ever financially smart.

Lots of reasons to buy a new car. Financial savvy is not one of them.

Sure. IMO the answer to that question is the best time to buy a new car is when you NEED one.Sometimes I look at the longer view too, in 7 years will they have needed to get a car? If so, when was the best time to?

")

Agree, just seems a little different when there is an existing car loan...Sure. IMO the answer to that question is the best time to buy a new car is when you NEED one.

Not that that’s when I buy new cars… don’t get me wrong. Sometimes you want what you want.

I will say I do think the WORST time to buy a new car is when you’re aspiring to buy a new home in the next year or two. Keep your DTI as low as possible. A 4-figure car payment can do some serious damage to mortgage qualification and affordability.