Welcome to Tesla Motors Club

Discuss Tesla's Model S, Model 3, Model X, Model Y, Cybertruck, Roadster and More.

Register

Install the app

How to install the app on iOS

You can install our site as a web app on your iOS device by utilizing the Add to Home Screen feature in Safari. Please see this thread for more details on this.

Note: This feature may not be available in some browsers.

-

Want to remove ads? Register an account and login to see fewer ads, and become a Supporting Member to remove almost all ads.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Tesla, TSLA & the Investment World: the Perpetual Investors' Roundtable

- Thread starter AudubonB

- Start date

I guess enough people are asking Gary the same question, so Gary clarified. Reason given is that receiving 3-4% on the $19B cash does not compare favourably to the 20% IRR for the stock buyback. And his Oct timing is to give time for Moody and S&P to revise the rating prior to the buyback.Gary has added point # 5 to his Tesla catalysts: Buyback in October.

I find Gary to be very conservative; so this prediction of a buyback in October is a bit out of character.

My thinking is that Tesla would not entertain a buyback for a few years. Perhaps in early 2025 when cash on hand exceeds $80b.

View attachment 831544

insaneoctane

Well-Known Member

Interesting. So, our P/E has been steadily declining (sans a few bumps) since November 2021.Ok - My Price to P/E Graph earlier had mistakes :-(

I've fixed it up and I've extended it back as far to July 1 2020, so we have a full 3 years of data in it now:

It will be interesting to see how the P/E ratio moves over this Q.

View attachment 831948

Tho Elon wants more liquidity due to possible economic slow down or random China shut downs, he may not oppose to stock buy back announcements as it's a true protector of share price from short raids or macro dumps. The more buyback announcements, the less appealing it is for people to buy puts or shorts Tesla. For this reason Elon might do it since he hate shorts.I guess enough people are asking Gary the same question, so Gary clarified. Reason given is that receiving 3-4% on the $19B cash does not compare favourably to the 20% IRR for the stock buyback. And his Oct timing is to give time for Moody and S&P to revise the rating prior to the buyback.

damonbrodie

Member

I created it in google sheets:Great chart, did you make it or is there a site to make others like it? Would like to see one for the FAANG gang. I'd imagine similarities

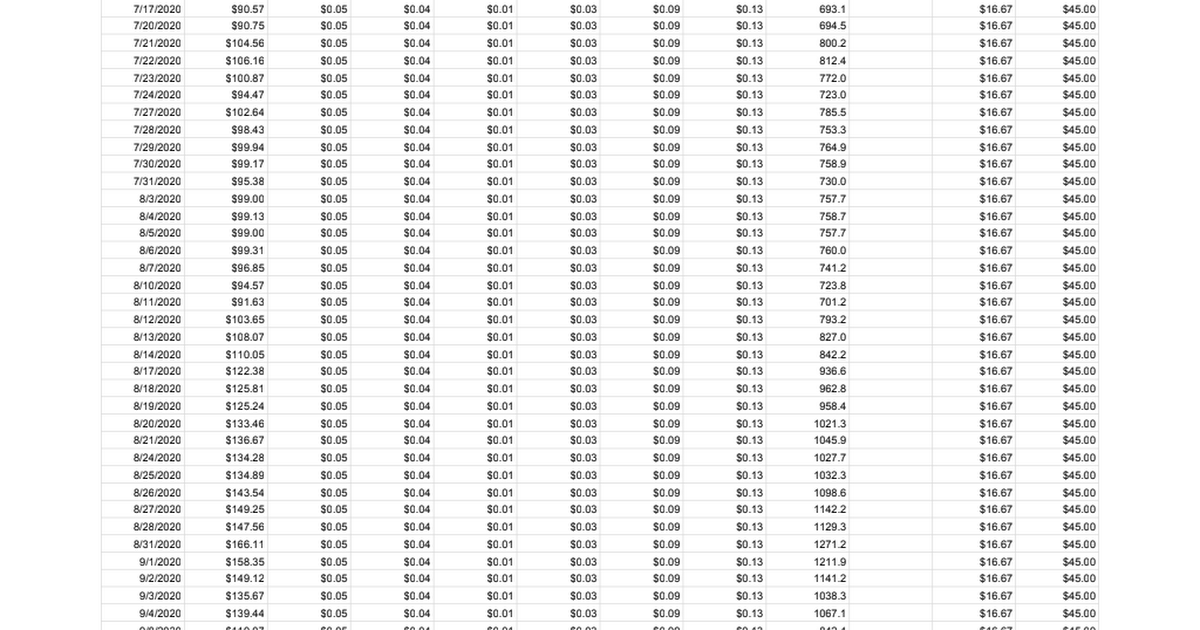

TSLA Share and PE Analysis

Trailing PE Trade Date,Share price,Q-4,Q-3,Q-2,Q-1,Current Q,EPS TTM,P/E,Q-1 - * 500,Q * 500 7/1/2020,$77.24,$0.05,$0.04,$0.01,$0.03,$0.09,$0.13,591.2,$16.67,$45.00 7/2/2020,$81.51,$0.05,$0.04,$0.01,$0.03,$0.09,$0.13,623.8,$16.67,$45.00 7/6/2020,$83.59,$0.05,$0.04,$0.01,$0.03,$0.09,$0.13,639.7,$...

StealthP3D

Well-Known Member

View attachment 831959

His beating the drum for buybacks seems to me like financial engineering merely to boost the stock price, and doesn't seem to be in tune with the Tesla mission.

Gary Black is extremely motivated for the stock price to rise.

He is responsible for not just himself, but all his fund owners.

Gary Black has poor fundamental analysis compared to masters like Ron Barron and if he and his clients finds this little dip we've had the last several months troublesome, well, it's his own fault for taking on clients that don't understand reality and calling himself an investment advisor and/or fund manager. He's worse than a brokerage analyst and that's saying a lot.

Worse, he has fundamental misunderstandings about Tesla that run deep and wide. In short, he's an idiot. If you want proof, it's in the first Tweet above which makes absolutely no sense. Somehow, he thinks the F-150 Lightning launch is relevant to Tesla (and Twitter?). I get the feeling he thinks the fact that the Lightning launched before the Cybertruck is somehow a negative (as if they are each other's primary competition). I would argue the Lightning launch is completely irrelevant to Tesla's positioning in the market. How he thinks the Lightning matters to Tesla is beyond me.

I can't for the life of me figure out why any Tesla investors give two hoots about what he says.

Bet TSLA

Active Member

Yeah, I can just picture the panic at Tesla. "If we don't do a stock buyback soon, we might lose credibility on Wall St.!!!"I guess enough people are asking Gary the same question, so Gary clarified. Reason given is that receiving 3-4% on the $19B cash does not compare favourably to the 20% IRR for the stock buyback. And his Oct timing is to give time for Moody and S&P to revise the rating prior to the buyback.

Gary Black is clueless.

If I remember correctly local elec. utilities have their rate and policies set by TVA. The State PSC has no jurisdiction. And TVA has little oversight. When I did my home solar project it had to be approved by TVA by within it's meager solar budget. I had to agree to sell it to TVA at a set rate and I couldn't get a building permit without a TVA contract. To make matters worse TVA sends out notices to those of us who have solar that we cannot toke credit for our solar investment publicly because TVA has given that credit to some other entity, probably a greenwash. Basically we have a monopoly unregulated federal agency that has complete control subject to Congress.By chance I'm keeping an eye on the Knoxville market and will let you know if Tesla or any other good options pop up.

Calling these utility solar options "community" is insulting. They're trying to pull the same thing in PA. Fracking lobby keeps the legislature from allowing community solar projects, then the utility lobby comes along and wants to extend their monopoly to solar. Horseshit.

I'm in the process of writing up some communications/proposals/petitions in support of community solar legislation on PA. It'll be posted here in the Energy forum for sure.

Artful Dodger

"Neko no me"

Tho Elon wants more liquidity due to possible economic slow down or random China shut downs, he may not oppose to stock buy back announcements as it's a true protector of share price from short raids or macro dumps. The more buyback announcements, the less appealing it is for people to buy puts or shorts Tesla. For this reason Elon might do it since he hate shorts.

Indeed. Having a standing 'buy-back' policy would enable Tesla to take advantage of those frequent artificial/contrived dips in the SP (a few times per year). Thus, Tesla puts a floor on the SP, and may 'discourage' further monkey business going forward.

However, a continuous high SP works against some of Tesla's internal provisions for stock-based compensation (SBC), where employess are allowed to buy a certain amount of TSLA shares at a reduced price vs. the Market, but based on the lowest Market SP reached during the previous incentive period (2x per year, IIRC).

I think these two mechanisms can be made to work together. However, it does require that Shortzes continue to massively undervalue Tesla as a company (looking at egregious pink-buoy Craig Irwin/Roth Capital Partners). One of these parties will foot the bill, and that right shortly.

I like it. Make it so.

Cheers!

insaneoctane

Well-Known Member

Yes, but...I guess I'd need to know how big my cash warchest for a 1T and rapidly growing company needs to be, because I think Tesla is past capital raises. So after they fund their internal capital needs and have a big enough warchest, I think using some in the way Gary recommends makes sense to me...I guess enough people are asking Gary the same question, so Gary clarified. Reason given is that receiving 3-4% on the $19B cash does not compare favourably to the 20% IRR for the stock buyback. And his Oct timing is to give time for Moody and S&P to revise the rating prior to the buyback.

Words of HABIT

Active Member

These CNBC business analysts are just some of many bad players that Tesla should be taking to court in defamation suits.

There are however things in Tesla’s control that could push its PE higher even in a bad macro environment such as -

-FSD wide release and revenue recognition along with push for subscription model and that recurring revenue actually start to show up in earnings

- Tesla insurance continued push and having that high margin revenue start to make a material impact on earnings

- Opening up superchargers in US, opening up subscription revenue

- Tesla Energy finally going into S curve of production and thus margins on Tesla Energy finally start trending towards total gross margin

I don't think Insurance nor opening up the Superchargers would impact PE all that much, at least not until either has sizable revenue coming in from each, but that would be down the road. Same with Tesla energy in my opinion.

However, I do feel FSD hitting level 5 could increase the PE significantly simply due to the market implications such an event would portend for the future. That's the one thing Tesla could do which I think would grow the PE almost instantly.

Last edited:

The Accountant

Active Member

Sam Alexander does a great job pointing out CNBC's latest lies about Tesla's Q2 performance.

These CNBC business analysts are just some of many bad players that Tesla should be taking to court in defamation suits.

It's one thing to get the Bitcoin/Free Cash Flow comment wrong . . . .I will give Andrew Sorkin (a communications major) the benefit of a doubt that he innocently does not understand the cash flow statement . . .BUT to call TSLA bulls sheeple is unforgiveable in my book. That was unnecessary. Does not sit well with me. If I am channel surfing and see Andrew on the screen, I will move on quickly to the next channel. Don't care for anything he has to say at this point.

I sympathize and agree with you feelings but this would be a terrible use of the company's resources because Tesla would lose. And how would it look if the headline is Tesla loses defamation suit. To much of the public that would confirm that the media is correct. Tesla would clearly lose because 1the defense would be no malice but simple mistake or 2 opinion not factual defamation and 3 no damages in fact the stock has gone up and Tesla could not show that it was damaged. While I agree with you viscerally it would do the company no good and would only enrich many lawyers.Sam Alexander does a great job pointing out CNBC's latest lies about Tesla's Q2 performance.

These CNBC business analysts are just some of many bad players that Tesla should be taking to court in defamation suits.

StarFoxisDown!

Well-Known Member

It’s not about those things actually effecting PE or earnings in a big way in a mathematical sense.I don't think Insurance nor opening up the Superchargers would impact PE all that much, at least not until either has sizable revenue coming in from each, but that would be down the road. Same with Tesla energy in my opinion.

However, I do feel FSD hitting level 5 could increase the PE significantly simply due to the market implications such an event would portend for the future. That's the one thing Tesla could do which I think would grow the PE almost instantly.

When Tesla has those things flowing into earnings and can start showing material SAAS revenue, then TSLA will trade a higher PE because more future revenue will be valued as SAAS revenue, which is much higher margin.

It’s the difference in valuation between lower margin revenue and high margin revenue, hardware margin revenue vs software high margin revenue

Last edited:

It’s not about those things actually effecting PE or earnings in a big way in a mathematical sense.

When Tesla has those things flowing into earnings and can start showing material SAAS revenue, then TSLA will trade a higher PE because more future revenue will be valued as SAAS revenue, which is much higher margin.

It’s the difference in valuation between lower margin revenue and high margin revenue, hardware margin revenue vs software high margin revenue

Ideally, yes, if the market allows it. My hunch is the MM's will do everything they can to hold the share price down from here on out, no matter how awesome Tesla becomes. And manipulating the PE is their best tool to do so by utilizing naked shorts and other stock manipulation tools they have.

It's just what I'm expecting to see play out over the next few years. We all have seen how much effort the MM's put into holding TSLA down, my gut feeling is that's not going to stop anytime soon...

damonbrodie

Member

I think this is why Elon says Tesla is "nothing" without FSD. While clearly Tesla is not "nothing", they will slowly just become a "car company" over time. (Let's ignore Solar/Energy for the moment). Of course they are a very well run car company and their profits and zero debt are very desirable.I don't think Insurance nor opening up the Superchargers would impact PE all that much, at least not until either has sizable revenue coming in from each, but that would be down the road. Same with Tesla energy in my opinion.

However, I do feel FSD hitting level 5 could increase the PE significantly simply due to the market implications such an event would portend for the future. That's the one thing Tesla could do which I think would grow the PE almost instantly.

The crazy P/E ratios of the past were because people were banking on the profits that we're now starting to see. Now that we're seeing the profits the P/E is adjusting to the new reality.

FSD, robotaxi and Bot are what will propel them into the stratosphere P/E wise. Personally I'm waiting for AI day 2 - Elon said on the earnings call that its going to be big.

FSD, robotaxi and Bot are what will propel them into the stratosphere P/E wise. Personally I'm waiting for AI day 2 - Elon said on the earnings call that its going to be big.

I know it's unrealistic, but a large part of me thinks we'll see an actual Optimus Subprime walking around and doing simple tasks at AI Day #2. Probably wishful thinking on my part, but it's okay to dream big now and then...

StarFoxisDown!

Well-Known Member

Well, MM’s can’t control buying volume. And the reality is that if Tesla can prove their SAAS revenue model, it will bring in a ton of buying volume from the part of the market that gives high PE valuation for that high margin revenue.Ideally, yes, if the market allows it. My hunch is the MM's will do everything they can to hold the share price down from here on out, no matter how awesome Tesla becomes. And manipulating the PE is their best tool to do so by utilizing naked shorts and other stock manipulation tools they have.

It's just what I'm expecting to see play out over the next few years. We all have seen how much effort the MM's put into holding TSLA down, my gut feeling is that's not going to stop anytime soon...

That is the dynamic that will change when SAAS is proven out on a material scale if those items I listed come to fruition for Tesla

Similar threads

- Locked

- Replies

- 0

- Views

- 3K

- Locked

- Replies

- 0

- Views

- 6K

- Replies

- 6

- Views

- 5K

- Replies

- 6

- Views

- 11K

- Locked

- Replies

- 27K

- Views

- 3M