KSilver2000

Active Member

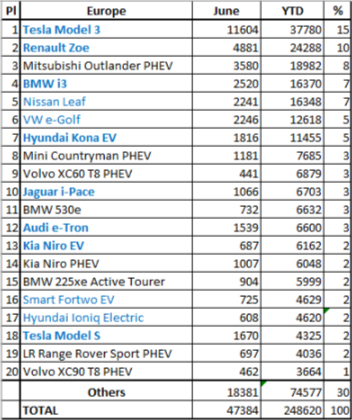

Clear data coming in about competitors floundering to make "Tesla Killer" will at least keep it where it's at.

Made no difference in the past. Leaf, Bolt, Pacifica, etc....doesn’t affect SP, IMO.

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

Clear data coming in about competitors floundering to make "Tesla Killer" will at least keep it where it's at.

You had to wake them didn't you.We interrupt this conversation for an important announcement. Would the short-seller in charge of TSLA whack-a-mole please return to your station. You may be browsing this interminable forum of bulls for grins, but while you've been distracted TSLA is up a full dollar! Much more and the bulls can get... well... bullish. That is all.

No powerful rebound after big drop after last ER.

Looks like a slow slide down again to $177.

Damn it's a long way to 52wk high at $379!

Thoughts?

No real catalyst until next production/delivery report at the beginning of October. So, we're basically stuck here for a while.No powerful rebound after big drop after last ER.

Looks like a slow slide down again to $177.

Damn it's a long way to 52wk high at $379!

Thoughts?

EVERYONE agrees the EV market is going to be huge, there are still some delusional people thinking Porsche or audi will have a big chunk of it.

No real catalyst until next production/delivery report at the beginning of October. So, we're basically stuck here for a while.

There aren't any other unknown special announcements expected before the end of the year that could really move share price. A solid Shanghai GF3 ramp up with high quality vehicles could help. Wildcard is any improvements in FSD, but that's an impossible to predict timeline. Macros are another factor.

No powerful rebound after big drop after last ER.

Looks like a slow slide down again to $177.

Damn it's a long way to 52wk high at $379!

Thoughts?

What's the probability, given that Elon will be in Shanghai the last few days of August to speak at the World AI conference, and that he'll probably stop by the new factory, that he's also there to christen a ceremonial first M3 off the GF3 assembly line as they slowly summon the new beast to life? 0%, 5%, ...100%?

In the end, this is a crappy deal for the consumer in the long run just like any other PV PPA/lease deals.

Tesla may get some dumb nuts to bite, but not many once you dig down into the details.

I hope everyone watched Rob Baron on CNBC Squak Box - All the FUDster panelists were very quiet when he spoke about Tesla

Good new info! This year, revenues will be about $27 billion. Cost 70% less to build in China than in US. 30% less to build than a year ago. Wow!

It's hard to tell who is being sarcastic and who really believes this crap.$800 million in credits this year, probably a billion.

What's the probability, given that Elon will be in Shanghai the last few days of August to speak at the World AI conference, and that he'll probably stop by the new factory, that he's also there to christen a ceremonial first M3 off the GF3 assembly line as they slowly summon the new beast to life? 0%, 5%, ...100%?

What's the probability, given that Elon will be in Shanghai the last few days of August to speak at the World AI conference, and that he'll probably stop by the new factory, that he's also there to christen a ceremonial first M3 off the GF3 assembly line as they slowly summon the new beast to life? 0%, 5%, ...100%?

0.01%

If this happens, it is a publicity stunt. I think Tesla has better things to spend their time on.

It would essentially be what Tesla did for the Model 3 launch in the US, 30 cars, probably hand-made.

It would essentially be what Tesla did for the Model 3 launch in the US, 30 cars, probably hand-made.

