The problem is, once you have FSD/Tesla network one of two things happen:

1. Tesla keeps prices the same, scalpers and those wishing to run a small fleet of robotaxis rush in and buy up all the production, creating a multi-year waitlist. Consumers can only buy a car second hand, at grossly inflated prices.

2. Tesla increases the prices themselves.

If Tesla really does get this working fully, and nobody else has them, demand is going to spike like crazy. Assuming you can afford the upfront price, there’s no reason not to buy as many as possible. Each one is estimated to give a 200% ROI per year.

This is my first observation regarding and comment upon Robotaxis. I’m using the post above to demonstrate a flaw I have noticed in mention after mention of this particular transportation mode, as follows.

But first, a slight apology for the didacticism.

Does no one else see the fundamental flaw in the assumptions here, esp. as epitomized ===>by what’s inside the arrows<===?

Tulips indeed.

For anyone else: You’re looking at a 200% ROI? Well, my friend, I’ll settle for 190%.

And

.......So

..............Forth

So the 200% fixed ROI is indeed a mistake, as in reality the total returns are fixed dollar amounts per car per year in the hypothetical scenario of Tesla gaining a robotaxi quasi-monopoly - so the returns will be lowered by the price paid to Tesla, via the initial purchase price and the Tesla Network revenue sharing fees paid to Tesla.

But the original primary point outlined by

@MarcusMaximus is sound: if there's significant earnings via a quasi-monopoly of robotaxis, buyers will bid up the price of Teslas, to a level where there's still a healthy return left beyond market rates. Just like PC makers still made a good living even after they bled most of their margins to Intel and Microsoft.

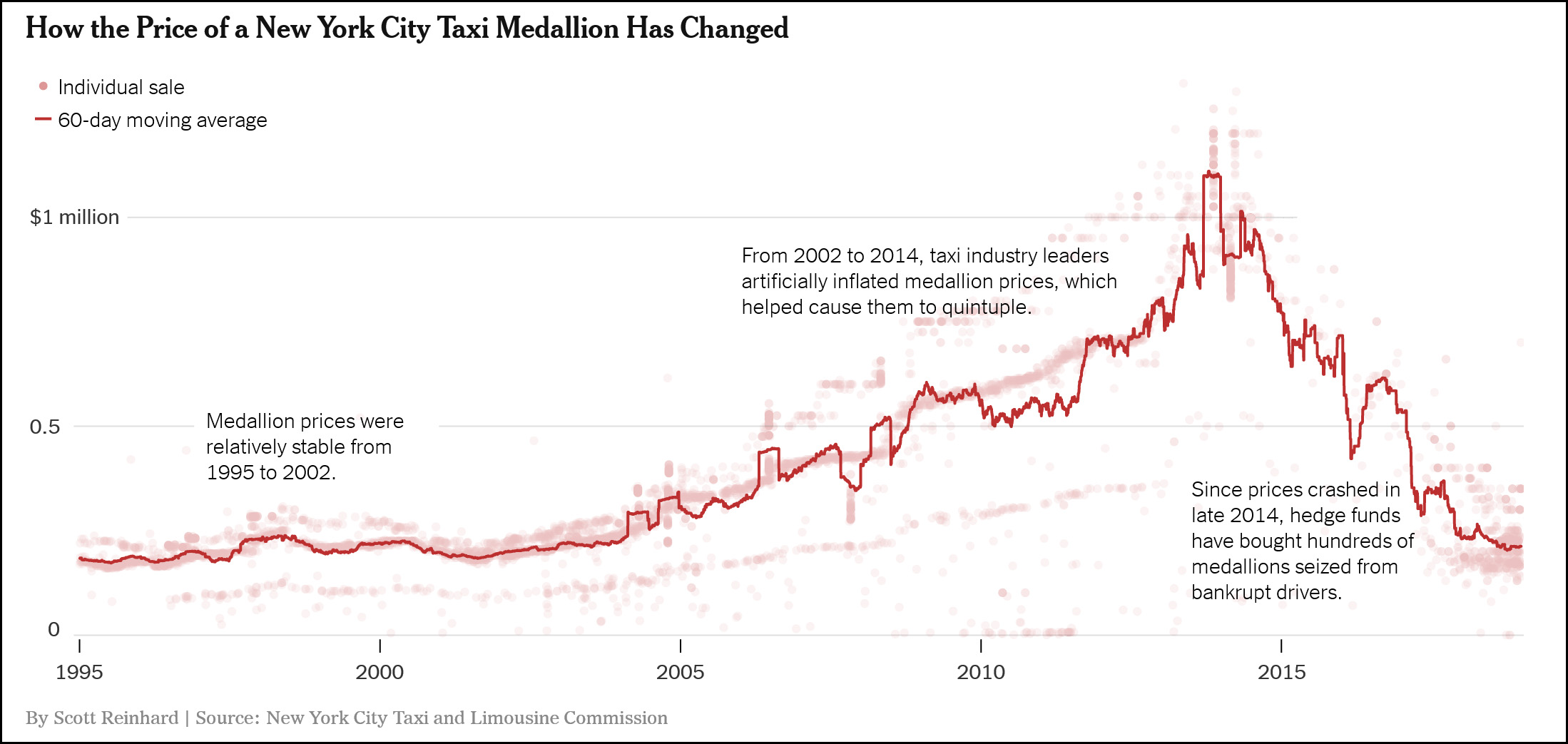

Under that scenario Tesla FSD pricing will, in some markets, mirror NY taxi medallion pricing which reached a peak price of $1m per unit a couple of years ago (until Uber broke the monopoly):

Note how NYC medallions are still worth ~$200k today, even after Uber/Lyft broke the medallion monopoly. Note how the $500k+ pricing phase of medallions lasted about a decade. Medallions were and are real sources of income.

So while artificial scarcity of supply won't generate 200% returns to Tesla buyers

then, but it is going to push the price of every FSD capable Tesla beyond ~$100k return times the number of years the market expects Tesla to keep their FSD monopoly, up to the point of market saturation. Could be well beyond 200% ROI to FSD buyers

now though.

Even bigger returns to Tesla shareholders: assuming Tesla limits supply to 10 million robotaxis globally, ~200 TSLA shares today mean a 0.0001% stake in Tesla, which means the income from about ~10 robotaxi "medallions". 20 TSLA shares today buy the income stream from a single robotaxi, without having to run the robotaxi.

It's not tulips and irrational bubble pricing, but the pricing spike of a (probably temporary) monopoly on an entirely rational basis.

Total return of an FSD "medallion" could move beyond the $1.2m peak of NYC taxi medallions, because an FSD taxi saves labor costs and can charge taxi income to customers, as long as Tesla manages geographical distribution of their robotaxis carefully to not crash taxi pricing in any city. I fully expect Tesla to apply medallion like quotas to robotaxis in major cities covered by the Tesla Network.

And yes, in such a scenario commercial robotaxi operators will initially price out private owners, with Tesla reaping a very high percentage of the FSD monopoly income.

BTW., in reality, should this happen, I expect Tesla to actually

license their FSD technology to other EV makers (but not to gascar makers). The licensing conditions will be dictated by Tesla and will mandate those cars to use the Tesla Network for robotaxi quotas, pricing and revenue sharing.

Tesla will become the Intel-Windows chip-maker-OS-maker entity of the car industry, other carmakers will become the PC makers of that era.

At that point Tesla's revenue expansion will not be capital expensive anymore (shout-out to

@TradingInvest) and will be valued like chip/software monopoly providers, with well beyond a trillion dollars market cap.

There's a

lot of conditions to that happening though - but it's plausible and it's not tulips.