The unfortunate thing about the sort of revolutions which happen when the elite is totally intransigent, hostile to the will of the people, and contemptuous of the people -- is that there's always a *massive* amount of collateral damage, essentially innocent people getting killed.

I really would like to avoid this sort of scenario, but to avoid that, people like Nick Hanauer have to get more power and people like Robert Mercer have to have a lot less power.

Maria Antoinetta von Hapsburg (Marie Antoinette)was a German princess who was brought up by Maria Theresa to be responsive to the needs of the people, for purely pragmatic reasons. When her mother wrote her letters asking if she was following her proper lessons as a princess, she responded frustratedly that the French court would not *permit* her to. After numerous failed attempts to do the sort of public outreach which she'd been brought up to do, what any sane nobleman would do to remain popular, she gave up and basically hid in the garden until she was executed.

It does show that this sort of rot is institutional. It's not just an individual nobleman, it's an entire court which has decided to be contemptuous of the common people. Her attempts to perform charity work and make the French government do useful things rather than wasting it on self-indulgence -- which are actually pretty well documented -- were entirely ineffective and didn't save her from being blamed for the crimes of her husband and his court. (More than a little sexism involved there, probably.) Of course she reflexively backed her Austrian relatives when the wars started.

Well said. I'm currently in the throes of trying to model and predict macro shocks of this magnitude and allocate portfolio assets to somehow hedge this kind of risk, but since virtually the entire market is operating as if this historically corrupt and dangerous administration is just business as usual, I'm failing to find answers that corroborate my uneasy hypotheses. One of my favorite street analysts, Ben Carlson who works at

Barry Ritholtz' firm, summed things up reasonably well when he

wrote about "Deep Risk" vs "Shallow Risk" last year (*EDIT - last February, good grief has it only been that long). The linked writings by William J. Bernstein are worth reading as well.

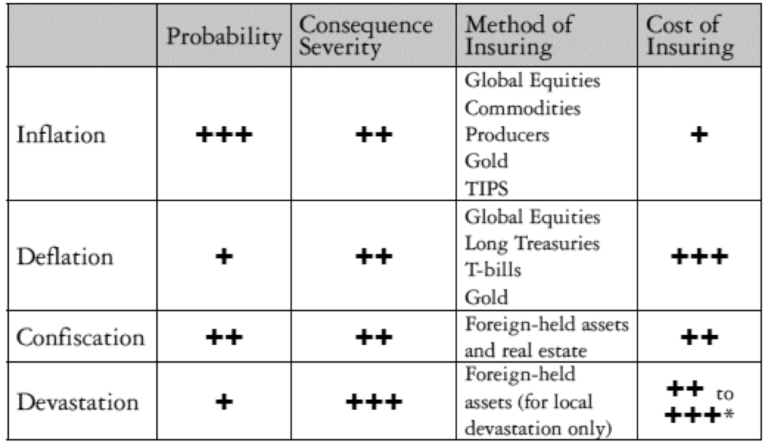

Here is a description and chart from the article outlining these "Deep Risk" types:

- Severe, prolonged hyperinflation, as occurred in Weimar Germany, post-Second World War Hungary and Latin America, in current-day Zimbabwe, and to a lesser degree after both world wars in many other major European nations.

- Severe, prolonged economic recession/ depression with consequent deflation, as occurred in post-1990 Japan, and as often plagued the United States and the rest of the developed world during the Valhalla of the gold standard, especially during the Great Depression.

- Confiscation of assets, as occurred after the communist takeovers in Russia, Eastern Europe, China, and Cuba, or with very high taxation rates in nearly all developed nations in the 1960s– 1980s.

- Devastation, due to international conflict or civil war, as occurred in continental Europe and Japan during the Second World War, or in much of today’s Middle East.

As for fund managers today contemplating portfolio allocation in the age of Trump, the best I can surmise is that many managers have concluded some combination of the following:

1) There is no portfolio strategy that can withstand severe conflict involving the US population directly against a fully compromised government hostile to its own people, so might as well just keep investing at these market highs "hoping for the best."

2) Such conflict, while possible if the current course of this administration continues unchecked, is not going to happen this quarter/this year and I'll be able to cash out before it happens in an orderly fashion. The US population probably doesn't have the will to revolt as long as they are paid, kept in line and/or distracted/entertained.

3) The now almost decade-long effects of QE by the Fed coupled with rising emerging market instability that exceeds US instability mean that US markets are still the least worst option for parking my risk capital.

4) There are a few amazing companies like Tesla doing legitimately great things and we'd rather focus on that than a hypothetical macro shock that we may not even survive if it comes to pass.

It's hard to find good research and analysis that attempts to draw parallels to other eras in human history and incorporate those patterns into an investment thesis, because that's just outside the scope of what most investors demand and/or outside the capabilities of most fund managers. Work that is done is too often peppered with unhelpful conspiracy theories.

Yet, we are living in a world with a "new normal" that is so emphatically outside the realm of what many leaders and fund managers thought possible in their lifetimes, that lack of ability to comprehend and fit this into their worldview often results in outright denial as a standard position.

I vacillate between thinking like the current market does that the US will survive this chapter relatively unscathed and plod along in a resilient can-do fashion, and that we are so far down the wrong path that there is no hedge against this Deep Risk, so might as well keep buying targeted parts of this market until things break more significantly, while holding ample cash reserves and considering foreign asset hedges.

This board and this thread remain largely an oasis of well-reasoned discourse in a desert of vitriol and shallowness elsewhere on the internet, and I remain grateful for everyone's contributions despite not being able to contribute as much myself lately due to other commitments.

To bring things back around, I still believe firmly that if humanity is to survive the unprecedented transition into fully mitigating the drastic incoming effects of climate change, Tesla and its legions of amazing employees, owners, champions and investors will be at the forefront of this effort, but I'm not as confident recently in the market's ability to shove Tesla's share price that much higher in the near term as the fallout from this administration's intentional and unintentional dismantling of decades-old alliances that form the fabric of a stable global economy continues.

Edit: Barry Ritholtz has an

interesting blog post today that may have a few interesting counterpoints. Worth a read (and a follow if you do the Twitter thing, in addition to his employee Ben Carlson).