Doggydogworld

Active Member

The 15% thing really only applies to the drive train. The rest of Tesla's COGS mostly come from the same vendors who supply ICE. Those parts are way, way down the cost curve.One way to think about this - I believe the car industry has consistently been on a trajectory where every doubling of the total units manufactured to date is worth another 15% cost reduction. For the ICE market with a few billion cars manufactured over all time, that means that another few billion need to be manufactured to find the next 15% cost reduction.

For TSLA with maybe 1M cars manufactured, the next 1M will lead to another 15% cost reduction; then 2M manufacturing for another 15% cost reduction, etc.. TSLA might see 4 or 6 of these 15% cost reductions piling on top of each other over the next decade. That will be a very tough cost curve for the ICE industry to keep up with.

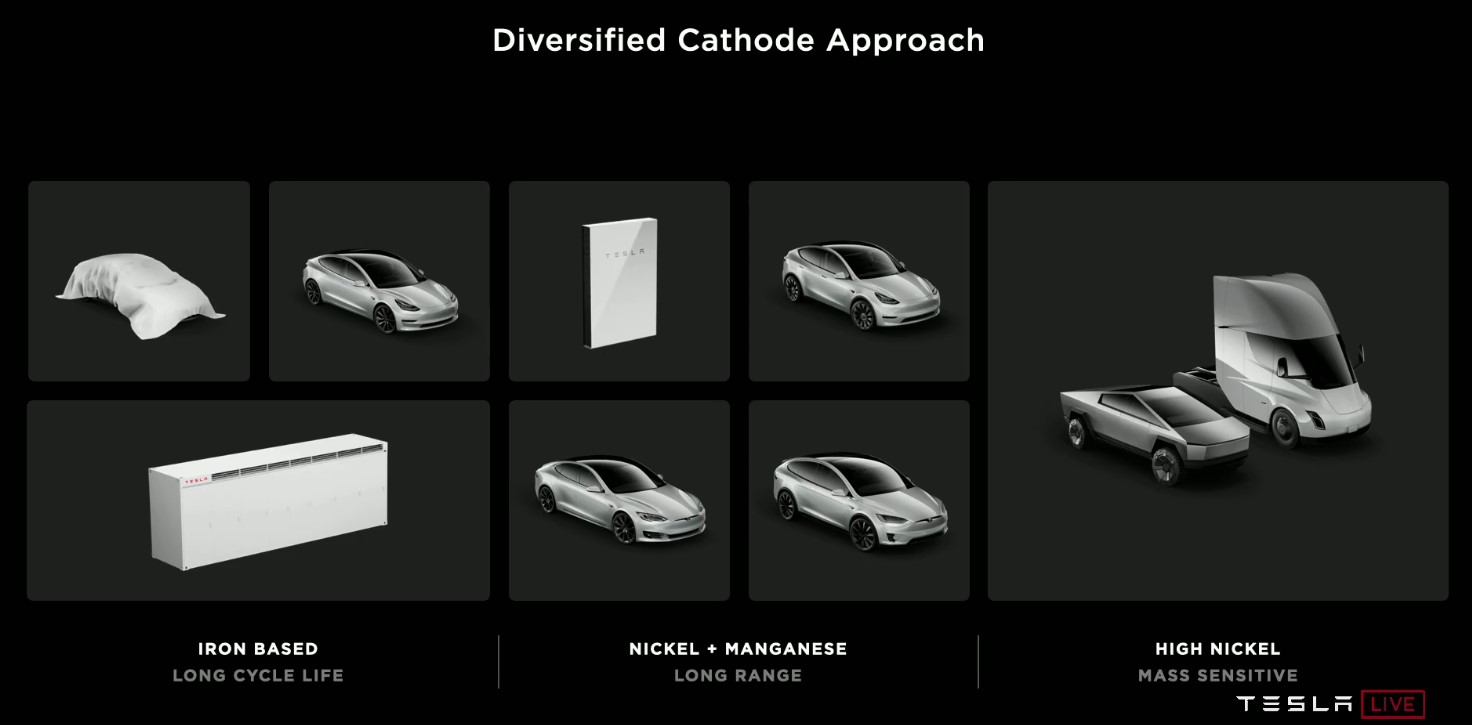

I believe the first Ys out of Berlin will be LFP, using packs built by CATL. Same as 3 and soon Y in China. 500 km WLTP is achievable and plenty for Europe. CATL CTP is a structural design, though maybe not as stiff as and certainly with a higher polar moment of inertia than Tesla's glued 4680 concept.

4680 high nickel will come later, IMHO, or perhaps never absent a DBE breakthrough. I see LFP taking over all but the high end. Even Mercedes plans to use LFP for low- and mid-range. It's heavier, but costs less and is safer with excellent cycle life.

I give a 5-10% chance CATL developed a glued 4680 LFP pack together with Tesla. That would help explain the delay in the Shanghai LFP Model 3. But most likely it's the same prismatic cells they use in their other CTP designs. CTP from CATL and others (e.g. BYD's Blade) have a lot of advantages. I suspect Tesla's structural pack is basically an adaptation of these CTP designs to a cylindrical form factor.