“Though Tesla is widely portrayed as a “disruptive innovator,” its major innovations are in fact of the sustaining variety. Electric drive can improve an ownership experience by eliminating emissions, reducing fuel costs, and improving acceleration, but it doesn’t fundamentally alter any of these consumer values, which have been present since the dawn of the industry. This makes electric drive no more “disruptive” than any of the technologies that have steadily improved the efficiency and emissions of internal combustion vehicles over the last century, most of which have been widely diffused across the industry without leaving a single automaker with a sustainable technological advantage. One of the great ironies of Tesla is that it is so widely seen as being a disruptive innovator when in fact it just barely missed the opportunity to fully capitalize on what is likely to be the first truly disruptive innovation to hit the auto industry in a century: shared autonomous vehicles. By enabling an access model instead of an ownership model, in which privately owned cars are replaced by on-demand access to fleets of self-driving mobility pods, autonomous drive has the clear potential to disrupt both consumption patterns and the fundamentals of the business. Musk’s awkward attempt to bend Tesla’s private ownership model to fit the new autonomous-drive–enabled paradigm in the Master Plan Part Deux illustrates how closely Tesla missed this historic opportunity to disrupt the auto industry. To truly lead this disruption, Tesla would have to walk away from core brand values—performance, styling, prestige—and reinvent the company around low-cost, highly reliable, shareable pods with an emphasis on its weakest points: interior comfort and durability. The one area where Tesla has had undeniable success, namely creating electric cars with performance and styling that appeals to existing customers, proves that its innovations are sustaining rather than disruptive. One of the fundamental cornerstones of the Tesla mythology is the belief that established automakers either can’t or won’t build electric cars in meaningful volumes. This theory relies heavily on crude interpretations of what Clayton Christensen called “The Innovator’s Dilemma,” which suggests that investments in existing technologies and business models make “incumbent” companies less able to establish new businesses in response to innovations. Christensen and his coauthors explain this dilemma in an article called “Innovation Killers: How Financial Tools Destroy Your Capacity to Do New Things”: Executives in established companies bemoan how expensive it is to build new brands and develop new sales and distribution channels—so they seek instead to leverage their existing brands and structures. Entrants, in contrast, simply create new ones. The problem for the incumbent isn’t that the challenger can outspend it; it’s that the challenger is spared the dilemma of having to choose between full-cost and marginal-cost options. We have repeatedly observed leading, established companies misapply fixed-and sunk-cost doctrine and rely on assets and capabilities that were forged in the past to succeed in the future. In doing so, they fail to make the same investments that entrants and attackers find to be profitable. This logic is popularly applied to the incumbent automakers, which are presented as having to adapt new technologies to their existing structures and capabilities, whereas Tesla is able to make itself in the image of new technologies and new possibilities. Put simply, this view holds that Tesla need not compromise or destroy an established business based on internal combustion technology to create a new business based on batteries and electric cars. As Tesla’s market cap climbed to match or exceed that of “incumbent” automakers whose production volume and profits eclipsed the upstart, this logic was increasingly trotted out as justification for its frothy valuation. But the perception that automakers wouldn’t invest as aggressively in electric vehicles as an unencumbered startup like Tesla was just that: a perception. This belief may have matched the popular understanding of The Innovator’s Dilemma, but it simply didn’t match the facts on the ground.”

— Ludicrous: The Unvarnished Story of Tesla Motors by Edward Niedermeyer

Ludicrous: The Unvarnished Story of Tesla Motors

This disconnect between Tesla’s mass-market struggles and its pricey next-gen hype left its latest spectacle feeling oddly hollow. Having largely subsisted on prototypes and promotion for much of the past decade, Model 3 was the company’s chance to prove that it could deliver the affordable electric car it had been promising since 2006. But when it found itself mired in “production hell,” its answer was to double down on even flashier but farther off prototypes. It was as if Tesla was becoming a parody of itself. The gargantuan semitruck embodied the company’s lack of focus, branching out into a product class that had nothing to do with the vehicles Tesla made or the markets it served. If Tesla’s cars had to make up for their shortcomings in reliability and affordability with style and performance, how were they supposed to sell an unproven semi to trucking companies that live and die on cost and uptime? A sexy drag-racing tractor-trailer truck may have fit in with the goofy, overgrown kid aspect of Musk’s personal brand, but it clashed badly with the perception that Tesla was finally growing up and becoming a real car company. Worse still, an electric semi was simply not a particularly promising concept. The limited range, long recharge times, heavy batteries, and high cost of an electric vehicle are a fundamentally poor match to the long-range, weight-hauling, moneymaking mission of a tractor-trailer truck. Meanwhile, Tesla was missing out on a far more suitable commercial use for its technology: short-range delivery vehicles that could enhance a business’s brand while ensuring that deliveries would continue even in cities that were moving toward bans and restrictions on diesel and gas cars. Eliminating the pollution caused by trucks crawling through urban gridlock could have profound environmental and public health benefits without requiring the absurdly optimistic costs, specifications, and unique charging network needed to make an electric semi seem like a viable proposition.

Going from the first shovel in the dirt to the first car off the line in 8 months is the kind of publicity stunt i'm all for as long as it doesn't cause a meaningful delay in what they have to do to spin up the line. it's also the sort of stunt that'll make a few shorts poop their pants and draw in more big money longs to establish their positions as the inevitable becomes ever more obvious...0.01%

If this happens, it is a publicity stunt. I think Tesla has better things to spend their time on.

What's the probability, given that Elon will be in Shanghai the last few days of August to speak at the World AI conference, and that he'll probably stop by the new factory, that he's also there to christen a ceremonial first M3 off the GF3 assembly line as they slowly summon the new beast to life? 0%, 5%, ...100%?