Fact Checking

Well-Known Member

I think the everybody wants a base model thing is a myth. When people see the difference in a loan payment for a few grand spread out over 4-6 yrs is small, they met opt for bigger battery. This is a generation that thinks not twice about buying 5$ coffee and avacado toast... no offense millenials...

The problem is the many buyers who can normally only afford a $25k-$30k car and who are already straining their finances to get a $35k Tesla. For them a $40k car is simply not an option - and they possibly wouldn't get the loan to begin with.

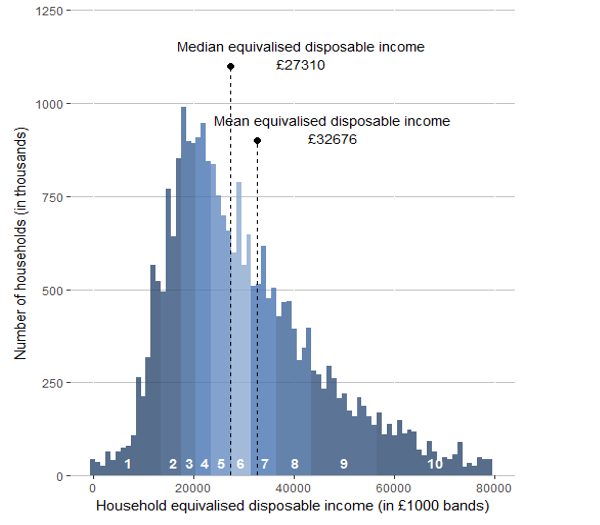

Here's the typical annual household income distribution in the UK (U.S. IRS data is way too coarse unfortunately, but it's similar):

As we can see it on the histogram, "mean" and even "median" income levels don't give a real picture of income distribution: the best figure is "modal" income (not depicted), the peak of the histogram, which is about 65% of "mean" and 80% of "median".

U.S. median disposable income is around $31k, the "modal" max is probably around $25k. For most people the prudent "affordability limit" is around 100% of their annual disposable (post tax) income, and this is roughly how far their banks will allow their car loans to stretch as well.

A lot of people in the $25k-$35k income bracket (~20% of the population) are probably straining to get a Model 3 (giving /r/personalfinance a collective heart attack), and for them the $35k entry price is a godsend.

Put differently: due to the non-even distribution of income, every $1,000 reduction in the entry price moves about +2% more of all car buyers into the "affordability range" of the least expensive Tesla.

In the U.S. alone that's ~2 million more households that can afford a Tesla - and those households alone are buying 300,000 cars per year on average (!).

These entry price reductions are expanding Tesla's addressable market enormously.

Last edited: