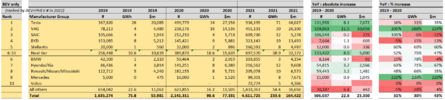

Gigapress

Trying to be less wrong

My margin situation isn't quite complicated but there is an crucial difference between what I'm doing and the scenario described, in which the investor sold for the margin call, but did not reverse the process by buying on the way up, thus ending up with a lower margin percentage than at the beginning. The investor started with $14k of stock with a $4k loan (10/14 = 71% real equity and 29% debt), but ended with $10k of stock with a $2k loan (8/10 = 80% equity, 20% debt). If the investor had been buying on the way back up, then, to a first approximation, every share could be repurchased and they would be back at $14k stock/$4k debt. I might be fundamentally misunderstanding something about how this works though.Let's say you own $10,000 of a stock that you are confident in. You're so confident, that you decide to use 40% margin to buy another $4k worth of the stock on margin, totaling $14k worth. Stock drops 50%, and you get a margin call. Your $14k worth of stock is now worth $7k, and you are forced to sell $2k worth. You now have $5k worth of stock, $2k of which is still on margin. Stock goes back up to it's original value, and you now have $10k worth of stock, $2k of whch is on margin. The stock is at the same price as originally, but you've lost $2k worth to margin calls.

I'm sure your situation is much more complicated, as you mentioned many margin calls on the way down, and most likely buying back on margin on the way up;

however, each time you get a margin call and are forced to sell, and then buy back in at a higher price (once you have more margin to play with), you are losing a portion of your original wealth due to being forced to buy back in at higher prices than when you were forced to sell due to margin calls.

This effect will always be nonzero with this strategy, but I'm keeping the effect close to zero by monitoring my account daily and buying back stock quickly after the margin credit flips back into positive territory.

For example, let's imagine I had a margin deficit triggered by TSLA falling below $240 and I sold to cover at $239 and for simplicity's sake, let's imagine I did not sell extra in order to buy calls on a 30% discount. Then, if and when TSLA gets back to perhaps $241 or so, I'll have enough margin credit and will rebuy as much as I sold, or maybe approximately 2/239 = 0.8% less because the price is now higher. Losing 0.8% wouldn't be ideal, but if my prediction is correct that TSLA will increase majorly in the long run, then in the long run this drag on my returns will be greatly outweighed by the leverage advantage of being able to hold nearly twice as many shares than I otherwise could with my finite resources. I also mitigate this drag by roughly aiming to stay a bit back from the maintenance margin line to avoid tax consequences of more selling and also "pattern day trader" status, but TSLA has been so volatile that it has still caused margin calls.

If TSLA were to never recover, or worse, if the company went bankrupt and my shares were worth zero, then I'd have a problem. However, like I wrote in my earlier post, I have set this up to a risk limit such that the "problem" would be running out of excess savings and needing to go find cushy first-world paid engineering employment again while living a frugal version of the American 2022 middle-class lifestyle, which is an outcome the vast majority of humans who have ever lived would love to have as their best-case scenario. I'd also come out of the experience knowing I applied as much pressure as I could to keep this company well-capitalized and tried to make millions for charitable purposes, so I would anticipate no regrets.

There's also the fact that if Tesla does not achieve something resembling the rapid success I'm forecasting and is worth $750B or less forever, my future as a human on this planet is looking pretty sketchy no matter how much money I have. I'm not really hedged against a Tesla bankruptcy scenario because I'm not convinced a legitimate hedge actually exists. I wish so much didn't depend on this one organization, but nobody else is getting the job done fast enough and I'm stuck on this warming rock with everybody else whether I like it or not. The Holocene mass extinction and biodiversity loss are much more concerning to me than my wealth or lack thereof. For better or for worse, capital allocation decides much of what happens in this world and if I can use leverage to increase my voting power on what needs to happen, then I'm going to use that tool, especially since I expect that the leverage is very likely to make me wealthier anyway.

Yes that's another important factor. Ultimately I'm playing the odds based on my firm belief that my margined TSLA position will appreciate faster than the margin interest rate.Note that this example also doesn't consider the margin interest rate your broker is charging you to borrow money as well.

There seem to be quite a few in this camp who really have no idea what his plans are for creating his decades-long dream of X.com

There seem to be quite a few in this camp who really have no idea what his plans are for creating his decades-long dream of X.com